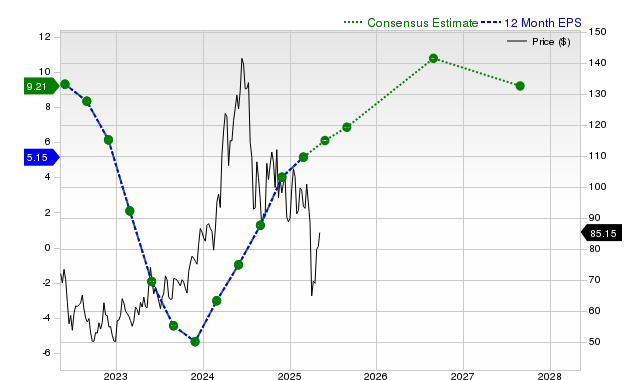

Micron Technology (MU) shares have gained 6% over the past month, outperforming the S&P 500, driven by significant positive revisions to its earnings and revenue estimates. Analysts now project current quarter EPS to increase 112.7% year-over-year to $2.51, with the estimate revised up 23.5% in the last 30 days, alongside robust full-year and next-year growth forecasts for both earnings and revenue. Despite these strong fundamental improvements and consistent earnings beats, the stock holds a Zacks Rank #3 (Hold), suggesting it may perform in line with the broader market in the near term.

Micron Technology (MU) is exhibiting strong fundamental momentum, primarily driven by significant upward revisions in sell-side analyst estimates for both earnings and revenue. For the current quarter, consensus EPS is projected to surge 112.7% year-over-year to $2.51, an estimate that has been revised upward by 23.5% in the last 30 days alone. This trend extends to the full fiscal year, with an expected EPS growth of 497.7%, and continues into the next fiscal year with a 57.4% growth projection. This earnings outlook is supported by robust revenue forecasts, projecting 38.5% YoY growth in the current quarter and 46.5% for the full fiscal year. The company's recent performance validates this optimism, having beaten consensus EPS estimates for four consecutive quarters, including a notable +20.13% surprise in the last report. However, these bullish indicators are tempered by a valuation that is considered at par with its peers, as indicated by a Zacks Value Style Score of 'C'. Consequently, despite the stock's recent outperformance of the S&P 500 (+6% vs +4.1% over the past month), its Zacks Rank #3 (Hold) suggests the market may have already priced in much of this positive news, pointing towards potential near-term performance in line with the broader market.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly positive

Sentiment Score

0.65

Ticker Sentiment