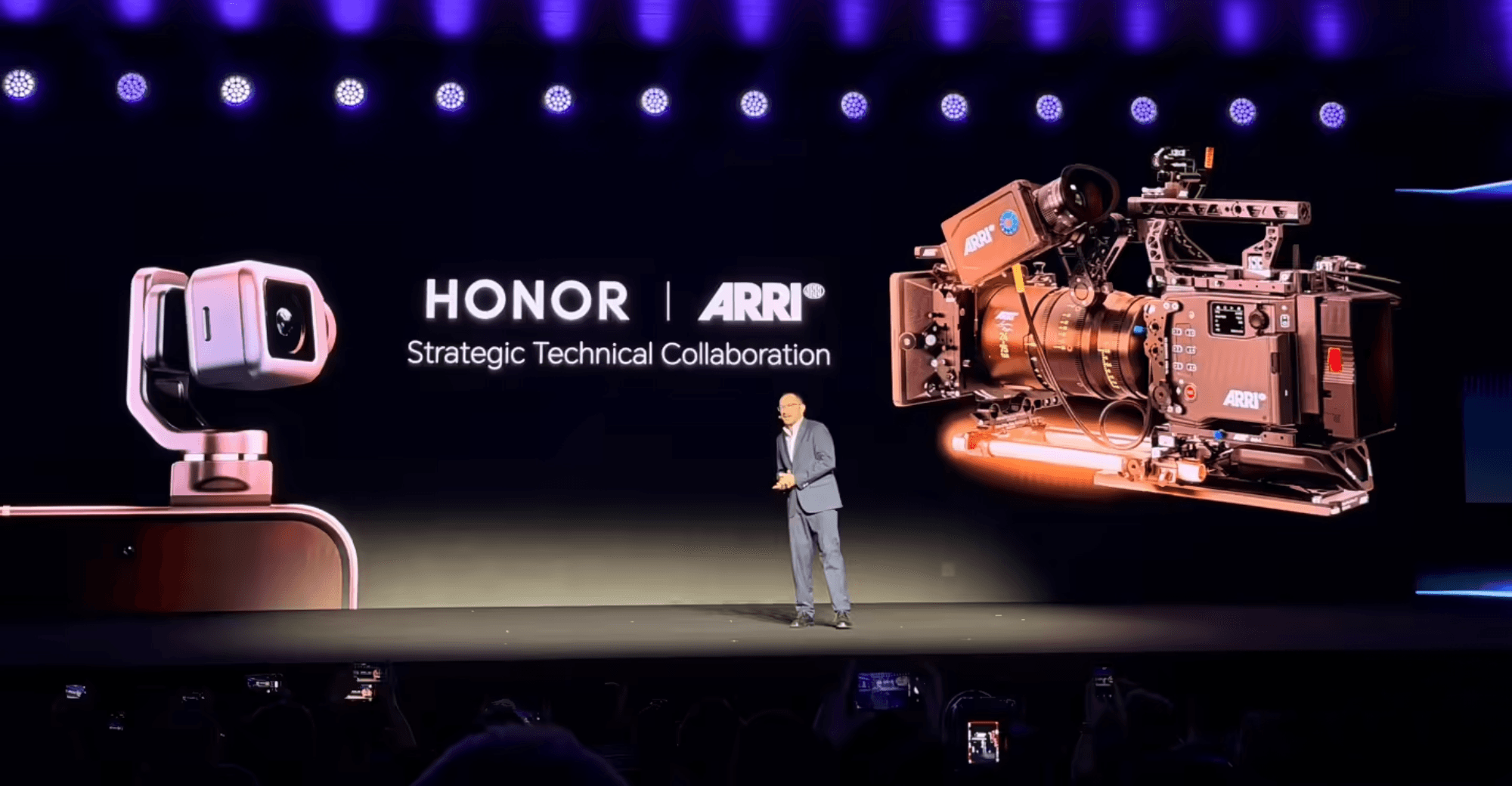

Honor has entered a partnership with cinematography-equipment maker ARRI to bring ARRI-grade cinematic imaging capabilities to its Robot Phone, positioning the handset as a premium mobile video-capture offering. The collaboration is aimed at differentiating Honor in the competitive smartphone market by enhancing creative video features, which could aid consumer appeal and brand positioning but is unlikely to have a material near-term impact on Honor's financials.

Market structure: Honor’s ARRI tie-up raises the bar for premium computational imaging in China’s mid-to-high smartphone tiers, favoring sensor/ISP leaders (Sony - SONY, Qualcomm - QCOM) and premium lens suppliers (Largan Precision - 3008.TW). Apple (AAPL) and Samsung (005930.KS/SSNLF) face modest share pressure in China/EMs but pricing power is unlikely to move more than ~100–200bp over 12 months; component suppliers should see a 3–8% revenue uplift if adoption scales.

Risk assessment: Tail risks include regulatory export limits on cinematic-grade sensors or motion-imaging IP within 30–180 days, and operational failure if ARRI-branding is perceived as marketing-only (low conversion). Short-term (days-weeks) this is a PR event; medium (3–9 months) impacts on supply chain orders; long-term (1–3 years) it can shift AR margins for imaging suppliers if it drives sustained ASP increases of $10–$50 per device.

Trade implications: Favor long exposures to public imaging nodes: SONY (sensors), QCOM (ISPs/SoCs), and 3008.TW (lenses), using 3–5% position sizing per name, executed over 2–8 weeks to capture order cycles. Use 3–9 month call spreads to express upside while capping premium; trim AAPL longs by 1–2% in Asia-exposed sleeves and rotate into semiconductor suppliers.

Contrarian angles: Consensus conflates cinematography branding with mass-market utility — adoption may be niche and drive only 1–3% unit premium; hype could be overdone. If ARRI’s role is limited to co-marketing, suppliers’ order growth will disappoint; position sizes should be calibrated to a 20–30% probability of disappointment and protected with options or stop-losses.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.25