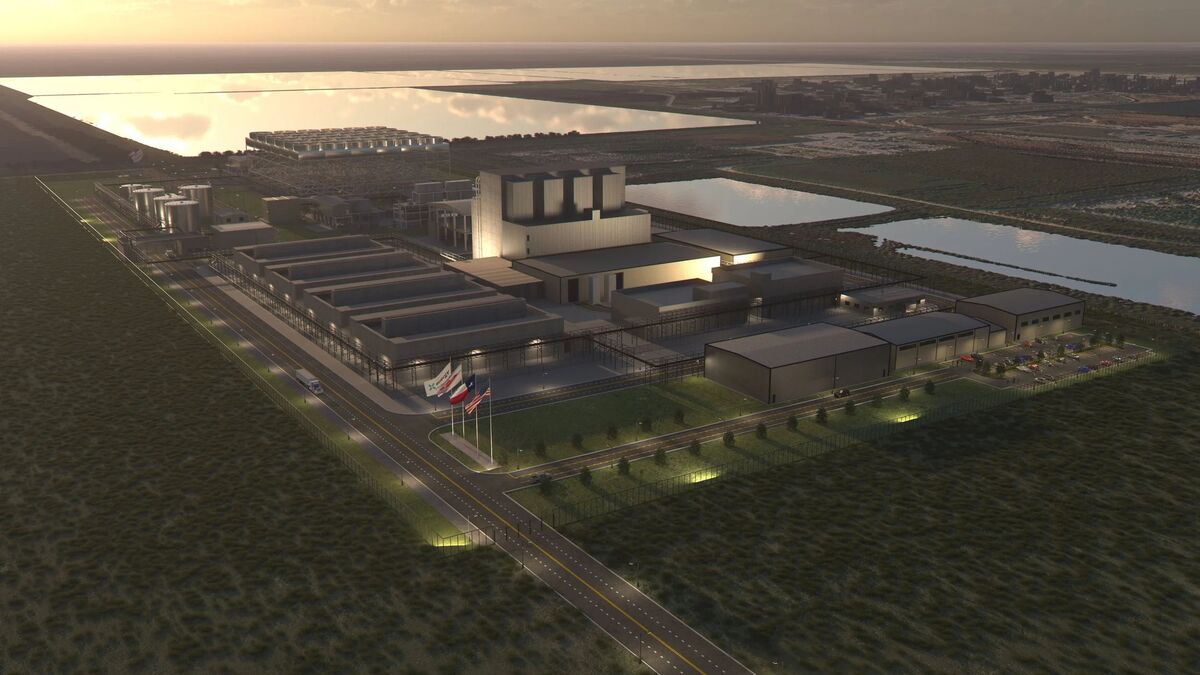

X‑Energy LLC secured approximately $700 million in an oversubscribed Series D financing led by Jane Street Group to commercialize its small advanced nuclear reactor, with new investors ARK Invest and Corner Capital and continued participation from Ares Management and Emerson Collective; the company is backed by Amazon. The large equity infusion accelerates commercialization of advanced nuclear technology and signals sustained private capital appetite for low‑carbon energy infrastructure, relevant to investors focused on energy transition and sustainable finance.

Market structure: Private capital inflows lower the implied financing cost and shorten commercialization timelines for SMRs, benefitting reactor OEMs, TRISO fuel suppliers, uranium miners and engineering contractors; incumbent gas peakers and standalone battery arbitrage providers face longer-term margin pressure if baseload low‑carbon supply scales (3–7 year window). Competitive dynamics favor firms that control licensing, fuel feedstock and modular manufacturing — expect pricing power consolidation in 2–5 suppliers rather than a fragmented market. Cross‑asset: anticipate upward pressure on uranium spot/enrichment; utility/project bonds issuance to rise (spread tightening for sponsors with offtake); modest downward pressure on long‑dated gas forward curves and gas‑peaker capacity valuation. Risk assessment: Tail risks include regulatory reversals, licensing delays, TRISO fuel scale failures, or a high‑profile incident that could re‑politicize nuclear (low prob, very high impact). Immediate impact is negligible (days) but expect re‑rating of small caps in weeks/months and structural demand shifts over 3–7 years. Hidden dependencies: TRISO manufacturing capacity, specialized labor, and geopolitical supply chains (Russia/China exposure) can bottleneck deployments and spike inputs. Key catalysts: NRC licensing milestones, DOE/utility offtakes, uranium spot >$70/lb or major PPA announcements within 6–18 months. Trade implications: Favor monotonic exposure to uranium/materials and select OEMs while hedging execution risk; rotate from pure gas midstream/E&P into nuclear‑adjacent industrials and regulated utilities that can sign offtakes. Use modest option overlays for time‑limited regulatory catalysts (6–18 months). Entry: scale into positions over 6–12 weeks; exits on +30–40% moves or failure to clear regulatory milestones within 12 months. Contrarian angles: The market conflates private oversubscription with commercial certainty — deployment risk and permitting will likely stagger benefits, creating multi‑year dispersion among suppliers. Historical parallels (post‑1970s nuclear rollouts) show serial cost overruns and contractor bankruptcies, so small‑cap supplier rallies can be overdone. Unintended consequence: faster nuclear build could strand natural‑gas infrastructure and credit profiles of midstream firms, creating bond and equity downside not yet priced.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment