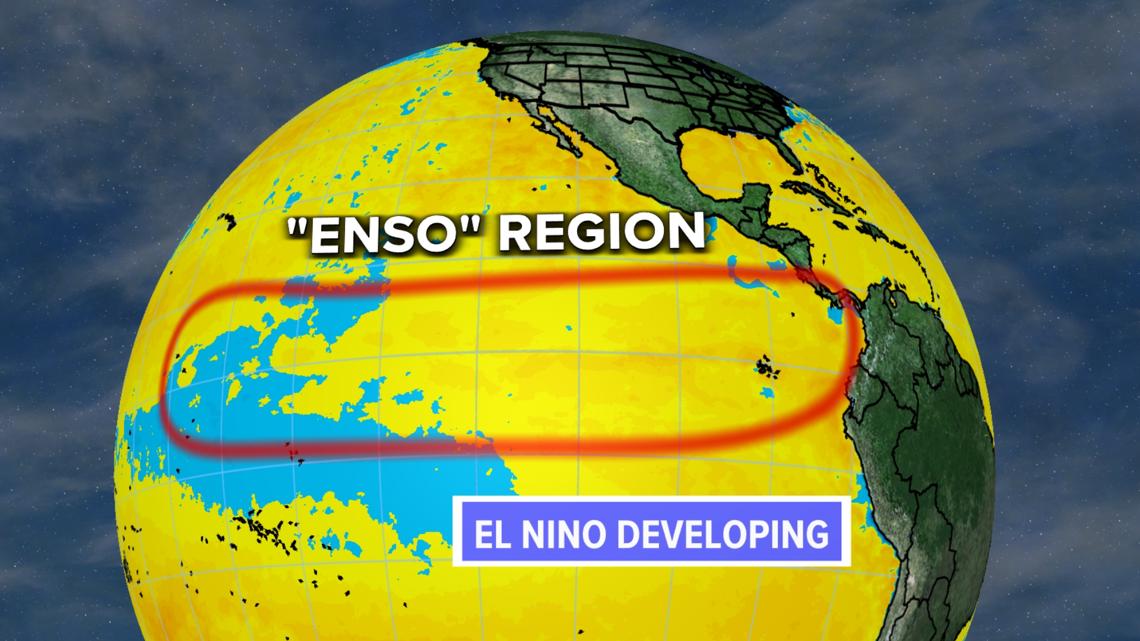

New forecast models and ocean data are pointing to a growing chance of a super El Niño developing later in 2026, with subsurface central Pacific temperatures running up to 6 degrees warmer than average. For Colorado, that would likely raise odds of a more active winter and above-average snow, especially in the southern mountains and the Denver area. The broader U.S. implications are wetter-than-normal conditions across the southern tier, but the outlook remains uncertain and is not guaranteed.

The market implication is not the weather headline itself but the lagged inflation mix: a stronger Pacific jet tends to raise near-term odds of softer domestic heating demand while increasing probability of winter storm volatility and localized freight disruption. That combination is usually bullish for insurers with disciplined catastrophe reinsurance, but more important for us, it can create a temporary dislocation in groups tied to winter operating costs, retail foot traffic, and last-mile logistics. The key is that the economic impact shows up with a 1-2 quarter lag through gas, electric load, airline disruption, and ag inputs rather than as a same-day macro trade.

The second-order winner is likely not just regional utilities but anyone with winter option value embedded in pricing power: natural gas storage operators, snow removal/salt suppliers, and select rail/intermodal names can see margin support if a colder, stormier pattern increases service interruptions and road-clearing demand. The losers are higher fixed-cost consumer businesses with weather-sensitive traffic and less ability to pass through elevated utility bills quickly. In commodities, the biggest opportunity may be in gas and refined products volatility, because a Super El Niño can be bearish for heating demand on balance but bullish for basis blowouts and short-term inventory swings.

The consensus risk is overfitting historical analogs. Strong El Niños do not translate linearly into U.S. snowfall or commodity outcomes, and the real trade is in probability distribution widening, not a one-way snow thesis. If the signal weakens into late summer, the market will likely unwind any early pricing of winter scarcity; if it strengthens, the rerating window opens before peak hurricane/winter risk premiums are embedded, giving us an edge in the autumn rather than mid-winter.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.15