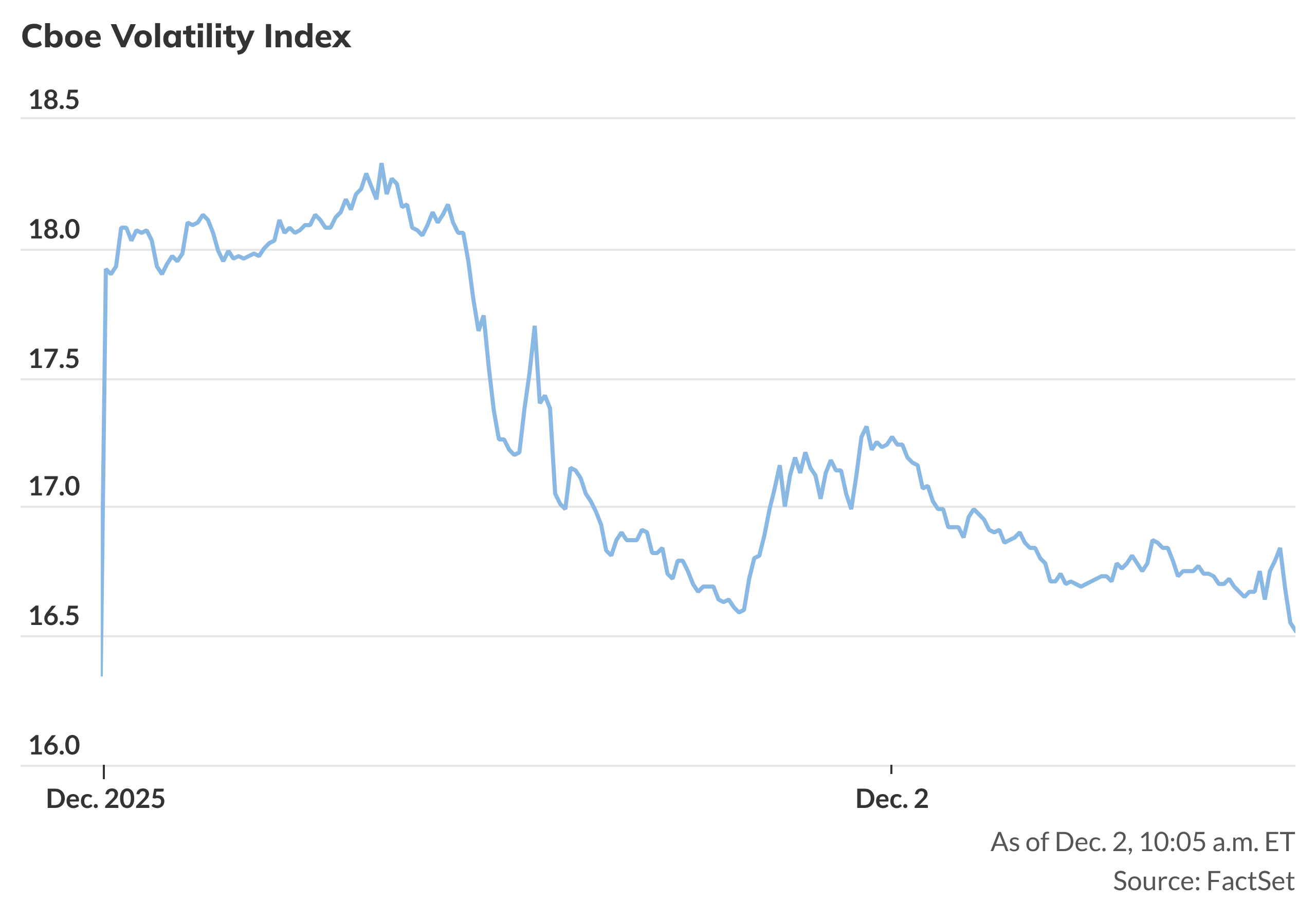

Stocks rose as the Cboe Volatility Index fell about 4% on Tuesday, trading near 16.5 after hitting above 18 the previous day and spiking above 27 on Nov. 21. The decline in the VIX—which measures option-implied expected volatility—signals lower expected market volatility and a momentary relief among investors, potentially encouraging incremental risk-on positioning. Managers should monitor VIX trajectory for confirmation of sustained calm or a reversal that would affect hedging and options strategies.

Market structure: A falling VIX (from >27 on Nov 21 to ~16.5 now) directly benefits equity risk-on exposures, short-vol ETP issuers (e.g., SVXY beneficiaries) and ETF/structured-product sellers who collect premium; it hurts long-vol products (VXX) and holders of expensive tail hedges. Lower implied vol reduces option spreads and hedging costs, improving return-on-capital for active long equity managers; expect rotation into cyclicals and small caps if flows sustain. Risk assessment: Tail risk is non-trivial — a geopolitical shock, hawkish Fed CPI/PCE surprise, or dealer de-grossing could re-spike VIX above 30 within days, causing >5-10% equity drawdowns. Near-term (days) momentum can persist; short-term (weeks–months) mean reversion to 18–22 is plausible if positioning normalizes; long-term (quarters) depends on liquidity/monetary path. Hidden dependency: crowded short-vol gamma exposure can create feedback loops during expiries or large index moves. Trade implications: Prefer tactical risk-on longs balanced with cheap, defined-cost protection: buy QQQ/IWM for 1–3 month windows while selling near-term OTM premium to fund positions; use small, targeted VIX call spreads or 3–6 month SPY put spreads as tail insurance. Sector tilt to discretionary and financials likely outperforms staples/defensive areas if VIX stays <18 and yields rise modestly (10–30 bps). Contrarian angles: The market is underestimating the fragility of short-vol crowding — current low VIX may be underdone relative to positioning, not fundamentals; historical parallels (Feb 2018, Mar 2020) show rapid reversals. Mispricing exists in near-term options (cheap OTM puts) but beware that selling premium without paid hedges risks asymmetric losses; a small, explicit insurance allocation is prudent.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.28