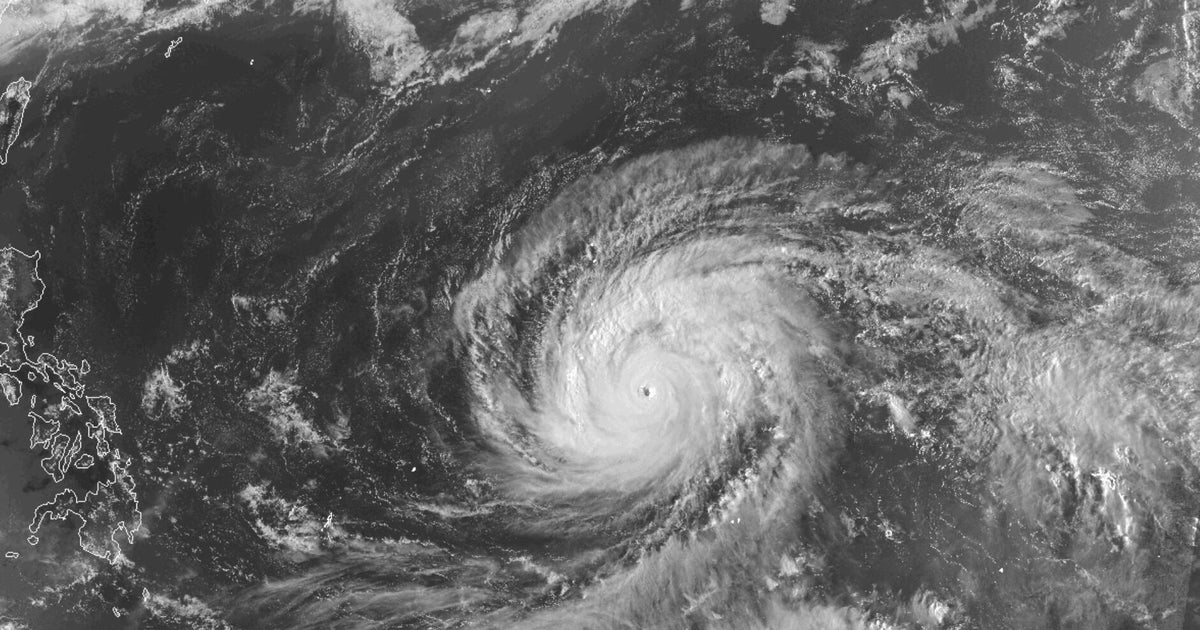

Super Typhoon Sinlaku brought 130 mph sustained winds, a strong Category 4, as its eyewall struck Tinian and Saipan and threatened widespread flooding and infrastructure damage across the northern Marianas. Guam recorded gusts up to 80 mph, with tropical-storm-force winds expected through Wednesday afternoon, multiple power outages reported, and schools closed Tuesday and Wednesday. Typhoon warnings remained in effect for several islands, with Sinlaku peaking at 180 mph over the open ocean earlier in the week.

The first-order trade is not in the storm path itself but in the fragility of island infrastructure and the time-to-recovery curve. For small grids, one major line fault or generator trip can create a multi-week sequencing problem: restoration of telecom, fuel distribution, refrigerated storage, and airport ops tends to lag the headline weather window by days to weeks. That means the economic damage can outlast the meteorological event, especially for places that rely on a single logistics spine and imported fuel. The bigger second-order effect is on military readiness and shipping reliability in the western Pacific. Even without a direct hit on Guam, sustained high winds and port/airfield disruption can create temporary rationing of sorties, maintenance delays, and inventory prepositioning friction. For defense contractors with Pacific exposure, the near-term read-through is less about incremental spending and more about operational strain that can pull forward maintenance, repair, and hardening budgets over the next 1-3 quarters. Transportation and insurance are the cleanest public-market transmission channels. Air cargo, regional passenger flow, and port throughput can see a short-lived but sharp drop, while insurers/reinsurers with catastrophe exposure may not book the loss immediately if the island footprint is limited; the underappreciated risk is claims inflation from business interruption and utility restoration rather than wind damage alone. Conversely, utilities, emergency telecom, generator, and diesel logistics vendors can see a temporary demand spike, but only if they can actually get assets and fuel into the region. The contrarian view is that this may be overread as a macro-Pacific supply shock. Because the geography is isolated, the real P&L impact is likely concentrated in a handful of local and defense-adjacent operators rather than broad semis, shippers, or global industrials. The best risk/reward is therefore in expression sizing: trade the restoration window, not the storm headline, and fade any attempt to extrapolate this into a durable commodity or growth impulse.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.74