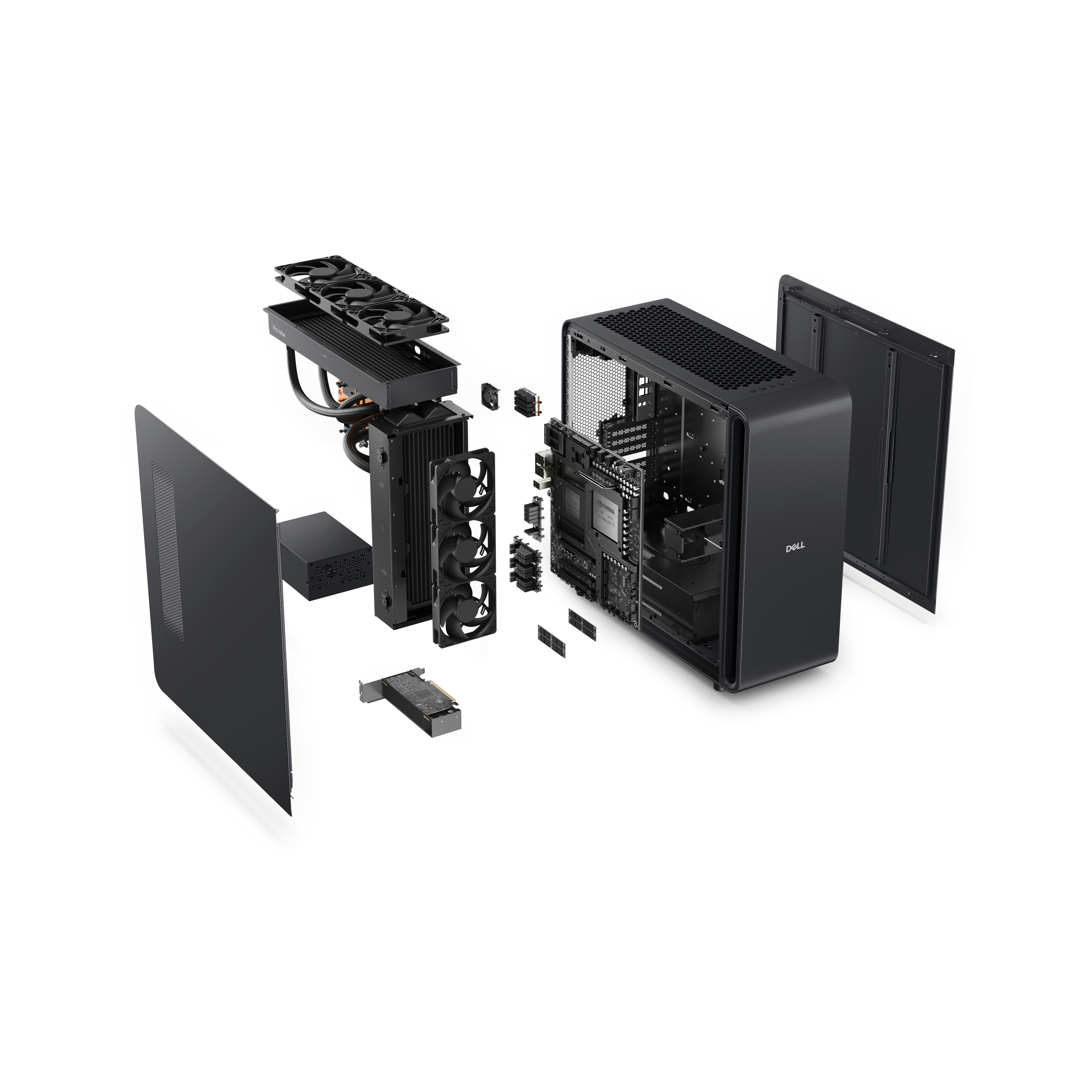

Dell launched a refreshed AI-focused commercial PC lineup including the Precision 9 tower, Precision 7 Series 14 laptop, and the Pro Max desk-side system with Nvidia Grace Blackwell 300. Key specs: Precision 9 supports Intel Xeon 600 CPUs up to 86 cores, up to 4 TB DDR5 ECC across 16 slots, up to 15 PCIe slots and as much as 316 TB of storage; the Precision 7 laptop offers Intel Core Ultra with an integrated NPU up to 50 trillion ops/sec, up to 64 GB LPDDR5X and 4 TB storage; the Pro Max GB300 provides a 72-core Arm CPU, up to 20,000 TFLOPS (4-bit), up to 748 GB coherent memory and 16 TB NVMe. Strategy: Dell is pushing on-premises and desk-side AI to curb cloud token costs and regain commercial-PC momentum, a move that could modestly boost Dell’s hardware competitiveness and near-term demand for high-end workstations.

Dell’s explicit push to make premium, desk-side AI infrastructure a repeatable commercial segment creates a nearer-term reallocation of AI capex away from cloud-hosted vGPU instances and toward higher-ASP OEM sales. That reallocation needn’t be large to matter — a sustained 2–5% shift of enterprise training/inference hours on to-premises would meaningfully lift OEM workstation revenue mix and spare-part/refresh cycles over 12–24 months, while also compressing cloud GPU utilization growth that underpins current data-center capex forecasts.

Supply-chain winners are non-linear: OEM margins and demand will concentrate on a narrow set of high-margin components (high-wattage GPUs, ECC DDR5, enterprise NVMe), increasing pricing power for dominant GPU suppliers and memory/NVMe vendors for quarters at a time. Conversely, this intensifies single-supplier and thermal/power design risk for smaller chassis and PSU vendors, and it compresses upgrade cadence — customers who invest heavily in massive local systems may defer refreshes, lowering replacement revenue velocity across years.

Key near-term catalysts are inventory digestion and enterprise procurement cycles (6–12 months) — reported “pull-forward” orders today may only materialize in revenue next-quarter to next-year, creating a classic guidance-vs-reality trap. Tail risks include a sudden deceleration in GPU availability, a competitive price response from hyperscalers (driving token/cloud costs down), or Dell execution missteps; any of these could reverse sentiment quickly within 1–3 quarters despite structurally positive medium-term demand.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.35

Ticker Sentiment