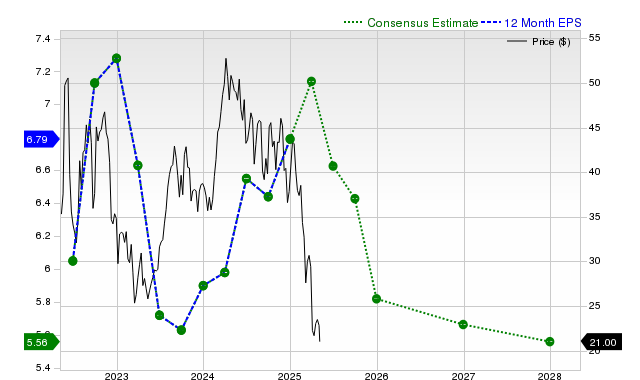

SM Energy (SM) faces downward earnings revisions with consensus EPS of $0.93 for the current quarter (-51.3% YoY; consensus -9% in 30 days), fiscal-year EPS of $5.39 (-20.7% YoY; -2.3% in 30 days) and next-year EPS of $4.74 (-12%). Consensus revenue estimates are $787.01M for the quarter (-7.7% YoY) and $3.29B/$3.25B for the current/next fiscal years (+22.3% / -1.1%), while the last reported quarter showed revenue of $811.59M (+26.1% YoY) and EPS $1.33 (vs $1.62 prior), a revenue miss of 3.13% and an EPS beat of 6.4%. Shares have underperformed recently (-11.9% over one month), Zacks assigns a Rank #3 (Hold) and a Value Style Score of A, suggesting the name may be attractively valued but faces near-term earnings pressure.

Market structure: A near-term earnings reset for SM reallocates marginal production and capital to the lowest-cost operators and hedged balance-sheet winners; expect weaker peers and oilfield services to cede pricing power while midstream fee-takers and fiscally conservative E&Ps gain negotiating leverage. If capex is cut industry-wide, the supply response could tighten crude in 3–9 months, supporting commodity-sensitive recoveries. Risk assessment: Key tail risks are a >20% WTI shock in 90 days, a covenant breach or accelerated reserve impairments, and an operational incident that forces production curtailment; these would propagate into HY spreads and equity downside. Near-term (days–weeks) equity volatility and analyst downgrades dominate; medium-term (3–12 months) outcomes hinge on commodity path and capex discipline; hidden dependencies include SM’s hedge roll schedule and midstream take-or-pay exposures. Trade implications: Tactical exposures should be event-driven and volatility-aware: favor option structures that cap premium while preserving upside if oil stabilizes (+$5 WTI moves within 90 days). Prefer dollar-neutral relative-value versus higher-cost peers to exploit valuation dislocation; de-risk energy-service exposure and reallocate to high-quality midstream where fee-based EBITDA cushions commodity swings. Contrarian angle: Consensus underweights asset-value and PDP reserve optionality and may over-penalize one quarter’s revision; a disciplined buy at 10–20% post-guidance dip can capture mean reversion if commodity-backed cash flows hold. The market has historically overreacted to single-quarter EPS hits in E&P (recovery often within 6–12 months when oil normalizes), but watch for persistent analyst downgrades that can prolong the mispricing.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mixed

Sentiment Score

-0.12

Ticker Sentiment