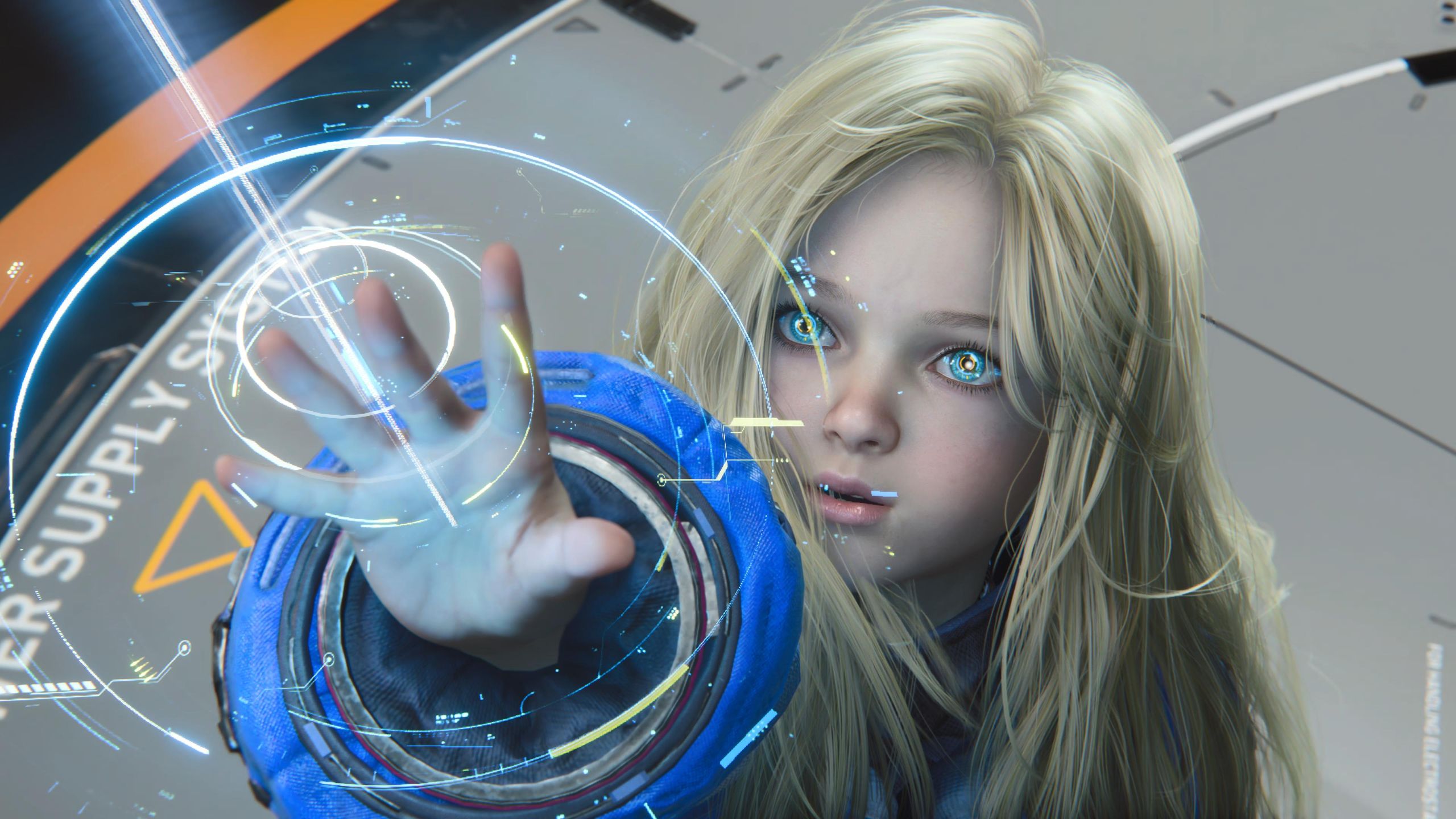

Capcom’s Pragmata is reviewed very favorably, with the article highlighting its innovative shooter/hacking gameplay, strong RE Engine visuals, and surprising variety despite a compact ~10-hour campaign. The main criticism is that the emotional narrative is lightweight, but overall the game is described as one of Capcom’s most inventive action titles in years. Market impact should be limited, though the review supports Capcom’s brand and upcoming release momentum ahead of the 17 April 2026 launch.

This is a useful data point for the premium video-game content stack: Capcom is still demonstrating that original-IP launch quality can create value disproportionate to expected unit volume when execution is high and brand trust is strong. The key second-order effect is not just one title’s reception, but reinforcement of Capcom’s ability to monetize mid-budget, mechanically differentiated games without relying on open-world sprawl or live-service economics. That supports the market’s willingness to assign a quality premium to Capcom’s release cadence, and it raises the bar for peers whose pipelines are heavier on cinematic ambition than on systemic depth. The more important implication is competitive. A strong reception for a compact, systems-first sci-fi action title suggests that consumers remain receptive to “AA disguised as AAA” product — high polish, tight scope, low fatigue. That is a headwind for publishers chasing bloated $100M+ productions, because it signals that gameplay novelty can still outrun narrative spectacle in the premium segment. It also reinforces the idea that engine-level efficiency matters: proprietary tools that compress development time and preserve visual quality can expand margin per shipped title even if the franchise is new. From a trading standpoint, the catalyst is less about this one review than about the market’s extrapolation over the next 1-2 earnings cycles: preorder strength, review aggregates, and whether this converts into a multi-platform tail. The risk is that initial enthusiasm overstates long-tail sales if the title’s emotional stickiness is limited; in that case, upside to estimates may be concentrated in the first 4-8 weeks, with a fade afterward. The contrarian view is that investors may be underpricing the strategic value of proving Capcom can still launch a new-action IP successfully, which improves the optionality value of the portfolio even if immediate software revenue is modest.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly positive

Sentiment Score

0.72