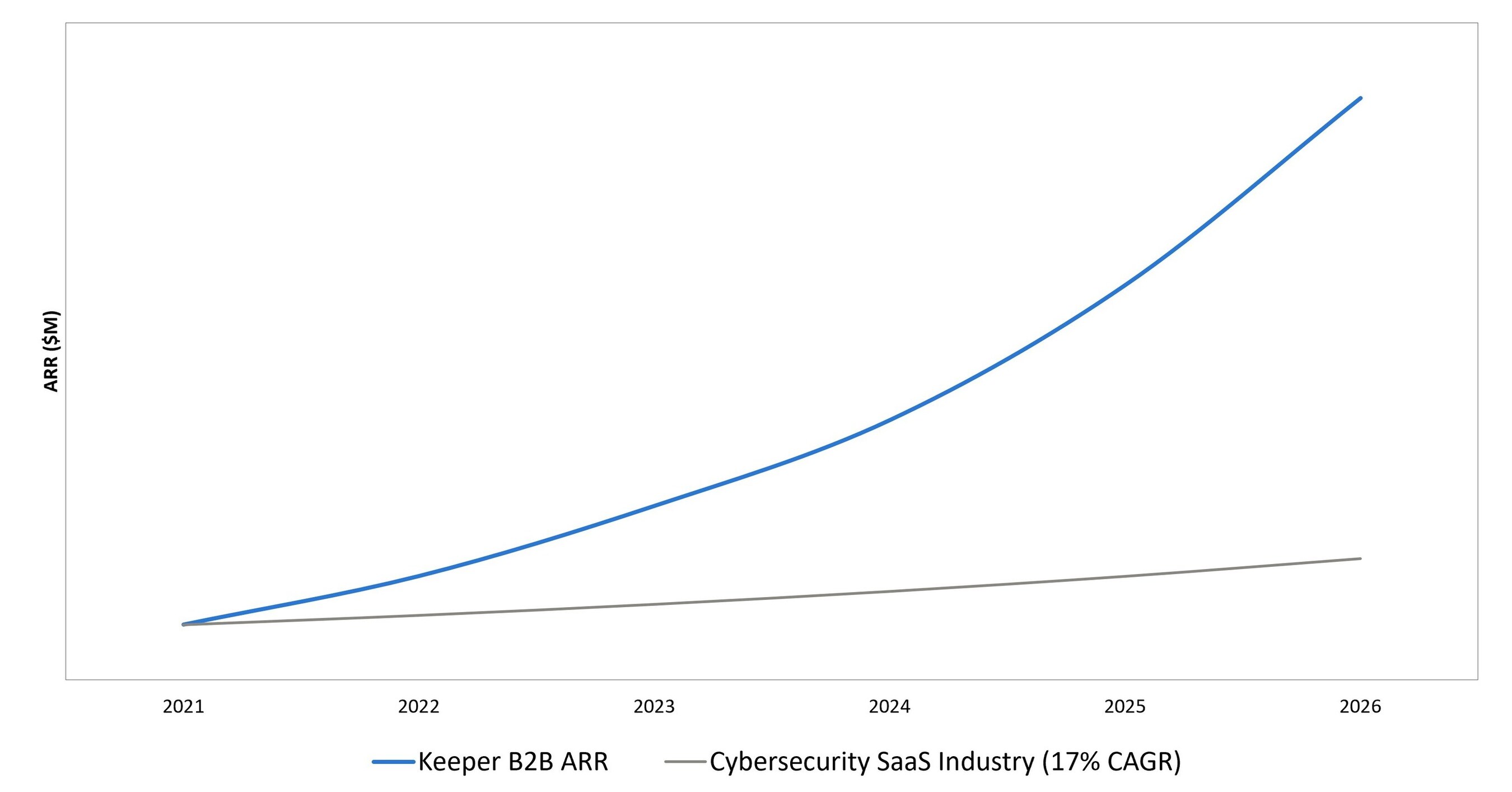

Keeper says it has surpassed $225M in ARR, reporting 10x year-over-year growth for KeeperPAM since its February 2025 launch and adding an average of 850 new organizations per month. Gartner (2025) recognized Keeper as the second-fastest-growing security software competitor globally, reinforcing momentum as enterprises expand agentic AI and non-human identities (NHIs) that increase identity attack surfaces. The company frames its unified privileged access management platform as positioned for an accelerated path to $1B ARR, supported by a debt-free capital structure.

The real signal here is budget migration inside cybersecurity: AI agents and machine workflows force security teams to spend on discovery, secrets, session control, and auditability, which is a higher-friction purchase than human SSO. That tends to favor the few vendors with credible privileged-access depth and can compress the value of broad-but-shallow identity platforms if they cannot prove machine-identity coverage. CYBR is the cleanest public beneficiary; PANW can participate through platform bundling, but the incremental upside is more limited because the market already prices it as a control-plane consolidator. Second-order, this is a headwind for seat-based identity names that rely on workforce login volumes rather than privileged control points. If enterprise AI spend shifts from experimentation to production, procurement will increasingly ask for non-human identity inventory and governance, which raises switching costs for incumbents that already own secrets/session telemetry and lowers them for point solutions. The article itself is promotional, so the growth claims should be treated as sentiment fuel, not as proof that the category has reaccelerated in public-company numbers. Near term, this is mostly a catalyst for the next earnings season rather than an immediate standalone trade. The thesis is falsified if public peers fail to mention NHI/agent governance in guidance, or if AI deployments remain sandboxed and do not trigger compliance-driven buying over the next 1-3 quarters. Over 6-18 months, a production incident involving an AI agent’s credentials would be the kind of event that forces a step-change in category demand and multiple expansion.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly positive

Sentiment Score

0.55

Ticker Sentiment