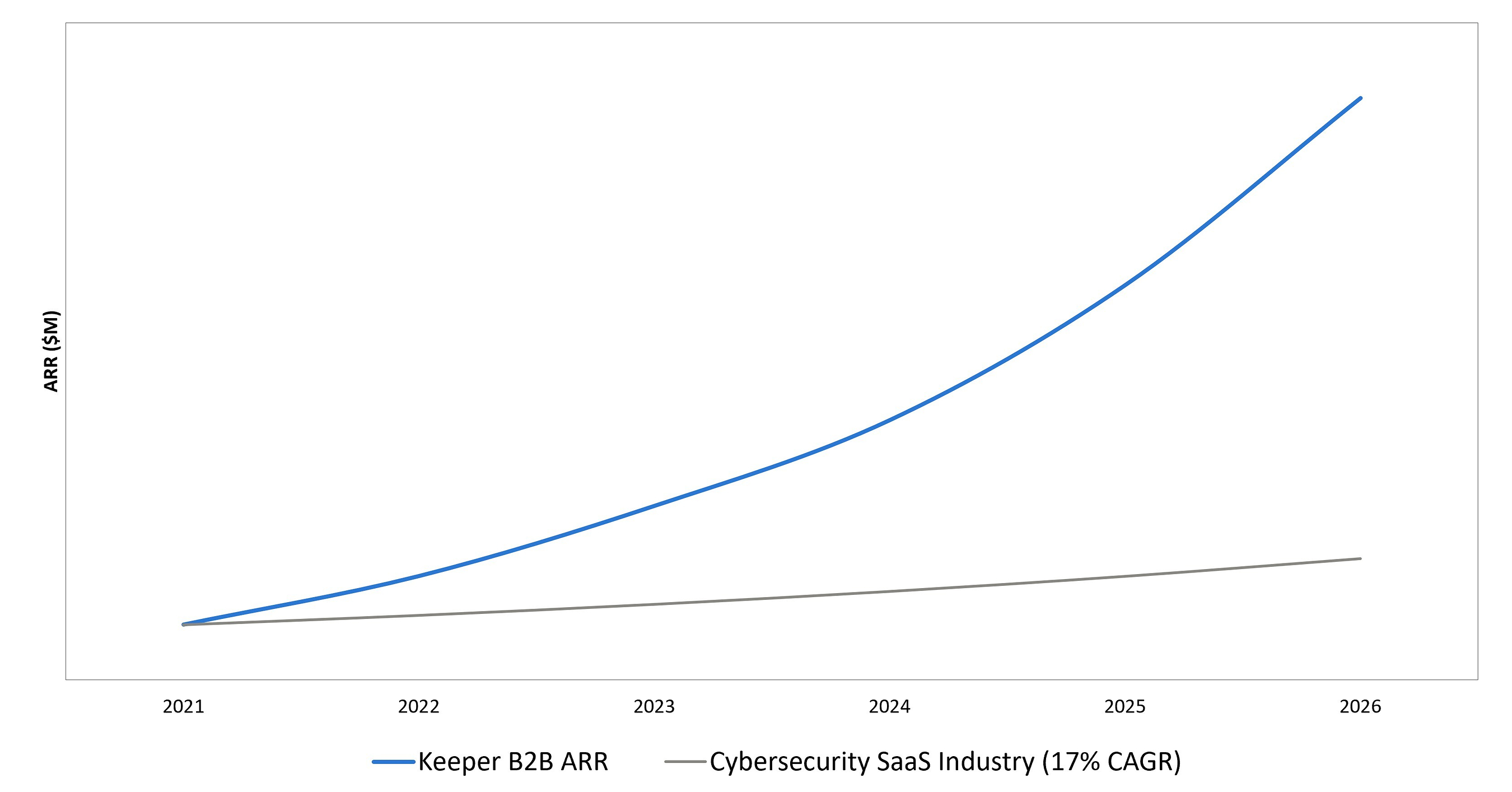

Keeper Security announced it reached $225M in ARR, growing over 3x since 2021 and at more than 4x the industry average. Since launching KeeperPAM in Feb 2025, the company reports 10x YoY growth in KeeperPAM revenue and added ~850 new organizations per month (400+ new features in 15 months). The firm is targeting an accelerated path to $1B ARR and highlights optionality for a future public offering, reinforcing strong momentum in AI-native identity security amid rising non-human identities.

The real signal is not the ARR milestone; it is that identity spend is broadening from human-user admin to machine-to-machine governance, which should lift TAM for platform vendors faster than point products. That favors the large suites that can bundle privileged access, secrets, endpoint privilege, and session control into one procurement motion: PANW, CRWD, and to a lesser extent OKTA. The second-order loser is the fragmented PAM/password-management layer, where growth can look strong in a rising category but multiple risk emerges once large buyers standardize on fewer control planes. In the next 1-3 months, this is more of a sentiment check than a direct earnings catalyst for public comps. The tradeable implication is whether management teams begin quantifying AI-agent identity spend on calls; if they do, expect upward revisions to security budget growth assumptions and some multiple support for CYBR/ZS/PANW. If they do not, the market may treat this as another private-market narrative with limited read-through. The contrarian issue is that “150:1 non-human identity growth” can be true while near-term monetization remains modest: agentic AI is still early, and buyers often solve governance with existing cloud/identity vendors before adding a specialist. That means the near-term upside is likely in product attach and renewal uplift, not explosive seat growth. Falsifiers: slower-than-expected enterprise AI deployment, or security budgets getting reallocated into cloud/compute rather than identity controls over the next two quarters.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly positive

Sentiment Score

0.70

Ticker Sentiment