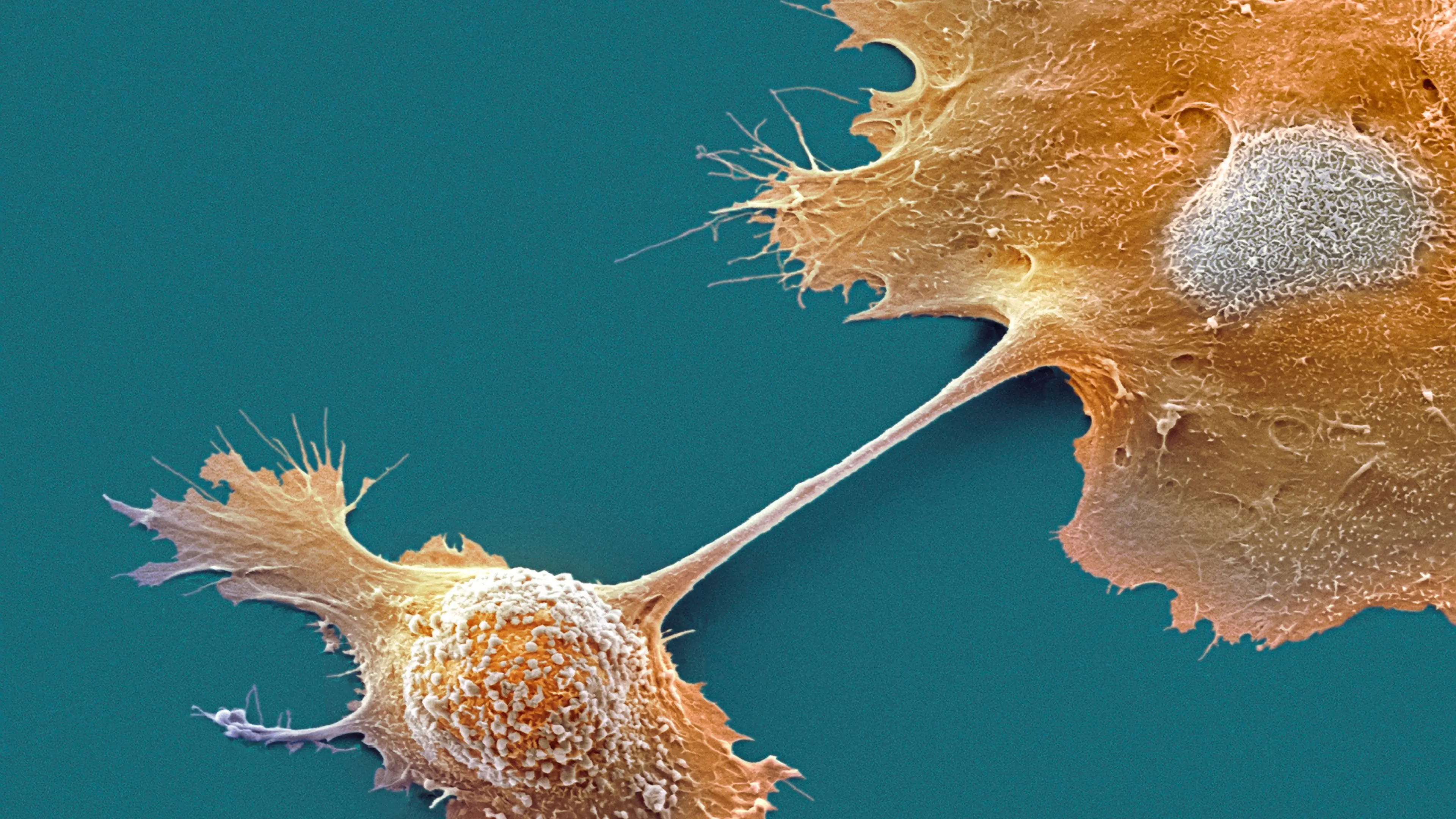

Revolution Medicines' daraxonrasib extended average survival in pancreatic cancer to 13.2 months versus 6.7 months on standard chemotherapy, while Actuate Therapeutics' elraglusib also roughly doubled one-year survival in a separate study. Revolution plans to submit daraxonrasib to the FDA under an expedited review path after a Phase III trial, and Actuate is advancing a Phase II program. The results are encouraging for a disease with limited treatment options and could support broader adoption if later-stage data confirm the benefit.

The market is likely underpricing how quickly a credible pancreatic signal can re-rate both programs, but the bigger second-order winner is the “KRAS as backbone” thesis. If the Phase III read truly translates into approval, RVMDW moves from speculative biotech to a de-risked oncology platform with label-expansion optionality into earlier lines and combinations; that changes partnering leverage, not just near-term revenue expectations. ACTU’s asset remains earlier-stage, but the Nature Medicine publication gives it a non-trivial credibility boost that can support financing on less punitive terms and keep the story alive through the slower data cadence.

The key competitive effect is not winner-take-all between these two drugs; it is that any validated activity in pancreatic cancer resets comparator expectations for the whole space. That can pressure smaller single-asset oncology names with no clear biomarker or mechanism differentiation, while benefiting tools/cro partners involved in combination trials and trial-enabling diagnostics tied to KRAS mutation testing. It also raises the odds of combo regimens becoming the real commercial prize, which favors companies with stackable assets or the ability to run rapid combination studies over pure single-agent developers.

The main tail risk is execution, not biology: Phase II/III efficacy can compress materially once treated across broader, sicker, or earlier-line populations, and pancreatic approvals are notoriously vulnerable to durability questions. For RVMDW, the near-term catalyst path is relatively clean over days to weeks as FDA filing/priority-review headlines hit; for ACTU, the timeline is months to years and the stock remains exposed to dilution risk before registrational clarity. Any signal of increased toxicity, manufacturing bottlenecks, or weak subgroup durability would quickly unwind the current enthusiasm.

Contrarian view: consensus may be too focused on absolute survival improvement and not enough on the fact that pancreatic cancer remains a combination-therapy market. That means monotherapy upside could cap out unless the drugs prove additive with surgery/chemo/IO, and the better trade may be on platform optionality rather than headline data alone. The move looks more underdone in RVMDW than ACTU because the former has a nearer monetization path and regulatory catalyst stack, while ACTU is still one step removed from definitive proof.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly positive

Sentiment Score

0.78

Ticker Sentiment