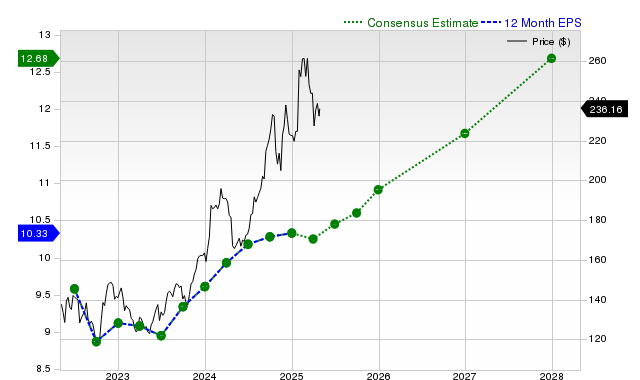

IBM shares have outperformed the S&P 500 over the past month, gaining 7.5% against the index's 3.9%, though trailing its industry's 11.5% rise. The company projects mid-single-digit earnings growth, with consensus EPS estimates for the current and next fiscal years at $10.95 (+6% YoY) and $11.66 (+6.5% YoY), respectively, and corresponding revenue growth estimates of +5.5% and +4.8%. While IBM has consistently beaten EPS estimates over the last four quarters, its Zacks Rank #3 (Hold) suggests near-term performance in line with the broader market, and a 'D' valuation grade indicates it trades at a premium to peers.

International Business Machines (IBM) has demonstrated notable stock performance over the past month, returning +7.5% and outperforming the S&P 500 composite's +3.9% gain, although it has lagged its direct industry peers' average of +11.5%. Forward-looking consensus estimates project stable, mid-single-digit growth, with earnings per share (EPS) expected to increase by +6.0% for the current fiscal year and +6.5% for the next. Similarly, revenue is forecast to grow +5.5% and +4.8% over the same periods. Despite this positive growth outlook, analyst estimates for both revenue and earnings have remained unchanged over the past 30 days, suggesting a lack of new positive catalysts to drive revisions higher. While the company has a strong track record of beating EPS estimates for four consecutive quarters, including a significant +12.68% surprise last quarter, its valuation appears stretched. The stock receives a 'D' grade for value from Zacks, indicating it is trading at a premium relative to its peers. This combination of factors culminates in a Zacks Rank #3 (Hold), signaling that the stock is expected to perform in line with the broader market in the near term.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mixed

Sentiment Score

0.15

Ticker Sentiment