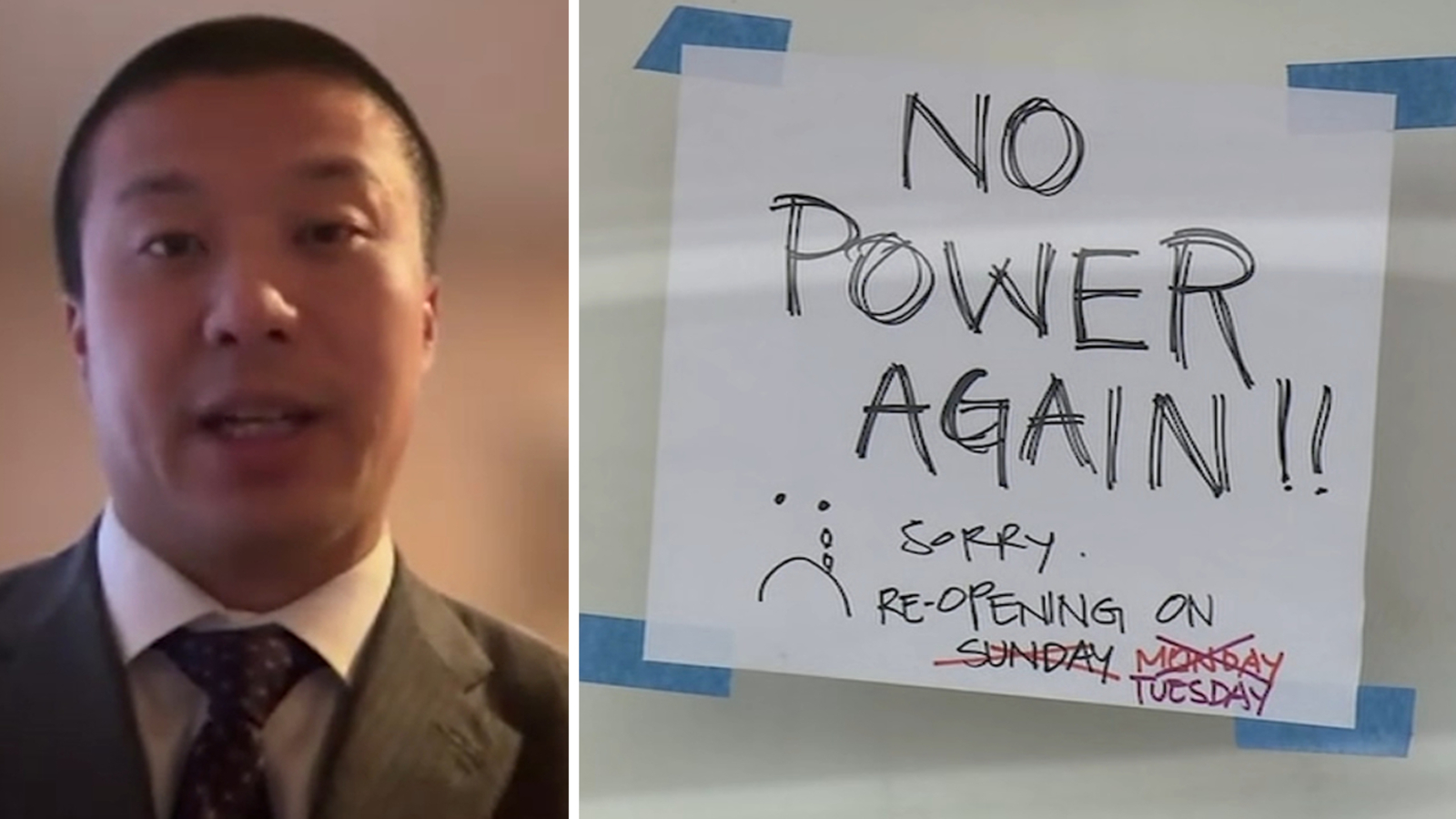

San Francisco experienced multiple prolonged power outages in the Sunset District in December, prompting newly appointed Supervisor Alan Wong to press PG&E for accountability and long-term grid resilience improvements. PG&E has offered a $200 bill credit for impacted residents and up to $2,500 for businesses, with additional reimbursement available via claims; city officials warn the amounts and claims process are inadequate and may disproportionately burden non-English-speaking residents. The episode raises operational and reputational risks for PG&E, potential regulatory scrutiny, and localized economic losses for small businesses that could translate into claims or policy action.

Market structure: Localized long-duration outages in San Francisco crystallize near-term winners — residential/commercial backup vendors (Generac GNRC, Enphase ENPH, Tesla TSLA energy), grid-equipment and controls suppliers (Eaton ETN, ABB ABB, Honeywell HON) — and losers: incumbent utility Pacific Gas & Electric (PCG) and small merchants facing uninsured losses. Expect equipment vendors to see a 5–15% uplift to orderbooks over 6–18 months as municipalities accelerate resiliency capex; PCG faces margin pressure from credits, claims and potential rate actions. Risk assessment: Tail risks include a major wildfire/earthquake triggering >$1bn in incremental liabilities for utilities and accelerated regulatory rate caps or asset restrictions; probability low but impact systemic for PCG and CA muni credit. Near-term (days–weeks) political noise and customer claims process friction; medium-term (3–12 months) CPUC investigations and possible fines; long-term (1–3 years) structural capex programs for hardening the grid. Trade implications: Direct plays favor 6–18 month exposure to backup power and grid-hardening names (buy equities or call spreads on GNRC, ENPH, ETN, ABB) and selective downside on PCG via puts or small outright shorts. Pair trades (long GNRC/short PCG) and defined-risk option spreads mitigate idiosyncratic volatility; monitor CPUC/City hearings as 30–90 day catalysts. Contrarian angles: Consensus will exaggerate utility reputational damage and underprice multi-year vendor backlog from mandated upgrades — equipment vendors may outperform consensus by 10–30% over 12–24 months. Counter-risk: residential backup demand can be front-loaded and political outcomes (rate relief vs capex authorization) will drive winner dispersion; treat positions as event-driven, not permanent buys.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.55