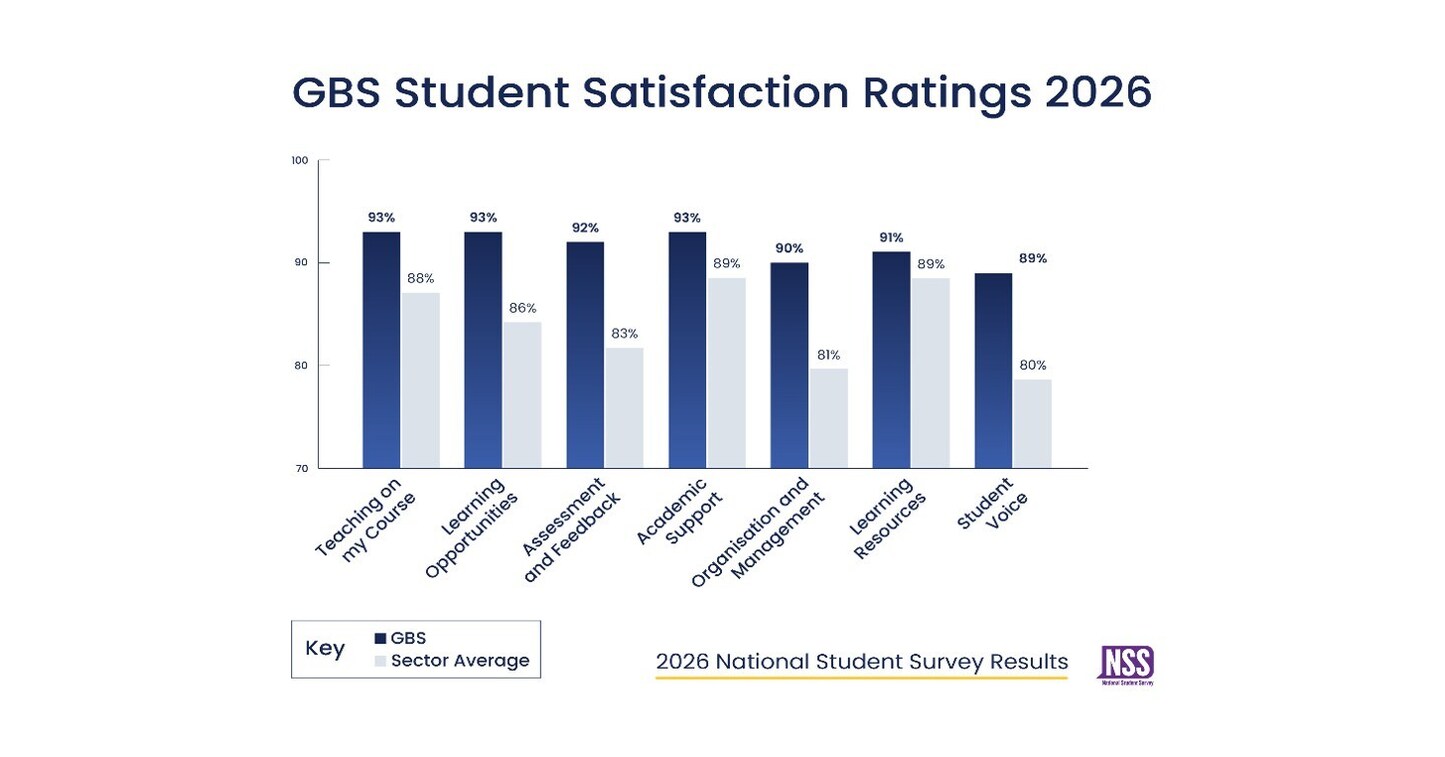

La Global Banking School (GBS) surperforme le secteur dans l’enquête nationale auprès des étudiants (NSS) 2026 sur les sept thèmes principaux, avec des taux de satisfaction allant jusqu’à 92,9% dans « L’enseignement dans ma formation » et « Soutien universitaire ». Les résultats s’appuient sur 6 488 réponses d’étudiants (hausse de 1 087 vs 2025) et un taux de réponse publié de 81,2%, renforçant l’image d’une amélioration de l’expérience étudiante.

This is a quality signal, not a revenue event. In UK higher ed, student-satisfaction outperformance only matters if it feeds through to lower dropout, better referrals, and cleaner OfS scrutiny; that is a multi-quarter earnings lever, not an immediate trading catalyst. The real winner is likely the broader model of flexible, career-oriented providers versus traditional campus-heavy institutions: better support and teaching scores improve retention economics and reduce marketing spend per enrolment, which should widen the gap against lower-touch rivals. Second-order, the pressure shifts to competitors that rely on weak student-outcome metrics or have heavier dependence on franchised delivery. If the market starts to believe these quality rankings predict continuation and graduate outcomes, private valuation multiples for vocational operators can expand modestly over 6-18 months, but only if corroborated by actual retention and employment data. Absent that confirmation, this is mostly a PR-driven reassurance trade with limited public-market impact. Contrarian view: the consensus may be over-weighting a survey result and under-weighting selection bias, as higher-response, more engaged cohorts often score better. The falsifier is simple: if next intake enrollment, continuation, or completion rates do not improve over the next 1-2 academic cycles, the satisfaction premium is noise. Near term, there is no obvious listed-equity expression unless one already has exposure to UK private education or adjacent training assets.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.30