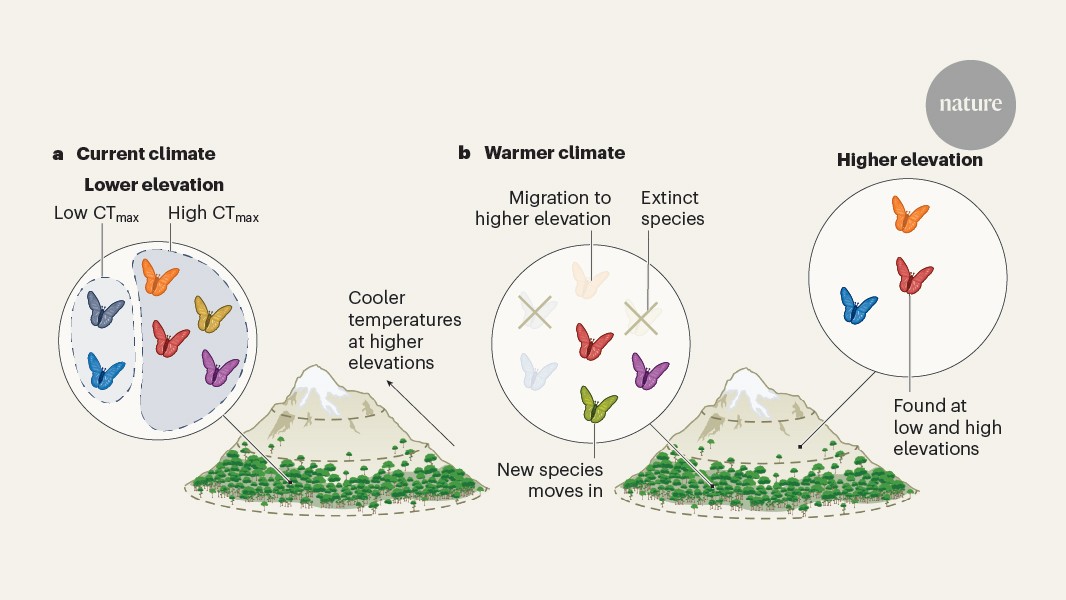

A Nature News & Views article highlights research that rising temperatures pose a significant threat to tropical insects because many species have narrow thermal tolerances and thus are particularly vulnerable to warming. The piece emphasizes potential ecological consequences — including impacts on pollination and food-web dynamics — but provides no company-level financial data or immediate market-moving figures, implying only long-term relevance for sectors that depend on intact ecosystem services.

Market structure: Rising tropical temperatures that suppress insect populations shift pricing power toward crop-technology, seeds and insurance providers while pressuring processors that rely on tropical crops. Expect demand uplift for Corteva (CTVA) and FMC-like crop-protection and seed solutions as farmers pay a 5–15% premium for mediated yield protection; coffee/cocoa spot markets (JO/NIB) can gap higher on 5–20% supply shocks. Tropical-producing sovereigns (BRL, IDR) face weaker export receipts and wider CDS spreads if multi-year yield declines >3–5% occur.

Risk assessment: Tail risks include a rapid, correlated collapse in pollination services causing >30% price shocks in specialty crops and sovereign stress in 1–3 years, or regulatory bans on specific pesticides that reprice agchem EBITDA within 6–12 months. Short-term (days–weeks) triggers are heatwave/El Niño announcements and USDA/CONAB crop revisions; medium-term (3–12 months) are harvest reports and insurance-loss seasons; long-term (1–5 years) are structural yield declines and premium inflation. Hidden dependencies include labor availability (disease/vector spread) and deforestation-driven microclimate changes that amplify yield shocks.

Trade implications: Tactical trades include buying 3–9 month call options on coffee (JO) and cocoa (NIB) to capture asymmetric upside if early-season yield shocks hit; initiate 1–2% long positions in CTVA and short 1–2% exposure to consumer names with high tropical-crop intensity (e.g., SBUX, HSY) as a pair trade. Buy selective reinsurer exposure (RNR or MUV2/Munich Re ADR equivalents) via 6–12 month longs to capture rising premiums; hedge FX exposure to BRL/IDR with 3–12 month currency hedges if satellite NDVI drops >5% vs 5-year average.

Contrarian angles: Consensus may overstate uniform crop downside — some pest declines reduce damage and lower pesticide volumes, pressuring agchem margins; therefore avoid full-size long equities in a single agchem name and prefer options or spreads. Historical parallels (2015 El Niño coffee shock) show 30–50% commodity spikes but also rapid policy and planting responses within 12–24 months, so size positions with 20–30% haircut and set clear stop-losses. Monitor ENSO index, USDA yield revisions, and EU/US pesticide regulatory notices over the next 30–90 days as primary catalysts to scale positions.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00