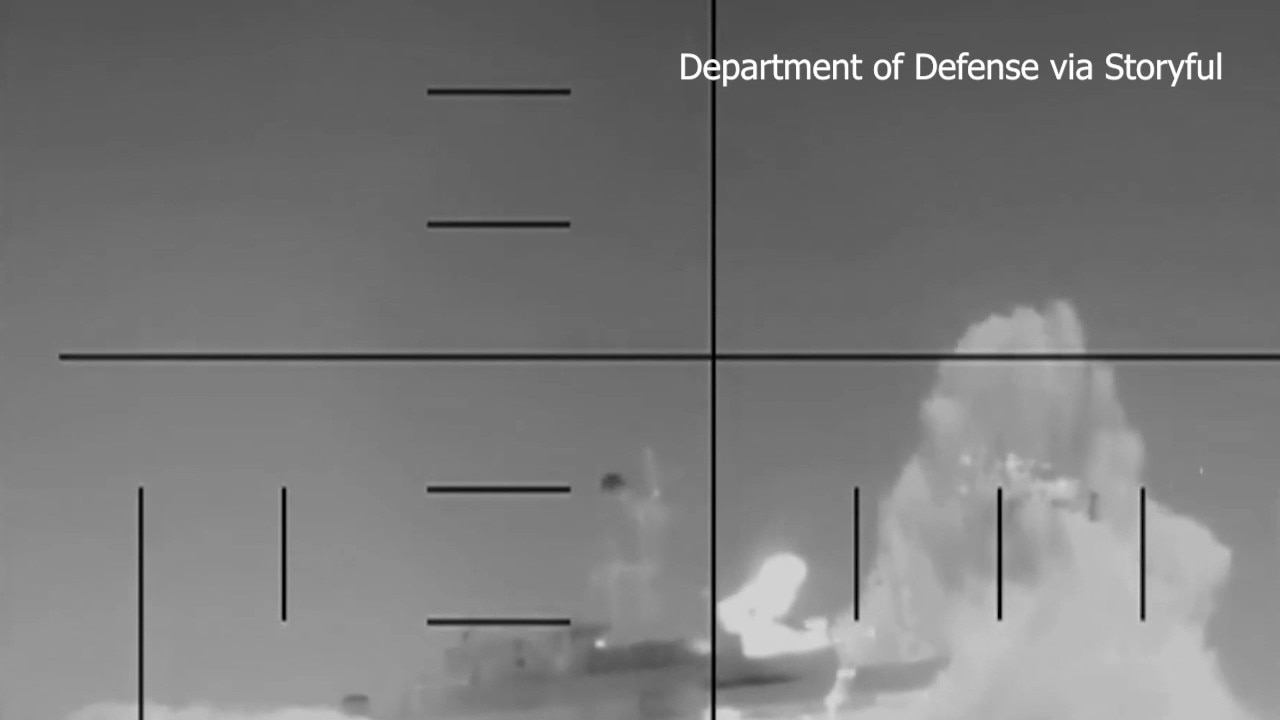

A U.S. submarine torpedoed and sank the Iranian warship IRIS Dena on March 4 in the Indian Ocean; Sri Lanka rescued 32 sailors and recovered 87 bodies. Washington rejects Iran’s claim the vessel was unarmed, while Tehran and an anonymous Indian official assert it was on a noncombat/ceremonial mission, creating acute ambiguity. The dispute increases regional escalation risk and is likely to pressure risk assets, raise energy and shipping volatility, and support defensives and defense-sector exposure in near-term portfolios.

This incident is a catalytic shock to regional naval procurement economics: expect a reallocation of near-term defense budgets toward anti-submarine warfare (ASW), torpedo countermeasures and survivability upgrades. For countries balancing limited budgets, a 1–3% re-prioritization of naval capex within 12–24 months could translate into multi-hundred-million-dollar tenders for sensors, expendables and platform hardening across South Asia and the Middle East.

Marine insurance and route-risk pricing will reprice faster than physical rerouting: war-risk premiums on Indian Ocean/Arabian Sea transits are likely to spike first, compressing carrier margins and temporarily elevating spot container and tanker freight 5–15% for the most exposed lanes over 4–12 weeks. That shock benefits firms that underwrite or broker specialty marine risk (and penalizes thin-margin carriers and airlines with international exposure) even if cargo volumes remain stable.

Macro spillovers: expect risk-off flows into U.S. Treasuries and gold in the immediate days, EM sovereign spreads to widen 20–70 bps, and incremental volatility in oil if chokepoints or insurance-led reroutes threaten Middle East exports. The key reversals are diplomatic de-escalation, transparent verification of operational intent onboard visiting vessels, and a demonstrable stabilization of naval rules-of-engagement — any of which can unwind risk premia within 2–8 weeks.

Contrarian frame: the market’s default to “full regional conflagration” is an overreaction relative to historic calibrated maritime deterrence episodes; most shocks of this nature produce policy-level bargaining and targeted capability buys rather than sustained trade-disrupting warfare. Tactical dislocations in equities and freight create a buy-the-dip window for select EM credits and under-owned defense names once headline-driven volatility abates (4–12 week horizon).

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.60