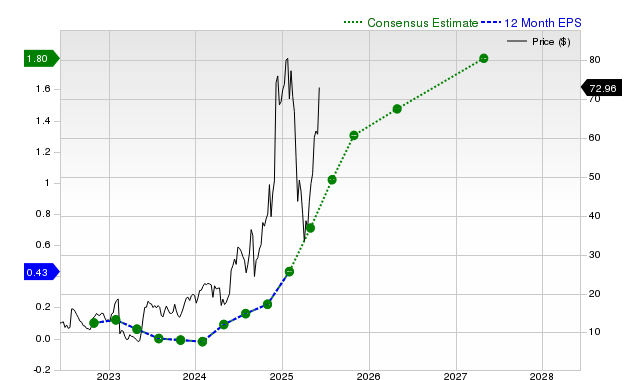

Credo Technology Group (CRDO) has seen substantial upward revisions to earnings estimates, with the current-quarter Zacks consensus EPS at $0.73 (+192% year-over-year) and full-year EPS at $2.66 (+280% year-over-year). Over the past 30 days the forward quarterly estimate rose 48.49% (three upward revisions, none negative) and the full-year consensus increased 31.09% on five upward revisions, contributing to a Zacks Rank #1 (Strong Buy) and an 11.2% stock gain over the past four weeks; these revisions indicate materially improved analyst expectations that may support further upside in the shares.

Market structure: The news is a classic estimate-revision driven rally for a small/SMID tech name (CRDO) — beneficiaries are CRDO shareholders, sell‑side analysts, and suppliers of high‑speed optical/SerDes components; losers are generic networking incumbents if Credo takes share. The 48–31% one‑month lift in consensus means near‑term price discovery is driven by expectations, not yet proven revenue cadence; expect elevated liquidity and 10–30% intraday swings around earnings/catalysts over the next 1–3 months. Risk assessment: Tail risks include a single large customer disappointment, supply‑chain hiccup for advanced silicon, or an analyst revision reversal that triggers a 30–50% drawdown in a thinly traded stock. Immediate (days) risk: mean reversion after an 11% four‑week run; short term (weeks–months): earnings/guidance must validate +192% Q/Q EPS est — miss would amplify volatility; long term (quarters–years): durable market share requires product wins vs integrated silicon vendors and steady hyperscaler demand. Trade implications: Tactical long exposure sized small (1–3% portfolio) makes sense; prefer buy‑writ or debit call‑spread (6–12 month) to target 30–60% upside while capping premium. For relative plays, go long CRDO vs short SOXX/XLK (equal dollar) for 3–6 months to isolate company‑specific upside; trim on a 20–30% run or add on a 12–15% pullback. Contrarian angles: Consensus likely overweights estimate momentum and underweights execution/gross‑margin risk — revisions can flip quickly in semiconductors. Historical parallels: small tech names with Zacks #1 ratings often retrace 40–60% after one missed guide; hence size positions defensively and use option structures to control tail loss.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

moderately positive

Sentiment Score

0.50

Ticker Sentiment