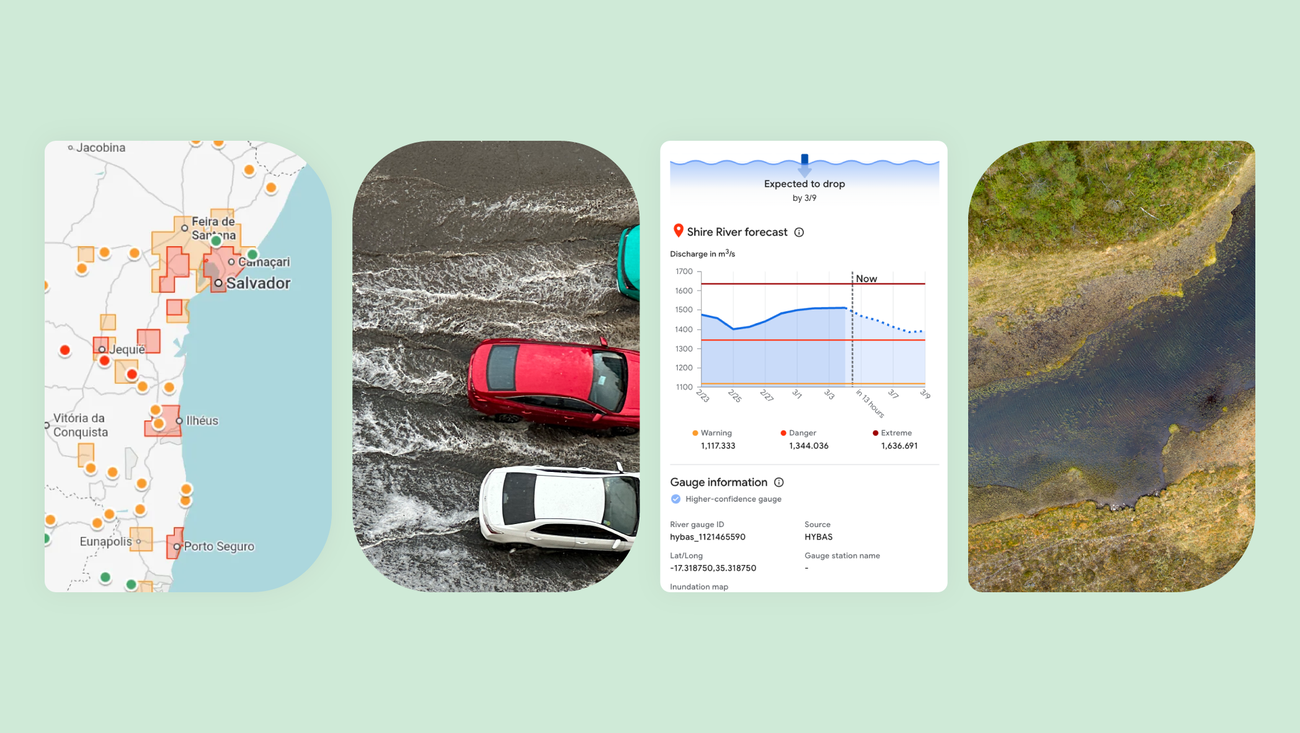

Google announced Groundsource, an AI methodology that used Gemini and Google Maps to identify over 2.6 million historical flood events across more than 150 countries to create an urban flash-flood dataset. Using this data Google trained a model that forecasts urban flash floods up to 24 hours in advance and added these forecasts to its Flood Hub alongside riverine forecasts that currently cover ~2 billion people. The dataset and model are being released as an open benchmark to help partners and researchers scale urban flood preparedness and extend the approach to other disasters.

This product should be read as an enterprise/government sales accelerant more than a consumer feature: the marginal value is in licensing verified, geo-indexed event histories into insurance, emergency management, and urban planning workflows. Expect a measurable sales cadence shift over 6–24 months as cities and reinsurers pilot live integrations; those pilots drive high-margin GCP workload growth and recurring data revenue rather than a one-off ad uplift.

Second-order winners include GPU and infrastructure suppliers that support large-scale retraining and inference (multi-quarter to multi-year demand for specialized silicon and storage), plus incumbents that can bundle resilience data into existing software-as-a-service contracts. Conversely, proprietary catastrophe model vendors face credible disintermediation risk in urban flash-flood niches: if public, validated datasets become the new benchmark, pricing power for bespoke historical data could compress materially over 12–36 months.

Key tail risks: a high-profile false-negative or legal challenge on data provenance/privacy would rapidly slow municipal procurement and invite regulation — that’s a 0–18 month catalyst that could flip the narrative. Competitive response from hyperscalers or well-funded niche startups is likely and fast; the decisive metric to watch is signed enterprise contracts (NDA-to-deal conversion) and incremental GCP bookings tied to resilience services over the next four quarters.

On valuation framing, incremental recurring data + GCP cross-sell of even 0.5–1% of Alphabet’s revenue base implies sizeable upside to FCF over 2–3 years, but realize monetization and regulatory risk create asymmetric near-term upside and require option- or pair-structured exposure rather than simple outright long exposure.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.35

Ticker Sentiment