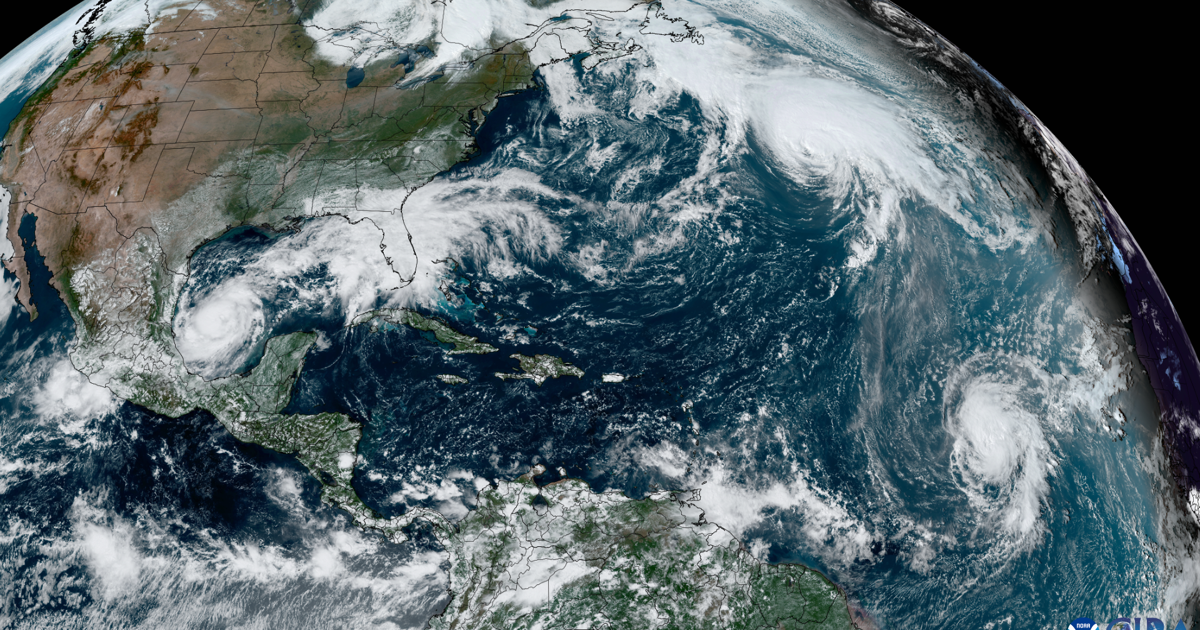

CSU forecasts 13 named storms, six hurricanes and two major hurricanes for the upcoming Atlantic season (vs. historical averages of 14/7/3). The team assigns a ~32% chance of a major hurricane hitting the U.S. coastline (20% Gulf, 15% East Coast, 35% Caribbean) and roughly a 28% chance a hurricane will come within 50 miles of Louisiana (10% for a major). Forecasters point to a high likelihood of El Niño (CPC: 61% chance May–July) suppressing activity, but mixed Atlantic SSTs and the early-April timing make the outlook uncertain; updates are due June 10, July 8 and Aug. 5.

A higher probability of El Niño compresses tail volatility for Atlantic landfall risk, which should translate into a measurable compression in cat-loss expectations across P&C carriers and reinsurers over the coming 3–12 months. That compression is not linear: much of the benefit will accrue to market participants that took elevated reserve positions or bought expensive retrocessional cover last year — they stand to release capital or let maturing hedges lapse, boosting near-term ROE. Second-order winners include insurers and reinsurance capital allocators who can redeploy freed capital into buybacks or higher-yielding spread products; losers include specialist storm-recovery contractors and building-material suppliers whose extraordinary post-storm demand is episodic and will likely undershoot consensus in a quiet year. Municipalities and utilities along the Gulf/Atlantic may delay costly resilience capex if perceived risk falls, creating a multi-quarter deferment in ESG-related infrastructure spending that could ripple to engineering firms and bond issuance schedules. Tail risk remains asymmetric: anomalously warm Atlantic SSTs or a late-season rapid intensification event can erase the premium compression in weeks, so the principal market catalyst to watch is the evolution of vertical wind shear and basin SST gradients through late spring into August. The optimal tactical window for positioning is the narrow late-spring / early-summer period when ENSO signals crystallize and market-implied hurricane volatility (cat bond spreads, catastrophe reinsurance front months) begins to reprice. Consensus underappreciates that a quieter Atlantic shifts incremental risk to liquidity- and capacity-sensitive instruments (ILS/cat bonds, retro cover) rather than to headline insured-loss exposure; that implies the biggest tradable move is in spreads and fees (reinsurance renewal pricing and cat-structured product yields) rather than in headline insurer P&L, which is already largely priced for normalization.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00