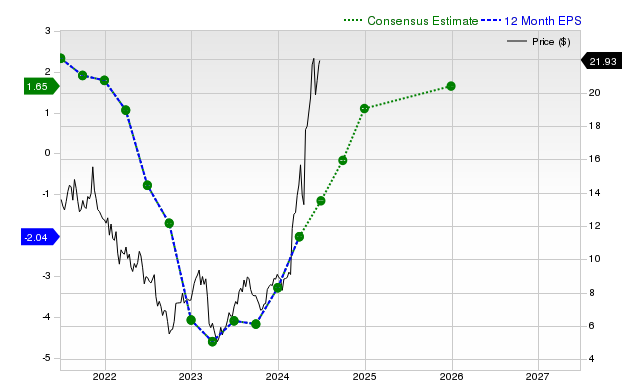

Tutor Perini (TPC) is showing meaningful fundamental improvement with Zacks consensus EPS estimates of $0.92 for the current quarter (+160.9% YoY), $4.01 for the current fiscal year (+228.1%), and $4.72 next year (+17.7%); consensus sales for the quarter are $1.28bn (+19.9%) and fiscal sales estimates are $5.32bn (+22.8%) and $5.98bn (+12.5%). In the last reported quarter the company posted revenue of $1.42bn (+30.7% YoY) and EPS of $1.15 versus -$1.92 a year ago, beating revenue and EPS estimates (+5.34% revenue surprise, +19.79% EPS surprise), and has a Zacks Rank #2 (Buy) with a Zacks Value Style Score of A. These trends in upward estimate revisions and recent beats support a constructive outlook despite the stock's recent month-to-month weakness.

Market structure: TPC’s upward revisions and beat point to strengthening backlog conversion and pricing power in mid-tier US civil/building contracting; beneficiaries include subcontractors, ready-mix/aggregate suppliers and steel/flat-rolled producers (expect +1–3% incremental demand in materials in next 3–12 months). Losers are lower-quality small contractors and margin-levered peers who face tighter bidding dynamics. Cross-asset: positive for lower-tier credit spreads (expect 25–75bps tightening for similarly rated contractors if trend persists), modest upward pressure on construction materials; FX impact immaterial. Risk assessment: Tail risks include large project overruns, contract disputes or single large-bid losses that could swing EBITDA by >20% in a quarter; regulatory changes to public infrastructure funding represent another low-probability high-impact shock. Immediate (days) risk is earnings/guide knee-jerk; short-term (weeks/months) hinge on backlog disclosures and subcontractor cost trends; long-term (quarters) depends on sustained margin expansion and capital allocation. Hidden dependencies: government infrastructure cash flow timing and subcontractor labor availability can compress margins even with rising revenue. Trade implications: Direct long TPC exposure captures upward estimate momentum; consider size-limited exposure with option protection to manage execution risk. Relative trades: TPC vs large diversified peers where mid-tier execution improves share; volatility likely compressed after beats, so use defined-risk option spreads or cash pairs rather than outright long vol. Catalysts to watch: next quarterly report, contract awards disclosures, and monthly housing/infrastructure data within 30–90 days. Contrarian angles: Consensus may be underweight downside from margin reversion — much of EPS upside could be nonrecurring or working-capital timing; the recent month-to-month stock weakness suggests sentiment already discounts risk, creating an asymmetric risk/reward. Historical parallels show midsize contractors can deliver strong cyclical rebounds then falter if backlog quality weakens; position sizing and protective exits are critical.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment