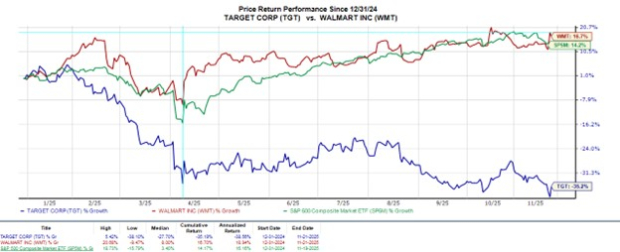

Walmart outpaced Target in Q3 results and guidance: Walmart reported sales up 6% YoY to $179.49 billion and EPS of $0.62 (vs. $0.61 est.), and raised fiscal-2026 net sales growth to 4.8%–5.1% and full-year operating income growth to 8.5%–9.5%, while Target posted EPS of $1.78 (vs. $1.76 est.) but sales slipped just over 1% to $25.27 billion and it trimmed the top end of FY26 EPS to $7.00–$8.00 from $7.00–$9.00, providing no revenue guidance and flagging weakness in discretionary categories offset by strength in food, beverage and digital. Analysts’ EPS revisions now favor Walmart—FY26/FY27 estimates point to modestly higher multi‑year earnings growth—whereas Target faces a material decline from FY25 and recent downward revisions. Zacks maintains both at a Hold (Rank #3), with Walmart’s stronger beat and upgraded outlook implying greater potential upside while Target’s cautious stance clouds its near-term rebound prospects.

Walmart and Target both beat Q3 consensus EPS, but the underlying pictures diverge: Walmart reported Q3 sales of $179.49 billion (up 6% YoY) and EPS of $0.62 versus $0.61 est., while Target posted EPS of $1.78 versus $1.76 est. with sales down just over 1% YoY to $25.27 billion and missing estimates of $25.35 billion. Walmart’s print built on its global e-commerce expansion and a modest sequential EPS improvement from $0.58 a year ago; Target’s EPS declined from $1.85 a year ago and management cited affordability pressures and weaker discretionary traffic. Walmart raised fiscal-2026 net sales growth guidance to 4.8%–5.1% (from 3.75%–4.75%) and lifted full-year operating income growth to 8.5%–9.5% (nearly +400 bps), while Target trimmed the top end of FY26 EPS to $7.00–$8.00 from $7.00–$9.00 and issued no revenue guidance. Consensus-model moves favor Walmart — FY26/FY27 EPS estimates show modest multi-year growth for Walmart versus a projected 17% EPS drop for Target from FY25 and recent downward revisions. Zacks retains both at a Rank #3 (Hold), reflecting that Walmart’s beat and upgraded outlook create greater upside potential, whereas Target’s cautious commentary, discretionary softness, and lack of revenue guidance increase execution risk through the holiday season.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mixed

Sentiment Score

0.05

Ticker Sentiment