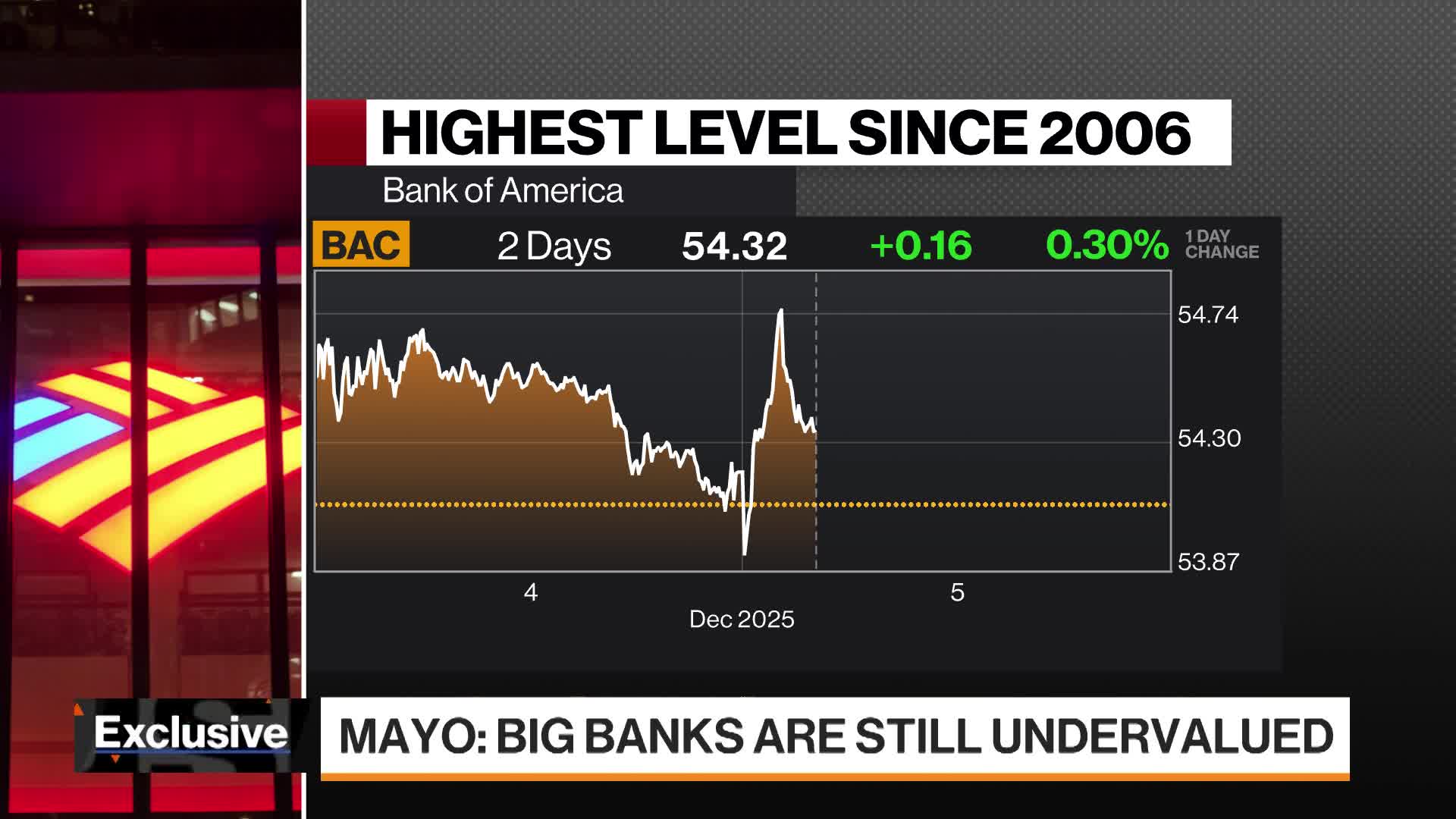

The commentary argues US banks are in a rerating phase akin to mid-1990s deregulation, with large-cap bank P/E multiples having moved from ~10x to ~12–13x and the potential to reach ~15x while the broader market trades above 20x. Valuations look inexpensive versus peers on returns-to-book metrics, and a projected multi-year EPS inflection from recent negative growth to positive over the next three years is driving renewed institutional interest and incoming investor engagement.

Market structure: Deregulation and higher rates disproportionately benefit large, diversified US banks (JPM, BAC, USB) and asset managers via wider NIMs and fee income, while regional banks and balance-sheet-light fintechs are losers due to deposit flight and concentrated CRE exposure. Expect a 25–35% relative re-rating potential if big banks move from ~12x to ~15x forward EPS within 12–24 months; that’s multiple expansion rather than a pure earnings surprise. Competitive dynamics favor scale (stable low‑cost deposits, trading, capital markets) and punish firms reliant on wholesale funding or concentrated CRE/office loan books. Supply/demand: loan demand for corporate credit and mortgages should absorb increased capital supply, but legacy AFS bond markdowns create a near-term supply of shares from cautious holders. Risk assessment: Tail risks include a regulatory reversal, systemic deposit runs (>5% rapid outflows for exposed regional banks), or a CRE shock that forces >200bps of loan-loss provisions across regionals — any would wipe out rerating. Immediate (days) risks are sentiment-driven spikes and volatility; short-term (weeks–months) hinge on Fed decisions and upcoming earnings; long-term (3–24 months) depends on actual EPS recovery and realized NII expansion (we model +50–100bps NIM benefit as plausible). Hidden dependencies: unrealized AFS losses, repo access, and counterparty exposure to hedge funds. Catalysts: Senate/House deregulation votes, Fed minutes, and bank Q4/Q1 earnings guiding NII/loan-loss trajectories. Trade implications: Tactical overweight financials (large-cap) while hedging regional exposure — long JPM/BAC and short KRE/KBE is a robust relative-value stance; for equities size initial allocations small (2–4% each) and scale into confirming NII/EPS beats. Options: use 9–15 month call spreads on large banks to lever rerating (limited-cost LEAP call spreads) and sell OTM puts to collect premium where capital allows; buy protective put spreads on regionals to cap downside. Rotate 2–4% gross from growth/capex names into XLF/KBE over 3–6 months if inflation stays sticky and rates remain elevated. Contrarian angles: Consensus overlooks duration losses in banks’ securities books and the political risk of partial deregulation that increases long-term funding costs; the mid‑1990s parallel is useful but not identical — today’s CRE and mark-to-market debt make regionals more fragile. The market may be underpricing a steady 15x rerating for the majors but overpricing recovery for regionals; mispricings favor long-large-cap/short-regional pairs. Unintended consequences: deregulation could boost ROE short-term yet raise systemic risk premiums, leading to episodic volatility and higher equity capital costs later, so size and hedges must reflect convexity.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.50