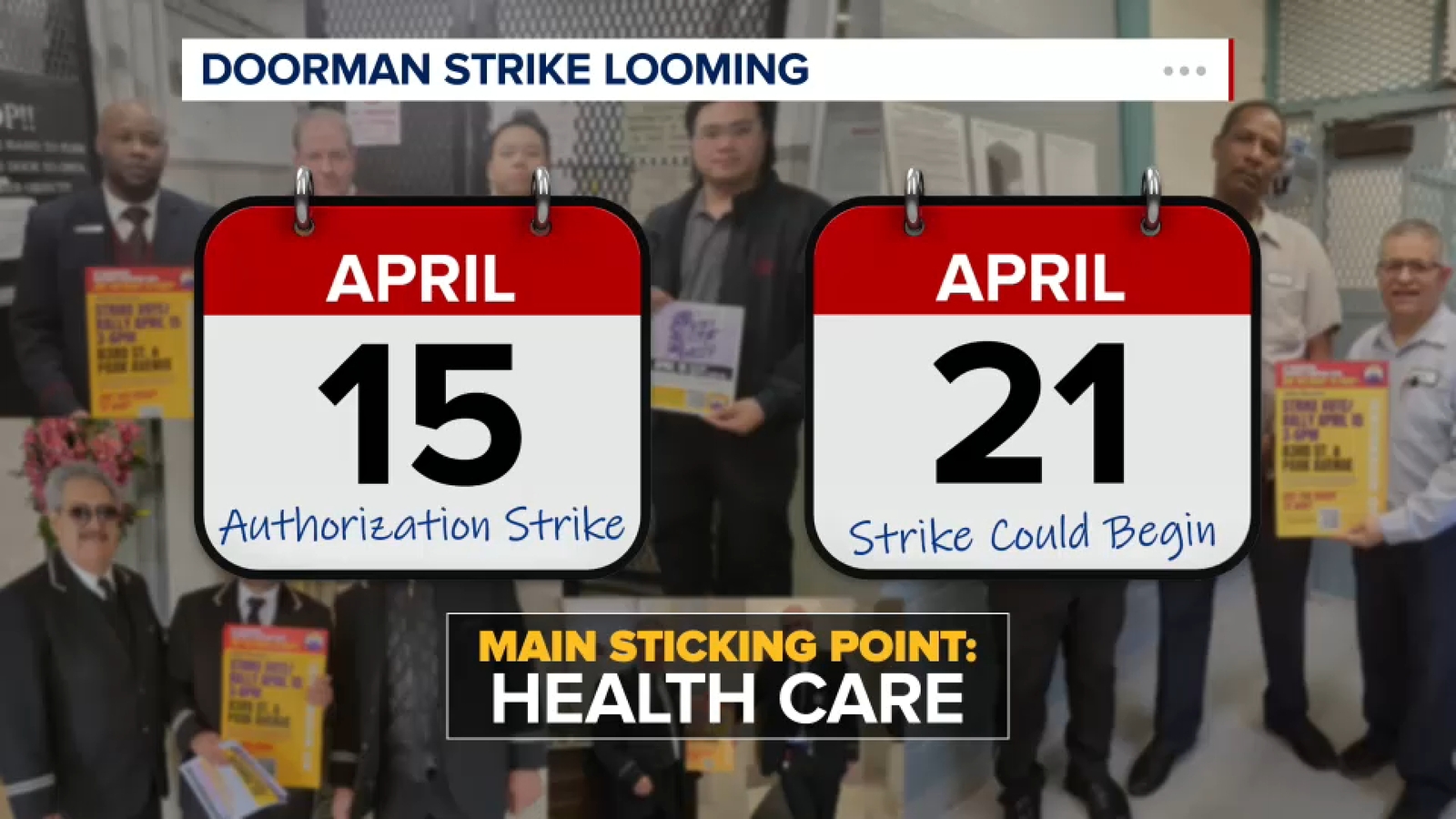

More than 34,000 New York City residential building workers could strike as early as next Tuesday if no contract agreement is reached, following a Wednesday vote to authorize a walkout. Key sticking points include wages, pensions, a proposed Tier II structure, and healthcare, with the Realty Advisory Board arguing current costs are unsustainable. The last similar strike was in 1991 and lasted 12 days, raising the risk of temporary disruption across roughly 3,500 buildings.

The immediate market impact is less about direct equity exposure and more about operational fragility in New York housing. A strike would disproportionately hit Class A/co-op and rental assets with high service intensity, and the real economic damage comes from a rapid deterioration in tenant satisfaction, move-ins, and discretionary amenity spend rather than a simple payroll interruption. That creates a short-duration but sharp revenue risk for landlords with concentrated NYC exposure, especially those already facing weak rent-stabilized economics and elevated refinancing pressure.

Second-order effects matter more than the headline labor dispute. If building staff coverage becomes inconsistent, insurance claims, maintenance backlogs, and compliance costs can rise quickly, while turnover in high-end rental buildings can accelerate as residents reprice the value of service. Vendors tied to residential property operations—handyman contractors, security, cleaning, and temporary staffing—could see a near-term bump, but that is usually offset by margin pressure and lower renewal rates if the work stoppage lasts beyond a week.

The key catalyst window is days, not months: a strike authorization is a credible signal because residential labor disputes tend to resolve only when both sides see a measurable disruption to building operations. The longer-dated risk is that a new contract with higher wages and/or benefit contributions becomes a permanent cost reset for NYC multifamily owners, which could worsen cap rates for labor-intensive portfolios and make the market more skeptical of net operating income growth in the city. Conversely, a fast settlement would likely fade the event quickly, leaving only a modest cost increase and little broader read-through.

The contrarian view is that the market may be overestimating the systemic risk and underestimating management adaptability. Many buildings can triage operations for several days using resident cooperation and temporary labor, which limits the odds of a broad financial shock; the bigger story may be a one-time re-rating of operating expenses rather than a structural impairment. That said, if the dispute extends past a week, expect a meaningful change in bargaining power that could reverberate through rent negotiations and asset underwriting for the next several quarters.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25