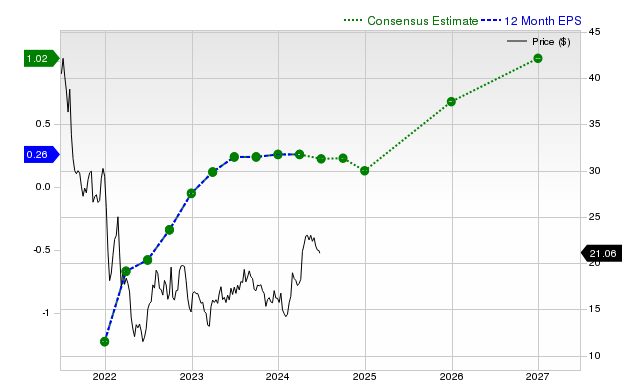

Coupang (CPNG) has recently outperformed the market with a 13.4% gain over the past month, but carries a Zacks Rank #4 (Sell) primarily due to projected year-over-year EPS declines of 33.3% for the current quarter and 22.7% for the current fiscal year. While revenue growth is forecast to exceed 15% for the next two fiscal years and EPS is expected to rebound significantly in the following fiscal year, the stock's valuation is graded D, suggesting it trades at a premium to peers and may underperform in the near term.

Despite strong recent share price performance, with a 13.4% gain over the past month that significantly outpaced the S&P 500, Coupang (CPNG) presents a mixed fundamental picture. The primary concern is near-term profitability, as consensus estimates project a 33.3% year-over-year decline in EPS for the current quarter and a 22.7% decline for the current fiscal year. This is underscored by the last reported quarter, where a substantial EPS miss of -71.43% overshadowed a 1.37% revenue beat. In contrast, top-line growth remains robust, with sales forecast to grow over 15% in both the current and next fiscal years. The long-term outlook appears more favorable, with a projected EPS surge of 247.1% for the next fiscal year. However, the combination of stagnant near-term earnings estimates, a premium valuation indicated by a Zacks Value Style Score of 'D', and the recent earnings miss has resulted in a bearish Zacks Rank #4 (Sell), suggesting a risk of underperformance in the near term.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.40

Ticker Sentiment