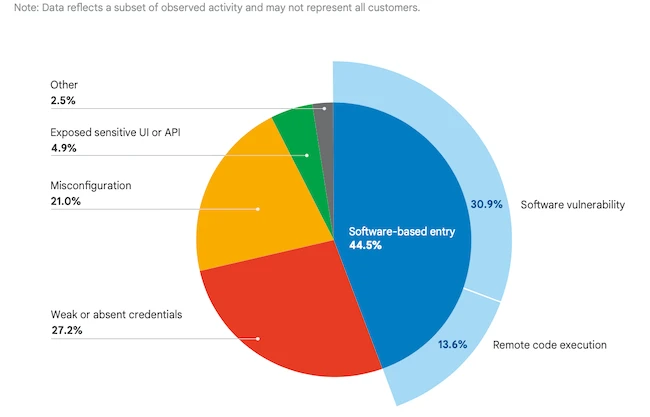

Unpatched third-party applications became the primary initial access vector in Google Cloud incidents in H2 2025, with automated remote code execution and mass exploitation windows collapsing from weeks to days (XMRig miners deployed within ~48 hours of disclosure). Identity compromise (vishing, token/theft, OAuth abuse), insider-driven cloud storage exfiltration, and AI-assisted supply-chain attacks also rose; a North Korean-linked campaign exploited Kubernetes and CI/CD to steal multimillion-dollar cryptocurrency. Expect increased near-term pressure on cloud providers, enterprise patch cycles, IAM/zero-trust adoption, and security tooling focused on supply-chain and application hardening.

Compressed exploit timelines and automated discovery tools change the economics of defensive security: detection-first models and slow patch cycles become a competitive disadvantage. Vendors that deliver near-zero-touch runtime protection (inline virtual patches, behavior-based blocking, eBPF instrumentation) win on immediacy; traditional patch-management vendors only win if they can automate rollouts across CI/CD within weeks. Expect enterprise procurement to prioritize one-click mitigations and managed services that convert security from a CapEx project into an OpEx subscription that can be stood up in days rather than quarters.

Identity and token hygiene will drive the next wave of spend but create operational drag: teams will accept a modest slowdown in developer velocity in exchange for ephemeral credentials, tighter OIDC controls, and automated token revocation. That creates windows for companies offering secrets management, least-privilege orchestration, and CI/CD policy-as-code to expand ARR materially over 12–24 months. Conversely, companies whose go-to-market relies on low-integration friction will see rising CAC as customers insist on prebuilt attestations and compliance connectors.

Supply-chain injection risk elevates demand for SCA, SBOM automation, and in-pipeline runtime safeguards; these products are in the sweet spot for mid-cap security vendors with deep developer integrations. But there is a valuation split risk: a handful of large platform vendors can monetize managed security (marketplace, professional services), compressing margins for smaller point-solution vendors unless they consolidate quickly. Regulatory tail risks (fines, mandated breach disclosures) could crystallize within 6–18 months and are the main near-term multiple compression catalyst.

The consensus underestimates cloud providers’ ability to recapture security spend by bundling managed controls into their developer platforms. That limits downside for major cloud vendors over 12–24 months even as pure-play security names reprice higher growth expectations into nearer-term revenue; tactically, dispersion will be large and event-driven.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.35

Ticker Sentiment