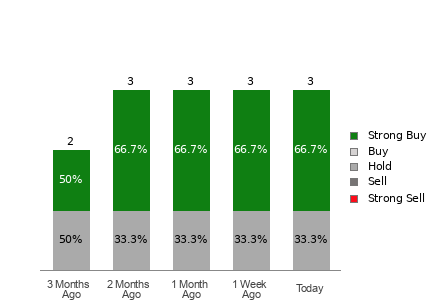

CSLM Acquisition Corp. (SPWR) carries an average brokerage recommendation (ABR) of 1.67 based on three brokerage firms, with two of three ratings at Strong Buy (66.7%). Zacks reports a Zacks Rank #3 (Hold) driven by an unchanged Zacks Consensus Estimate for the current year of -$0.45 over the past month, and the note flags potential upward bias in broker recommendations. Given the negative per-share estimate and the conflicting buy-equivalent ABR versus a Hold Zacks Rank, a cautious stance is warranted until further earnings- or deal-related clarity emerges.

Market structure: The disconnect between broker ABR (1.67, buy) and Zacks Rank (Hold) points to persistent sell‑side optimism benefiting brokers, SPAC sponsors and retail momentum players while disadvantaging arbitrageurs and longer‑term fundamental buyers who pay premiums for deals that may never close. Expect episodic repricing around deal announcements over the next 3–6 months; failed or dilutive deals commonly produce 10–40% downside from peak levels. Cross‑asset: a rise in SPAC idiosyncratic risk will lift equity volatility (SPX options skew) and increase demand for short‑dated puts or VIX hedges, with minimal direct FX or commodity impact but potential localized pressure on short‑term corporate credit if PIPE market retracts. Risk assessment: Tail risks include SEC/regulatory action reclassifying SPAC warrants or tightening disclosure (could compress implied valuations 20–50%), PIPE funding withdrawals, and sponsor conflicts/insider redemptions that force reversions to trust NAV (~$10). Immediate (days) risk is volatility around headlines; short term (weeks–months) is deal/PIPE execution; long term (quarters–years) is regulatory/legal restructuring of SPAC economics. Hidden dependencies: broker ratings drive retail order flow and can create self‑fulfilling price moves until fundamentals reassert. Trade implications: Direct plays favor small, disciplined arbitrage and hedge strategies — e.g., selective long only when SPWR trades >4–7% below pro‑rata trust value with a 6‑month horizon, or buy 3‑month put spreads to cap downside at defined cost. Pair trade: short SPAC ETF SPAK vs long XLF (financials) to capture relative weakness if deal flow disappoints while keeping exposure to banks/underwriters if activity recovers. Use options (3‑6 month) to express directional views while limiting capital at risk. Contrarian angles: The consensus misses that steadily unchanged negative EPS estimates (‑$0.45) imply scarce upside absent a high‑quality deal — so buy ratings are fragile. Reaction may be underdone for high‑quality sponsor SPACs (better than peers) and overdone for speculative names; history (2021 SPAC unwind) suggests quick 30–60% re‑ratings can occur on catalyst failure. Unintended consequence: regulatory tightening could improve long‑term deal quality, creating selective opportunities in 12–24 months for disciplined fundamental picks.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00