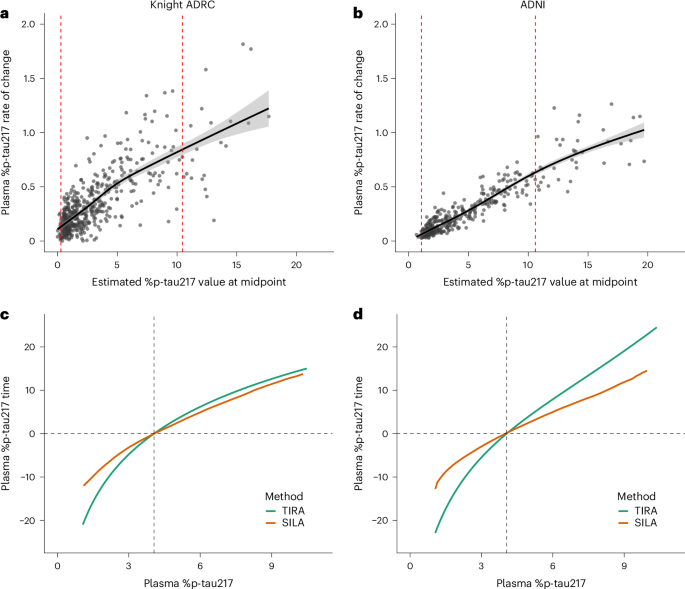

Researchers developed plasma p‑tau217 “clock” models (TIRA and SILA) using longitudinal data from Knight ADRC (clock cohort n=258) and ADNI (clock cohort n=345) to estimate age at biomarker positivity and predict symptomatic Alzheimer’s onset. Estimated age at %p‑tau217 positivity correlated with age at symptom onset (adjusted R2 range ~0.337–0.612) with median absolute error ~3.0–3.7 years; Cox models showed discrimination (C‑index ~0.73–0.79). Findings generalize across multiple commercial p‑tau217 assays (including FDA‑cleared Fujirebio Lumipulse components and C2N PrecivityAD2) and imply a single blood test could improve selection/timing for prevention trials, though applicability is limited to a defined biomarker range (1.06–10.45%) and has important age‑dependent and generalizability caveats.

Market structure: High‑accuracy, low‑cost plasma p‑tau217 clocks (MdAE 3–4 years; positivity window 1.06–10.45%) materially expand screening throughput for AD trials and will directly benefit assay vendors and high‑throughput lab platforms (Quanterix/QTRX, Fujirebio, ALZpath, C2N ecosystem) and large pharmas running anti‑amyloid/tau programs (BIIB, LLY, ABBV, TAK) by lowering enrollment timelines and per‑patient screening cost. Incumbent imaging players (GE HealthCare) and PET‑centric service providers face demand erosion for screening scans; we estimate a meaningful share (>20% of trial screening PETs) could shift to blood tests within 12–36 months, pressuring pricing power for imaging centers. Risk assessment: Key tail risks are regulatory/payer pushback (CMS/FDA coverage and appropriate‑use guidance within 3–12 months), assay reproducibility across diverse ancestries, and IP/legal disputes among assay makers — any of which could delay adoption and cause >30% drawdowns in diagnostics vendors. Short horizon (days–months): press releases, assay clearances and pharma partnerships will move stocks; medium (6–18 months): CMS/FDA guidance and trial enrollment metrics; long (2–5 years): uptake across clinical practice and durable PET volume declines. Hidden dependency: diagnostic value creation is contingent on pharma trial success — better screening only monetizes if therapies prove effective. Trade implications: Favor long exposure to QTRX (diagnostic platform) and selective large pharmas with broad AD franchises (BIIB, LLY, ABBV, TAK) via modest long positions and structured call spreads to time regulatory/trial catalysts over 6–24 months; tactically underweight/hedge GEHC exposure to imaging hardware. Implement pair trades (long QTRX, short GEHC) and buy 9–18 month call spreads on BIIB/LLY sized 1–2% NAV to capture accelerated readouts while capping downside; consider 6–12 month puts on GEHC sized 0.5–1% NAV for insurance. Contrarian angles: Consensus understates that clocks are only validated within a biomarker window and have MdAE 3–4 years, so immediate clinical adoption for individual decision‑making is unlikely — adoption will be staged (trials → specialty clinics → general practice) over 12–36 months, creating a multi‑year alpha runway. The market may be underpricing the optionality that widespread blood screening provides to accelerate trial timelines (raising probability of success and shortening time‑to‑peak sales for successful drugs), which is a second‑order uplift to large-cap AD drugmakers; conversely, diagnostics margins may compress rapidly if assays commoditize, favoring platform owners over reagent specialists.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment