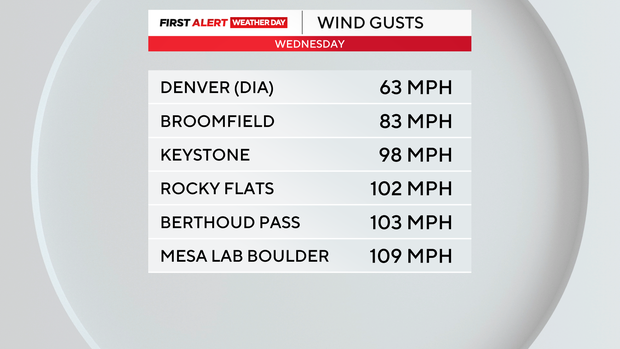

Jet-stream-accelerated downslope winds battered Colorado's northern Front Range with the strongest gust measured at 109 mph at NCAR's Mesa Lab and multiple locations exceeding 100 mph, downing power lines and damaging vehicles. Over 100,000 customers faced safety-related outages, highways near the foothills were closed and flights at Denver International were delayed; high wind warnings, a red flag warning for far eastern Colorado, and a Fire Weather Watch are in effect with additional gusts up to 90 mph expected Thursday into Friday, raising near-term operational risk for utilities, transportation, and regional infrastructure.

Market structure: Immediate winners are electricity generators and spot power markets, civil-construction firms, and local grid-reliability contractors due to outage repairs and potential accelerated hardening capex; expect regional day-ahead power and ancillary-service prices to spike 20–40% in the next 7–14 days and contractor revenues to lift 5–10% over the next quarter. Clear losers are airlines and airport service providers (DEN-centric carriers), autos/retail exposed to physical damage, and P&C insurers facing near-term claims; short-term cashflow strain for regional airlines could compress margins by several percentage points in the month ahead. Risk assessment: Tail risks include a cascading grid failure or a large wildfire that produces >$500M insured losses and triggers regulatory rate reviews or emergency public capex; probability low (<5%) but systemic. Time horizons: immediate (0–7 days) for flight disruptions and power-price spikes, short-term (1–3 months) for insurance claims and contractor revenue recognition, and long-term (6–36 months) for utility capex/rate-base repricing and potential insurance premium increases. Hidden dependencies: transformer/relay supply chains and skilled-labor availability could extend restorations; catalysts include repeat high-wind events and dry conditions that would materially raise loss estimates. Trade implications: Direct plays favor short-dated protection on airlines and long exposure to utility/contractor equities with strong balance sheets; consider buying 30-day put spreads on AAL/UAL-sized to 0.5–1% of portfolio and adding 2–3% long to XEL or NEE for defensive cashflows and potential rate-base upside over 6–12 months. Options: implement defined-risk put spreads on regional airlines and a 1-month bull call spread on front-month Henry Hub gas futures expecting a 10–30% move; rotate 1–3% from cyclicals into utilities and construction equipment names (CAT, DE) for 3–12 month horizon. Contrarian angles: Consensus may overstate permanent damage—many disruptions are one-off and price moves could be mean-reverting in 2–4 weeks; airline IV may be rich for short-dated puts if cancellations normalize. Historical parallel: 2013 Colorado floods led to multi-year municipal and infrastructure spending — if state/federal relief follows, Colorado contractors and muni bonds could outperform. Unintended consequence: accelerated grid-hardening policy could favour large vertically integrated utilities and muni issuers, pressuring smaller captives and boosting muni issuance (watch yields).

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.45