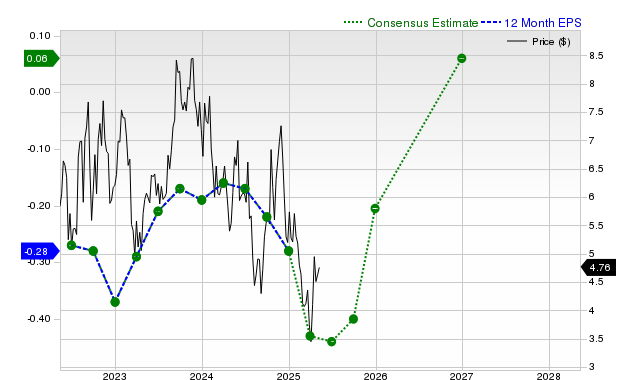

Energy Fuels (UUUU), a uranium and vanadium miner, carries a Zacks Rank #3 (Hold) and a poor Zacks Value grade (F) after large recent estimate revisions: the consensus expects a current-quarter loss of $0.08 (Q/Q change +57.9%) with the 30-day consensus for the quarter down -23.1%, fiscal-year EPS of -$0.35 (-25% YoY) and next fiscal EPS of $0.06 (+81.9%). Revenue consensus for the current quarter is $13.5m (-66.2% YoY), $47.07m for the current fiscal year (-39.7%) and $87.05m for next fiscal (+85%); the company reported last quarter revenues of $17.71m (+337.3%) beating consensus by +79.8% and EPS of -$0.07 (12.5% surprise). Shares have underperformed recently (‑29.8% over the past month), suggesting investor caution despite the recent revenue beat and mixed forward estimates.

Market structure: The selloff in UUUU (-~30% month-to-date) disproportionately hurts small-cap uranium/vanadium juniors with weak balance sheets and premium valuations; larger integrated uranium producers (e.g., CCJ) and utilities buying spot inventories are the indirect beneficiaries as capital re-prices toward scale and counterparty credit. Competitive dynamics favor firms with contracted production and processing capacity — juniors that cannot secure offtake or funding will lose pricing power and market share if spot/contract prices remain volatile. Supply/demand signal: the market is signaling near-term demand uncertainty (consensus revenue -40% year) but a possible recovery next fiscal (+85% revenue estimate) — this implies tight physical markets are expected later, but timing is uncertain and contingent on contract wins and financing ramp-up. Risk assessment: Tail risks include regulatory reversals on nuclear policy, permitting/operational delays, and equity dilution — any one can wipe out common holders (low-probability, high-impact). Time horizons split: immediate (days-weeks) driven by earnings/estimate revisions and funding news; short-term (1–6 months) by contract announcements and uranium spot moves; long-term (12–36 months) by physical supply additions and utility contracting cycles. Hidden dependencies: UUUU’s valuation premium (Zacks F) hides dependency on non-core asset sales, government incentives, or convertible financings; catalysts that reverse trend include US/Europe strategic stockpile purchases or large utility long-term contracts. Trade implications: Direct play — avoid size-heavy outright longs in UUUU unless funded clarity; prefer small, tactical exposures (1–2% portfolio) or higher-quality equivalents (long CCJ). Pair trade — long CCJ / short UUUU to capture quality spread if uranium contracts firm up. Options — use 3–6 month call spreads on UUUU or CCJ for directional upside with defined risk, or buy UUUU 3-month put spreads as hedges if >15% further downside appears. Sector rotation — reduce junior mining exposure and rotate into integrated miners and select utilities with contracted nuclear exposure until funding/cash-flow visibility improves. Contrarian angles: Consensus overlooks that the consensus +85% revenue next fiscal implies discrete contract wins or asset sales — if confirmed, market could sharply re-rate UUUU; conversely, if estimates fall further (another -20–30%), downside is large. The current selloff may be overdone given physical uranium tightness prospects, but only buy after 1) confirmed financing/contract announcement or 2) stock stabilizes with volume-backed base; historical junior uranium rallies are sharp but binary. Unintended consequence: equity raises at distressed levels could dilute existing holders >20–30%, so assume financing risk in any bullish thesis.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25

Ticker Sentiment