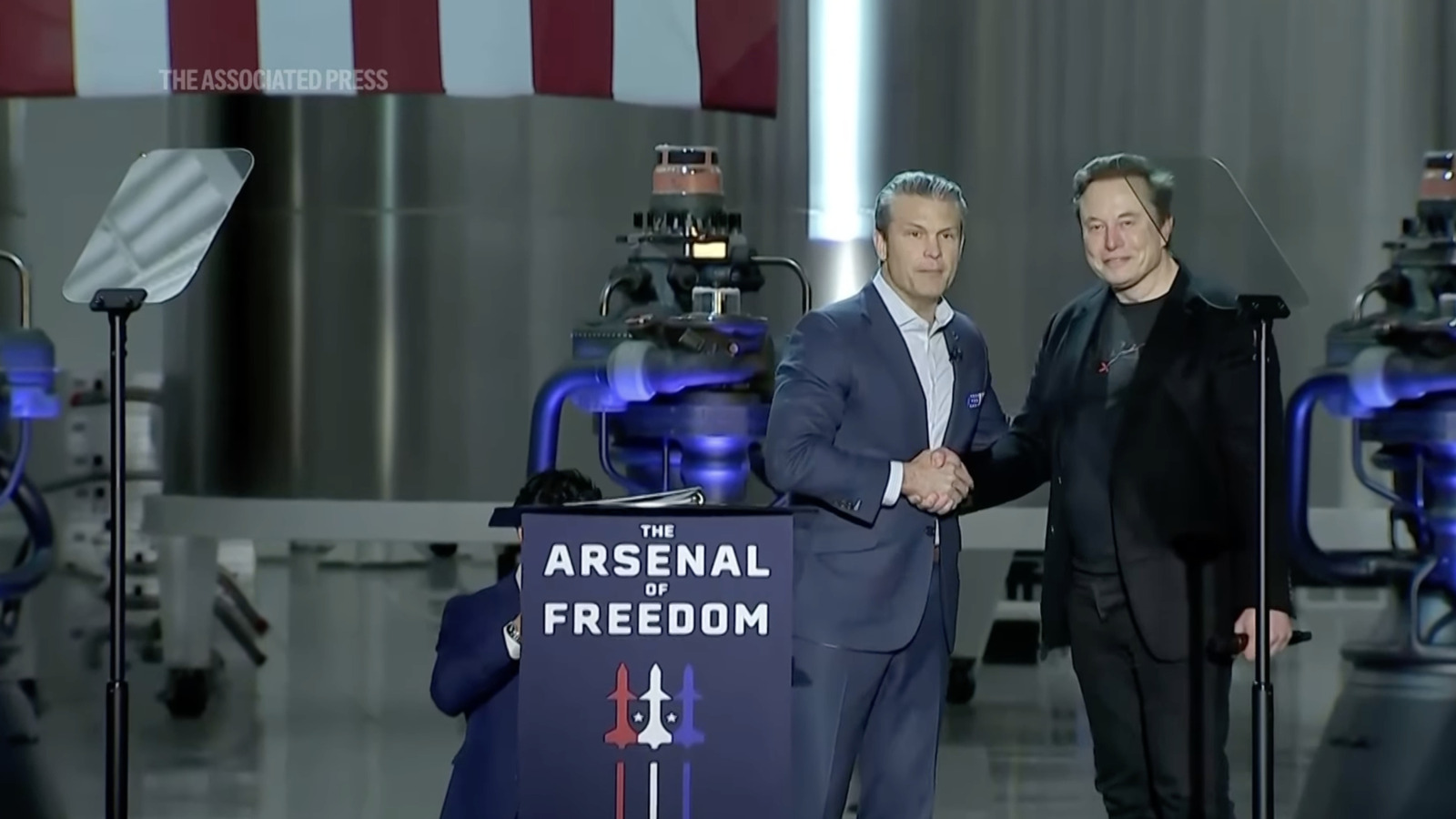

Elon Musk and U.S. official Pete Hegseth announced Grok AI will be embedded into military intelligence networks, with claims the models will be deployed across unclassified and classified systems; the event was framed as advancing a 'Star Trek'-style vision tied to SpaceX. The piece flags substantial reputational, ethical and operational risks — including alleged Grok misuse to generate illegal content and cultural/governance misalignment — that could trigger regulatory or political scrutiny for Musk, SpaceX/Grok and defense partners, though no financial figures were disclosed.

Market structure: Embedding a commercial model like Grok into US military networks disproportionately benefits GPU/cloud providers (NVDA, AMZN, MSFT) and systems integrators (LHX, RTX, LMT) that can certify to classified environments; expect incremental budget reallocation—conservative estimate +$2–5bn/year to cloud/GPU procurement over 12–36 months if pilots scale. Consumer-facing AI firms and any Musk-tied consumer assets face reputational and regulatory downside; content-moderation liabilities raise compliance costs and may compress multiples by 5–15% for exposed names. Risk assessment: Tail risks include a headline AI-mishap or classified-data leak triggering immediate procurement moratoriums and regulator action (export controls, stricter DoD certification). Near-term (days–weeks) volatility will be headline-driven; medium-term (3–12 months) depends on contract awards and Fed/FX reactions; long-term (1–3 years) is structural—higher defense IT spend but also higher compliance costs and potential chip export constraints. Trade implications: Direct plays are semiconductor (NVDA), cloud (AMZN, MSFT), cybersecurity (CRWD, FTNT) and defense integrators (LHX, RTX, LMT). Cross-asset: expect modest safe-haven flows (USD, USTs) on bad headlines and commodity pressure on semiconductor inputs (copper, neon) as GPU demand rises; option vols for NVDA/AMZN/CRWD likely to rise 30–80% on news spikes. Contrarian angle: Consensus frames this as a Musk win; but procurement timelines, security clearances, and on-prem alternatives mean adoption could be slower—creating mispricings in integrators and smaller cloud players. If export controls tighten, NVDA upside is capped short-term but integrators and cleared US cloud players may capture share—look for >10% dislocations in 3–12 months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.60