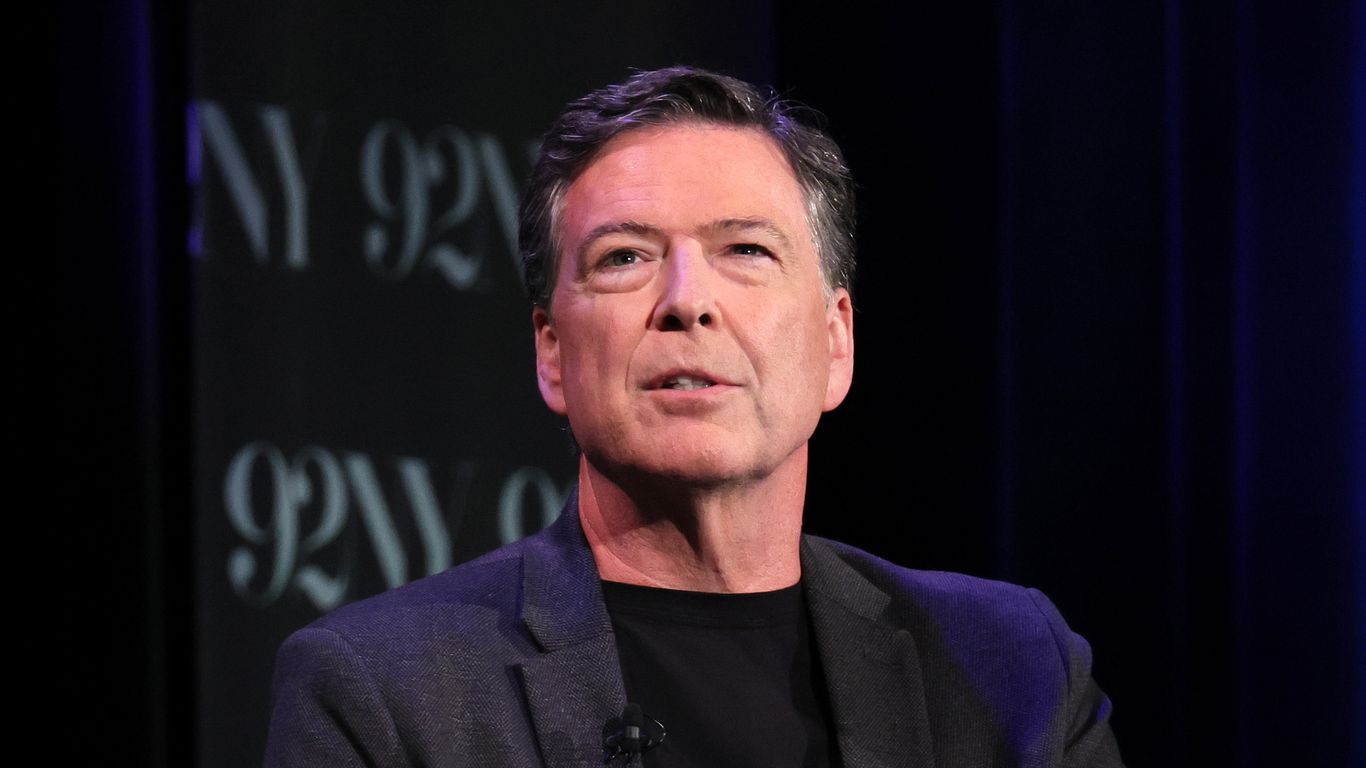

More than 130 subpoenas have been issued in the broad 'grand conspiracy' probe; former FBI Director James Comey was subpoenaed last week relating to his alleged role in drafting the January 2017 Intelligence Community Assessment that referenced the Steele Dossier. The investigation, overseen by Judge Aileen Cannon in the Southern District of Florida, targets senior officials who served under Presidents Obama and Biden and seeks to link figures including Comey, John Brennan and Jack Smith in a conspiratorial prosecution. Legal timing is mixed: Brennan remains within a five-year statute of limitations for alleged false testimony in 2023, while the window has closed for alleged false statements by Comey in 2020. For portfolios, this is a politically significant development but likely has negligible direct market impact.

This subpoena materially increases the odds that headline legal drama — not a neat near-term resolution — persists through the next 6–12 months, raising a politically driven volatility premium that’s currently underpriced by equity markets. The key second-order channel is attention and resource diversion: prolonged high‑profile prosecutions pull senior DOJ/CIA staff time, slow new regulatory/enforcement actions and lengthen procurement and contracting timelines, which reshuffles winners toward firms with large backlogs and away from small, discretionary-exposure names.

Expect a tactical bid for traditional safe-haven assets and short-dated volatility hedges around court milestones: 30–90 day windows around indictments, pre-trial motions or Judge rulings are where realized vol spikes. Conversely, larger prime government contractors should see relatively smoother revenue visibility if award cadence slips by 3–6 months — that favors balance-sheet-heavy primes over smaller integrators or suppliers that rely on fast award turnarounds.

There is a modest, under-appreciated payoff to being long corporate-service providers whose revenues scale with legal caseload (e-discovery, litigation finance, legal analytics): persistent high-profile cases lift recurring revenue and pricing power for these vendors by measurable basis points on margins. The primary tail risks are (a) an escalation that drags in additional senior officials or corporate actors, producing a market-wide risk-off shock, or (b) a rapid judicial curtailment that collapses the uncertainty premia — both are binary and will materialize within weeks of major filings or rulings.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00