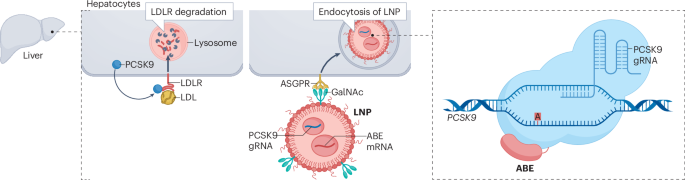

Base editing therapies targeting PCSK9 have entered clinical trials, with early human data showing promise for a durable one-and-done approach to lowering LDL cholesterol. The article suggests a potentially meaningful advance for hypercholesterolemia treatment, though it remains early-stage and not yet commercially validated. Market impact is likely limited to biotech and gene-editing names rather than the broader market.

This is a structural threat to the economics of chronic LDL management, but not an immediate extinction event for the existing PCSK9 franchise. The market is likely over-indexing on the headline of durability and underestimating the slower adoption curve for a gene-editing therapy that must clear not just efficacy, but manufacturing scale, payer comfort, reversibility concerns, and long-tail safety monitoring. That means the first-order winners are probably not the companies with the most exposed current revenue, but the platforms that can credibly position themselves as the “control layer” around one-time editing: diagnostics, longitudinal monitoring, and combination lipid-lowering regimens.

The second-order risk for incumbents is channel conflict, not just share loss. If a one-and-done therapy proves durable in a narrow high-risk phenotype, it can compress the lifetime value of a patient by forcing payers to reframe LDL treatment as an up-front capital expense rather than recurring pharmacy spend. That typically triggers tougher prior authorization, larger outcome-based contracts, and more aggressive step-editing toward cheaper injectables or RNA-silencing agents before an edit is allowed. In practice, that can pressure near-term reimbursement velocity even before broad commercial adoption arrives.

For biotech, this is a signal that the competitive moat is shifting from target validity to delivery and safety economics. The broader base-editing stack gains optionality, but only if the field can prove low off-target risk in larger, more diverse populations and show that hepatic editing scales without rare idiosyncratic toxicity. The key catalyst window is months, not days: follow-on data readouts will determine whether this becomes a niche interventional procedure or a platform with cardiometabolic category expansion. The contrarian read is that the real upside may accrue to the companies whose assets can be paired with editing, not those betting on replacement.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly positive

Sentiment Score

0.70

Ticker Sentiment