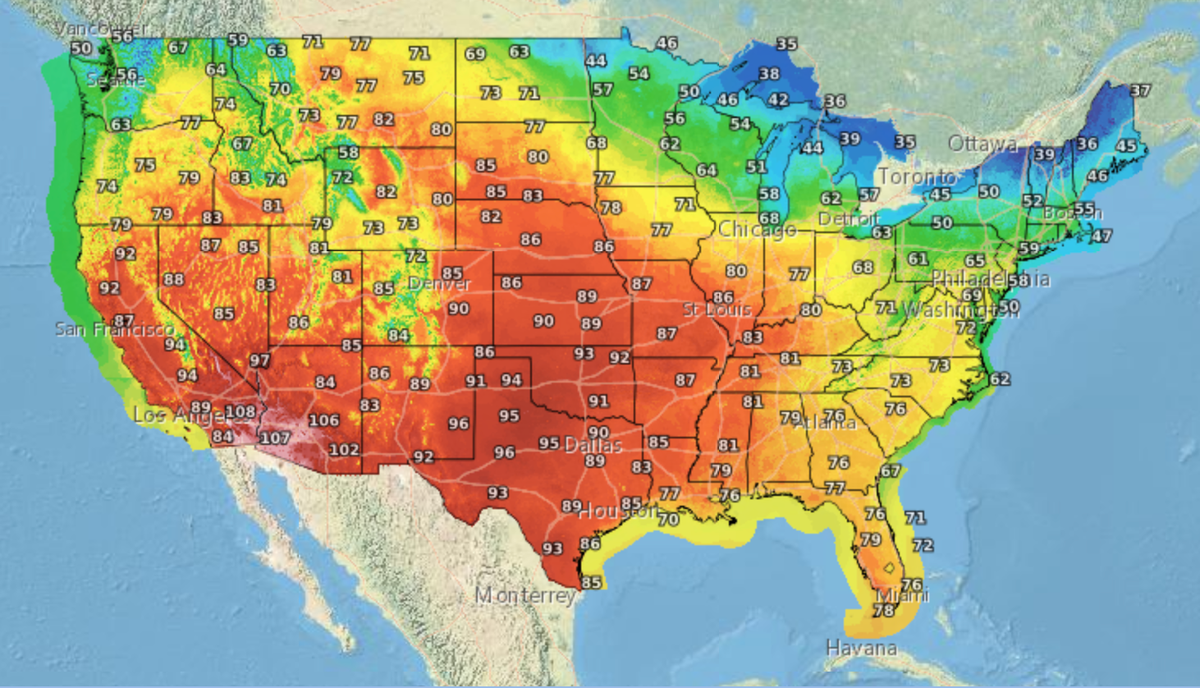

Record March heat: North Shore, CA hit 108°F (state March record), Phoenix reached 105°F (earliest by >1 month), and Martinez Lake, AZ hit 110°F (highest March temperature in U.S.). A record-strong March high-pressure ridge is driving temperatures 20–30°F above normal; World Weather Attribution finds the event ~4x more likely and ~1.4°F hotter because of human-caused climate change. Heat advisories and extreme-heat alerts raise near-term health, power-demand and wildfire risks, while abrupt snowpack loss threatens spring water supply and amplifies drought/wildfire exposure for affected sectors.

Early-season heat anomalies have an outsized economic lever: they compress the normal spring transition window that markets, utilities and agriculture rely on to reallocate water, fuel and labor. Rapid snowmelt produces a front-loaded loss of seasonal hydropower and reservoir buffering within weeks, forcing marginal supply to switch to thermal generation and driving summer spark spreads materially wider than models that assume gradual melt.

Grid reliability and fuel markets will feel the impact before insurance markets price it in. A multi-week spike in peak demand and increased peaker-plant dispatch tends to lift near-term natural gas forwards and localized basis spreads in Western hubs by double-digit percentage moves during stressed months, while insured wildfire risk and catastrophe modeling typically show losses accumulating over a 6–18 month window as claims, loss-adjustment and underwriting cycles react.

On the demand side, durable goods and services tied to cooling and resilience (HVAC OEMs, distributed storage, backup generation, irrigation equipment, and municipal water capex) see accelerated replacement/upgrade cycles; that drives 2–4 quarter revenue uplift for OEMs and installers even if seasonality normalizes. Conversely, concentrated exposure names—regional insurers, undercapitalized muni issuers, and unhedged renewable-heavy grid participants—face persistent margin and funding stress unless reinsurance capacity or federal mitigation dollars are stepped up within the next 3–12 months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.45