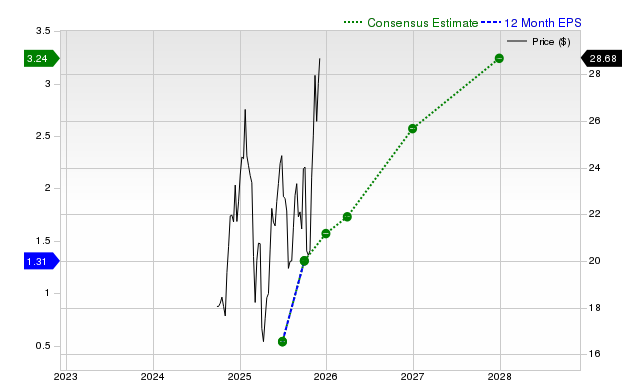

BKV, a natural gas producer, has seen sizable analyst upward revisions to earnings estimates with consensus next-quarter EPS at $0.27 (a +2,600% YoY change) and full-year EPS at $1.57 (+385.5% YoY); over the past 30 days one analyst raised estimates driving a 107.69% rise in the current-quarter consensus and a 48.11% rise in the full‑year consensus. The revisions have earned BKV a Zacks Rank #1 (Strong Buy) and the stock has gained 15.8% over the past four weeks, signaling growing analyst optimism that could support further upside in the equity.

Market structure: The sharp upward estimate revisions for BKV (natural gas producer) disproportionately benefit small-cap pure-play gas explorers that can quickly reset guidance after short prior lows; integrated majors and LNG midstream players are neutral-to-negative as cash flows reallocate. If revisions reflect higher realized Henry Hub or regional basis economics, BKV gains pricing power in the near term (0–6 months) but sector-wide pass-through depends on sustained spot prices > +20% vs. prior quarter. Cross-asset: stronger nat gas cashflows tighten credit spreads for speculative-grade E&P debt (positive for high-yield bonds) and raise natural gas futures — increasing option implied vols for the XOP and CHK/EQT complex by 20–40% on event risk. Risk assessment: Tail risks include a 1–3% probability of a regulatory shock (federal methane/permits) or a weather-driven gas price collapse (>30% drop) that would wipe out 2–3 quarters of upgraded EBITDA for BKV; operational downside (reserve revisions, well performance) is medium probability with high impact. Immediate horizon (days): momentum could continue; short-term (weeks–months): consensus EPS upgrades must be validated by results and realized prices; long-term (quarters–years): capital allocation and hedging patterns will determine sustainable returns. Hidden dependencies: one-off items (asset sale, tax benefit) can drive estimate jumps — verify sources of analyst upgrades within 7–14 days. Trade implications: Direct play — initiate a tactical long BKV position sized 2–3% of portfolio risk-capital with a 3–6 month horizon; set stop-loss at -15% and take-profit at +35–50% or on EPS revisions reversal. Pair trade — long BKV / short XOP (equal notional) to capture idiosyncratic upside while hedging commodity beta; rebalance after quarterly results. Options — buy a 3-month BKV 25-delta call or a 3-month 10–15% OTM call spread (pay <3–4% premium of notional) to cap cost; hedge with a 3-month 10% OTM put if downside protection needed. Contrarian angles: Consensus may be overstating sustainability — the +107% short-term EPS revision is from a low base and could revert if commodity prices slip or if revisions reflect non-recurring gains; the 15.8% four-week rally suggests momentum is partly priced in. Historical parallels: small E&P rerating episodes (2016, 2020 rebounds) quickly reversed when cashflows failed to meet elevated guidance; a prudent investor should demand at least two consecutive months of realized price/backlog evidence before adding incremental exposure (>1–2% more). Unintended consequence: crowded longs could spike implied volatility and widen bid-ask spreads, making late entries costly.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.55

Ticker Sentiment