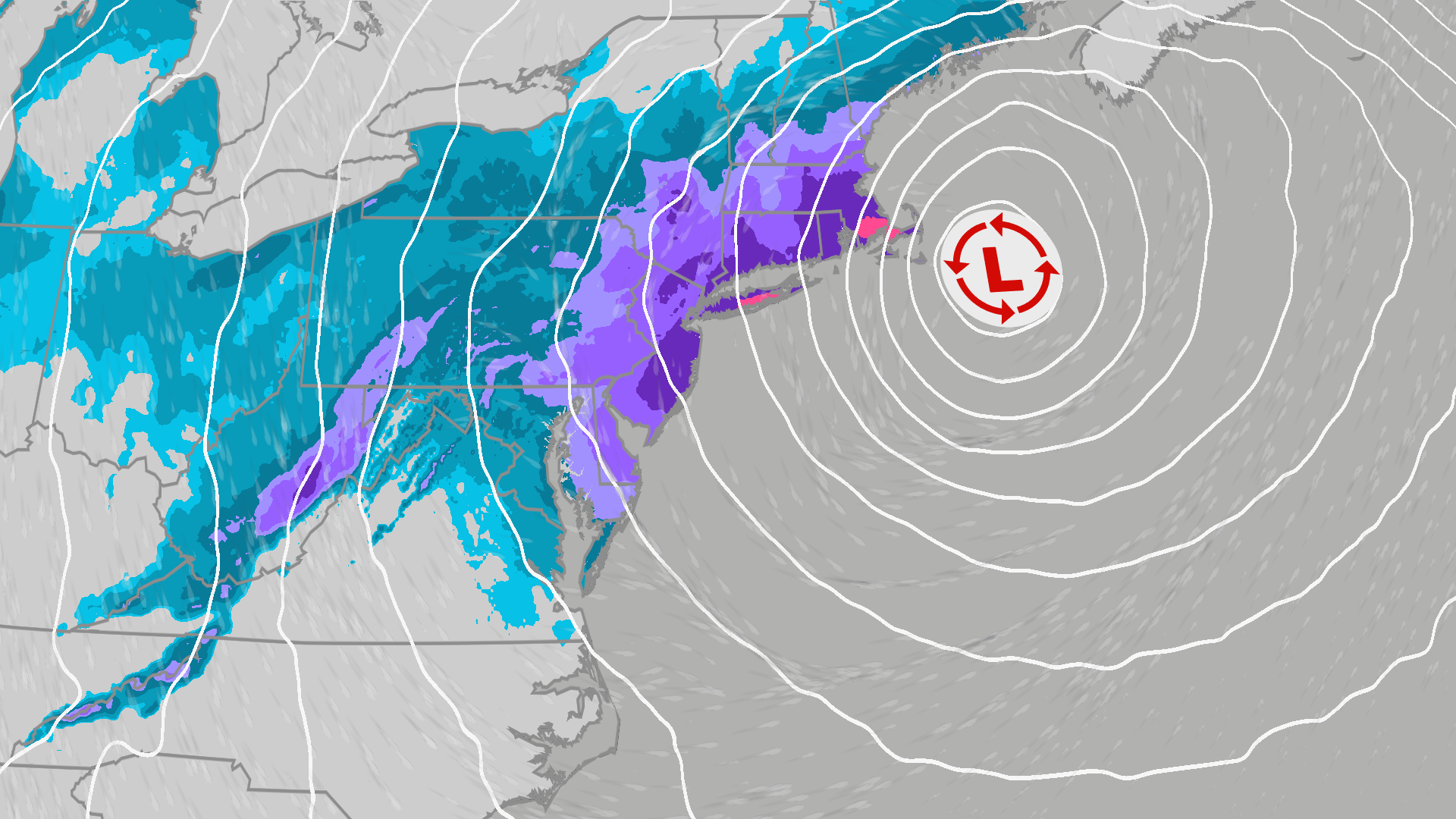

A powerful nor'easter is intensifying into a 'bomb cyclone' across the U.S. East Coast with blizzard warnings from Virginia to New Hampshire; New York City has announced a travel ban effective 9 p.m. and expects roughly 20 inches of snow, while forecasts call for 16–24 inches in many areas and wind gusts up to 70 mph in Boston. More than 15,000 flight delays have been reported nationwide with over 60% of flights into JFK and LaGuardia canceled, and authorities warn of widespread power outages and disruptions to transportation, heightened heating demand and concentrated retail stocking activity—outcomes that pose near-term operational risk to airlines, utilities and regional retail supply chains.

Market structure: Near-term winners are home-improvement retailers (HD, LOW), portable-generator maker Generac (GNRC) and fuel distributors (PSX, VLO) from urgent demand for snow-clearing, heating and backup power; losers are airlines (AAL, DAL, UAL, LUV), airport services and parcel carriers (UPS, FDX) facing cancelled flights and logistics delays. Pricing power is temporary — expect 1–3 week spikes in retail/commodity volumes (salt, diesel, propane) with margin expansion for retailers of ~1–3% if restocking constraints persist. Supply-demand: regional natural gas/propane balancing will tighten in Northeast hubs, likely adding $0.10–0.30/MMBtu to spot prices for 1–2 weeks. Risk assessment: Tail risks include prolonged grid outages (>72 hours) causing sustained retail closures, insurance loss accumulation (>=$1bn regionally) and municipal liquidity strains; these would widen credit spreads for short-dated munis by 10–30bp. Time horizons: immediate (0–7 days) sees travel/logistics disruption and volatility spikes, short-term (1–3 months) captures replacement demand for generators/retail restock, long-term (quarters) minimal structural change absent repeated storms. Hidden dependencies: port closures cascade into supply-chain SKU shortages and create asymmetric inventory drawdowns at regional DCs, amplifying pricing for replacement goods. Trade implications: Direct plays — short airlines and airport services into the next 7–14 days, long HD/LOW and GNRC for 1–12 week demand reversion; open options to monetize volatility (buy puts on JETS/AAL, buy call spreads on GNRC). Cross-asset — buy short-dated NE natural gas futures options and monitor utility outage-related credit moves; consider hedging with investment-grade muni protection if exposure to city revenues exists. Contrarian angles: The market will likely over-penalize airline balance sheets for a weather event; if cancellations normalize within 7 days, intraday panics can be faded — selectively buy airline single-day IV crush plays post-storm. Conversely, retail restocking may be front-loaded and priced in the first 2–3 days, so stagger entry into HD/LOW and prefer call spreads 4–12 weeks out to avoid immediate mean-reversion in sales.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.60