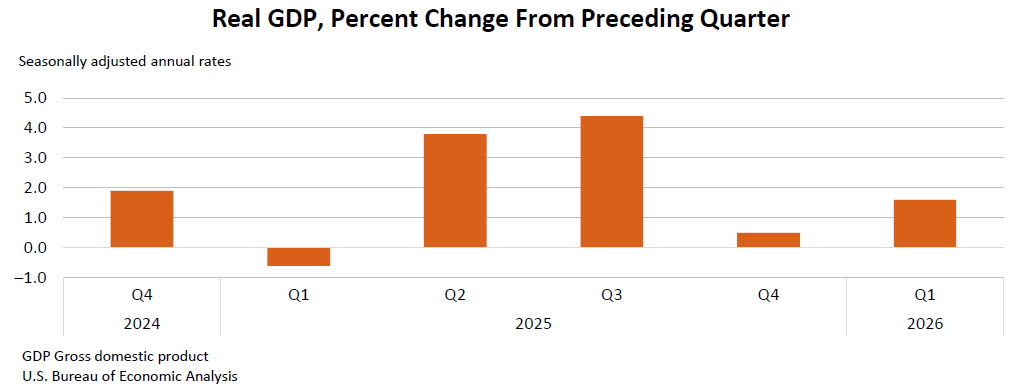

U.S. real GDP grew at a 1.6% annualized rate in Q1 2026, down 0.4 percentage point from the advance estimate and below Q4 2025's 0.5% pace. Growth was supported by exports, investment, consumer spending, and government spending, while the GDP price index rose 3.5% and core PCE inflation came in at 4.4%. Corporate profits from current production increased $40.4 billion, and BEA noted IEEPA tariff refunds do not affect first-quarter GDP.

The composition matters more than the headline: growth is now being held up by external demand and public-sector spending while household demand and private inventory dynamics are softening. That mix typically supports defensives, exporters, and selected industrials, but it is a poor backdrop for broad cyclicals because it implies less self-sustaining domestic momentum heading into the next few months.

The inflation details are the real macro signal. Core services re-acceleration alongside still-elevated headline price pressure argues that the Fed’s policy easing path remains constrained, even if real activity is decelerating. That combination is usually bearish for duration-sensitive equity segments and credit risk because growth is not weak enough to force rapid easing, yet inflation is not cool enough to justify a clean risk-on multiple expansion.

Corporate profit growth slowing that sharply is a second-order warning for margins, not just earnings growth. If inventories were the main drag, that is a near-term earnings issue for wholesalers, retailers, and manufacturers; if services demand is also cooling, the pressure broadens into labor-intensive consumer-facing sectors over the next 1-2 quarters. The market may be underestimating how quickly lower top-line nominal growth can translate into margin compression once wage stickiness is combined with slower volume growth.

The contrarian view is that the release is mildly stagflationary rather than outright weak, which is usually better for quality balance sheets than for broad index beta. Consensus may be too focused on the growth downgrade and not enough on the fact that nominal GDP is still running above real GDP by a wide margin, keeping pricing power and revenue growth alive for companies with exposure to government spend, defense, infrastructure, and export channels.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00