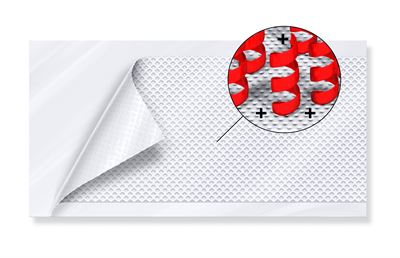

Swedish medtech Amferia has signed a distribution partnership with Magnum Veterinaaria to roll out its antimicrobial peptide hydrogel wound dressings across the Baltic states (Latvia, Lithuania, Estonia) with availability targeted for spring 2026. The product — positioned as Europe’s first veterinary dressing using stabilized antimicrobial peptides — reportedly accelerates healing, counters antibiotic-resistant bacteria by physically disrupting cell membranes, and can amplify antibiotic bactericidal effects up to 64x in research; Amferia is already marketed in parts of Europe and is pursuing U.S. regulatory approval for human wound care. The deal expands Amferia’s commercial footprint in animal health but is incremental from a market-moving perspective absent revenue or clinical-trial milestones.

Market structure: Winners are specialty veterinary distributors and companion-animal product lines (distribution analogs: Covetrus CVET, Patterson PDCO) plus niche medtech/peptide suppliers; losers are low-margin generic veterinary antibiotics and commoditized dressings where pricing will be pressured. Expect initial market penetration in Baltics of <5% of wound-care units in 2026, scaling to 5–15% in 2–3 years in specialty clinics; pricing can command 1.5–3x conventional dressings but not a full antibiotic-replacement price premium. Risk assessment: Key tail risks include regulatory setbacks (EU/US veterinary/human approvals within 6–24 months), manufacturing scale/cost overruns (peptide synthesis costs could blow out COGS by +200–400 bps), and adverse-event recalls that would crater adoption. Immediate impact is negligible (days); watch distribution launches over next 90–180 days and human-regulatory catalysts over 12–24 months; hidden dependency: vet reimbursement/budget cycles and feed/food-animal restrictions could limit TAM. Trade implications: Tactical longs: small exposure to distribution plays (CVET, PDCO) and large, diversified animal-health (Zoetis ZTS) for optionality on adoption and M&A; pair: long CVET vs short Elanco (ELAN) to capture distribution/portfolio skew. Use 9–15 month call spreads (10–20% OTM) rather than outright calls to limit premium; prefer avoiding small medtech debt and long-dated bonds of pre-revenue peptide firms. Contrarian angles: Consensus will likely overrate near-term revenue—Baltic launch is proof-of-concept, not scale—so valuation rerating will follow multi-year adoption or an acquisition. Historical parallel: multiple peptide-platform companies showed early clinical promise but failed on stability/manufacturing; if Amferia cannot hit scaleable COGS targets or faces IP litigation, downside is severe.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.30