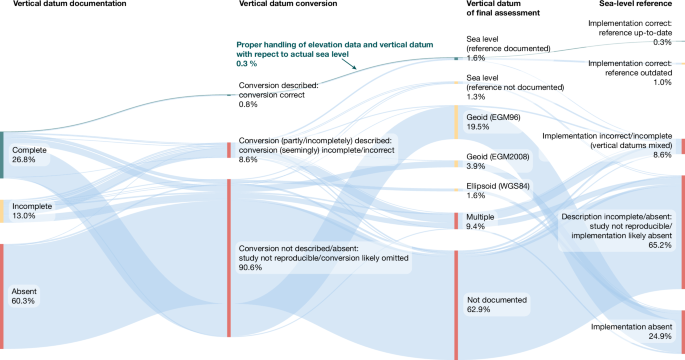

A systematic review of 385 coastal-hazard studies finds pervasive methodological errors: more than 99% mishandled sea-level and land-elevation alignment and ~90% assumed geoid-based sea level instead of measured sea-surface height. Measured mean dynamic topography exceeds common geoid assumptions by a global average of ~0.27 m (EGM96) and ~0.24 m (EGM2008), locally exceeding 1 m in key Global South regions; correcting for this raises land exposed under a 1 m relative sea-level rise by 31–37% and population exposure by 48–68% (to ~77–132 million people), implying material upward revisions to coastal adaptation, insurance, real-estate exposure and climate-finance liabilities.

Market structure: The Nature paper materially raises the physical-risk baseline — global meta-results imply 31–37% more land and ~48–68% more people (77–132m) exposed under 1 m RSLR, with Southeast Asia facing up to +94% area and +96% population. Winners are firms supplying geospatial/MDT/LiDAR, flood‑defense engineering, pumps and water management (data + capex); losers are coastal residential real‑estate, regional property insurers/reinsurers and sovereigns with delta exposure. Expect a multi‑year reallocation of capex from new coastal development to adaptation and data services, shifting pricing power toward specialist engineering and geospatial vendors.

Risk assessment: Near term (0–3 months) market reaction will be muted but informational — the key catalyst is reinsurance renewals (Jan) and IPCC/reporting updates (3–12 months). Tail risks include litigation and accelerated sovereign credit stress in vulnerable deltas (Vietnam, Bangladesh) and a rapid insurance repricing event (>10–20% rate shocks at renewal) that could impair regional carriers’ solvency. Hidden dependencies: widespread reliance on flawed DEMs means many portfolios and muni/RE exposures are mispriced; a policy shock (large adaptation spending or mandatory disclosure) would re-rate multiple sectors quickly.

Trade implications: Buy exposure to geospatial/data + adaptation contractors and water infrastructure; underweight coastal REITs and EM delta sovereigns; use options to express convexity (long calls on vendors, puts on exposed insurers/REITs). Time the moves around two catalysts: (a) next 3–6 month reinsurance renewals and (b) 6–12 month IPCC/agency re‑assessments — these are likely windows for repricing and new capital flows.

Contrarian angles: The market may underreact because this is a methodological shock (data‑driven) rather than a weather event; conversely adaptation spending could be larger than priced in, making some coastal assets safer if governments underwrite protection. Historical parallel: post‑Katrina insurance repricing led to outsized gains for infrastructure contractors. Risk of overpaying for adaptation names exists if governments centralize procurement — seek names with recurring data/maintenance revenue rather than one‑off construction exposure.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.40