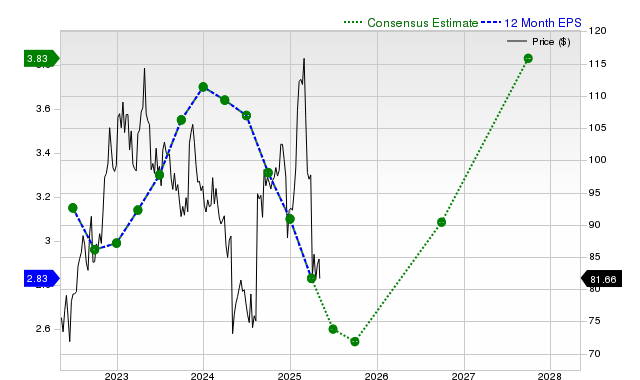

Starbucks (SBUX) has recently underperformed, returning -1.3% over the past month against the S&P 500's +1.9%, driven by significant downward revisions to earnings estimates for the current quarter and fiscal year. Consensus EPS for the current quarter is $0.59 (-26.3% YoY) and for the current fiscal year is $2.21 (-33.2% YoY), leading to a Zacks Rank #4 (Sell) for SBUX, which suggests potential near-term underperformance. Furthermore, the stock carries a Zacks Value Style Score of D, indicating it trades at a premium relative to its peers despite recent EPS misses.

Starbucks (SBUX) is facing significant headwinds, evidenced by its recent stock underperformance of -1.3% over the past month and a deeply negative fundamental outlook driven by deteriorating earnings estimates. Sell-side analysts have markedly lowered their projections, with the consensus estimate for the current quarter's earnings per share (EPS) now at $0.59, representing a 26.3% year-over-year decline, and this figure has been revised downward by 10.8% in just the last 30 days. The full-year forecast is similarly weak, with an expected EPS of $2.21, a 33.2% drop from the prior year. These substantial negative revisions are the primary driver behind the stock's Zacks Rank #4 (Sell), signaling likely near-term underperformance. While revenue growth remains positive, with a forecast of +3.9% YoY for the current quarter, the company's recent history reveals a stark divergence between top-line performance and profitability; Starbucks beat revenue estimates in three of the last four quarters but missed EPS estimates in all but one, including a significant -23.08% miss in the last reported period. Compounding these concerns is a rich valuation, with a Zacks Value Style Score of 'D' indicating the stock trades at a premium to its peers despite the challenging earnings trajectory.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly negative

Sentiment Score

-0.65

Ticker Sentiment