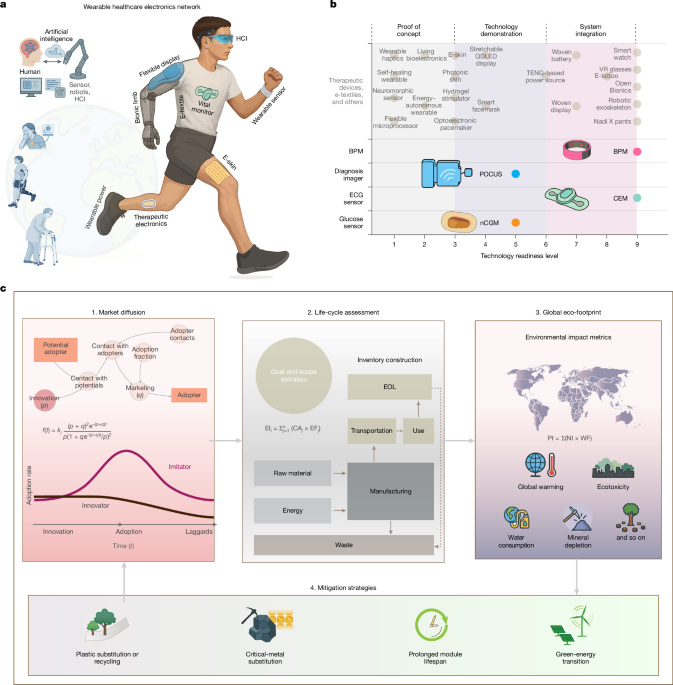

A life‑cycle assessment of wearable healthcare electronics finds per‑device warming impacts of 1.1–6.1 kgCO2‑eq and projects global annual device consumption to rise ~42× by 2050 to nearly 2 billion units, producing roughly 3.4 MtCO2‑eq alongside significant e‑waste and ecotoxicity risks. The study shows marginal environmental gains from recyclable/biodegradable plastics but identifies greater impact reductions from substituting critical‑metal conductors and optimizing circuit architectures, highlighting supply‑chain exposure to critical materials and opportunities in design‑for‑recycling and materials innovation. For investors, the findings point to sectoral ESG risks (regulatory, reputational, and e‑waste liabilities) and potential upside for firms offering low‑impact materials, advanced recycling, or circuit efficiency solutions.

Market structure: Winners will be firms that sell lower-metal circuitry, closed-loop recycling, and reusable-service models (materials innovators, recyclers, and platform OEMs with scale such as AAPL), while pure-play disposable-device manufacturers (high-volume CGM makers like DXCM) face margin pressure from EPR and material-cost inflation. The 42x projected device growth to ~2bn units/year by 2050 implies multi-year upward pressure on copper/gold/rare‑metal demand and gives pricing power to suppliers of speciality foils and flexible PCBs; expect some OEMs to pass costs to payers or consolidate procurement. Risk assessment: Tail risks include EU/US extended producer responsibility (EPR) levies, sudden export curbs on critical metals, or a product-recall wave that forces buyback/recycling — each could cut EBITDA 5–25% for exposed med‑device makers within 6–24 months. Hidden dependencies: cloud-compute and IoT scaling (emissions/energy caps), rebound effects (more devices -> higher total emissions despite per‑device improvements); catalysts in the next 30–180 days are UN/EU e‑waste reports and major OEM sustainability pledges that could reprice winners/losers. Trade implications: Tactical books should overweight AAPL (+1–2% portfolio) for scale/engineering to absorb regulatory costs, underweight/hedge DXCM (-0.75–1.5%) via puts (6‑9 month, ~10% OTM) anticipating margin/headline risk, and go long IRTC (+0.75–1%) for recurring-service models that reduce per‑unit e‑waste over 12–24 months. Add 0.5–1% commodity exposure to copper (COPX or JJC) for a 12–36 month horizon, scaling on >10% pullbacks. Contrarian angles: Consensus over-emphasises plastics; the paper shows metal conductors and PCB architecture drive outsized impact — so early stakes in metal‑substitution IP/recyclers are underpriced. The market may under-react to consolidation risk: large vertically integrated OEMs (Apple) could gain share as regulators favor reusable/service models, producing asymmetric upside if EPR rules arrive in 12–24 months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

-0.05

Ticker Sentiment