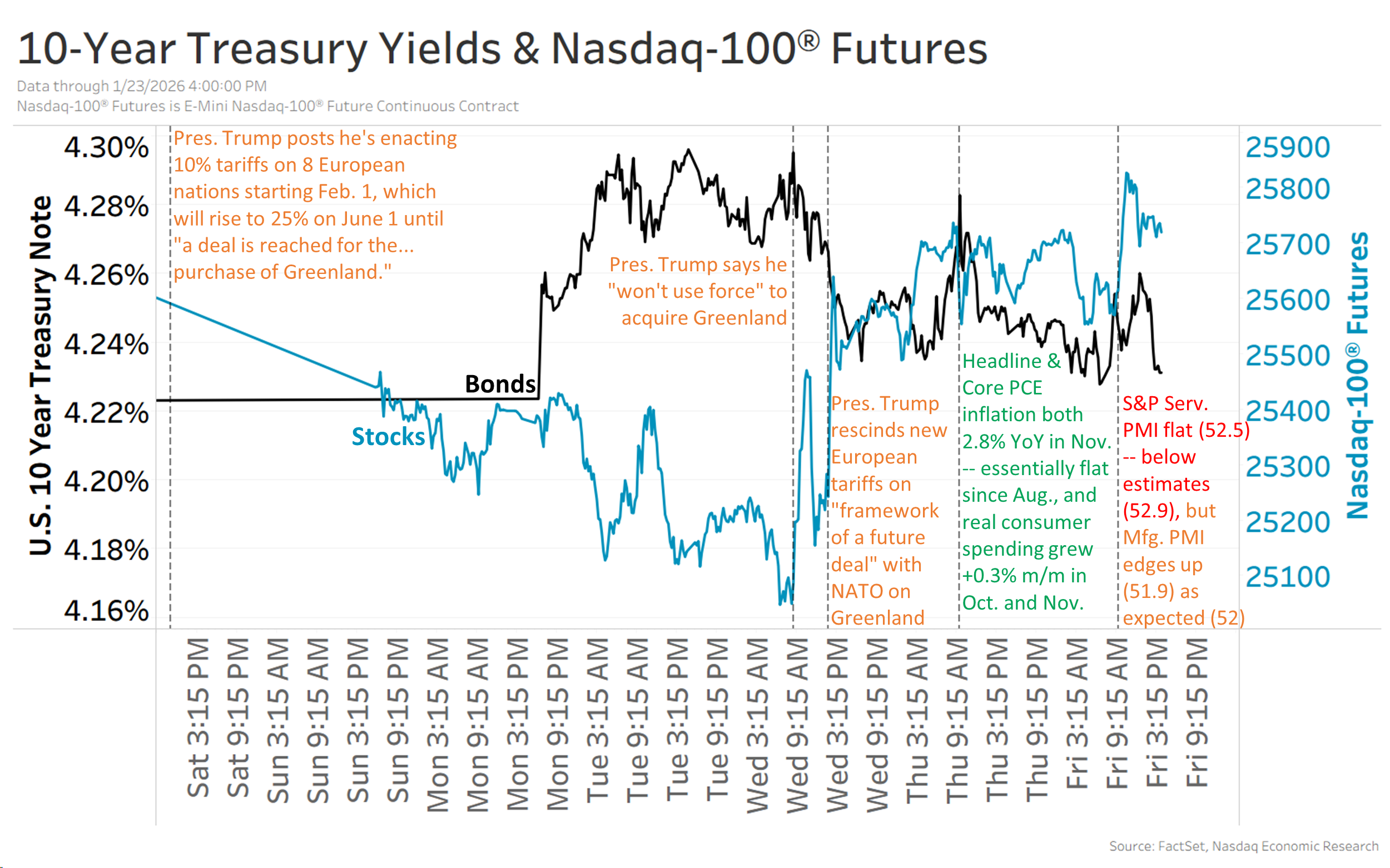

Headline and core PCE inflation both printed 2.8% YoY in November and have been essentially flat since August, with core goods inflation also flattening—signaling tariff-related inflation may be peaking. Real consumer spending expanded a solid +0.3% month-on-month in October and November across discretionary categories, supporting resilient demand; markets recovered midweek leaving the Nasdaq-100 and 10-year yields roughly flat for the week. Key near-term catalysts include Wednesday’s Fed decision (97% chance of no change), major Q4 earnings from MSFT, META, TSLA (Wed) and AAPL (Thu), and December PPI on Friday.

Market structure: Cooling headline and core PCE at 2.8% YoY and flat since August, combined with real consumer spending +0.3% MoM (Oct/Nov), favors consumer discretionary, travel/restaurant chains and device makers that benefit from resilient services consumption. Flattening core goods inflation reduces input-cost pass-through and strengthens retailer margins (favoring XLY over XLI) while removing near-term upward pressure on nominal yields, supporting long-duration growth (MSFT, META) if earnings hold. Risk assessment: Primary tail risks are (1) a re-acceleration of inflation (PCE >3.5% or MoM CPI surprise >0.5%) that forces Fed hawkishness, and (2) a sharp reversal in consumer funding (credit-card delinquencies rising >50bp or personal savings drawdown >$150B) that would collapse discretionary spending. Immediate horizon (days): Fed decision/earnings will drive realized vol; short-term (weeks): PPI and payrolls; long-term (quarters): durable decline in inflation would compress term premium and re-rate growth multiples. Trade implications: Tactical trades: favor 6–12 week exposure to consumer discretionary and long-duration growth while hedging earnings risk—e.g., small long positions in AAPL (1–2% portfolio) and XLY (2%) with defined downside protection; add 10-year duration exposure sized to 1% portfolio expecting yields to drift lower (stop if 10y >3.75%). Use short-dated options around MSFT/META/TSLA prints (buy straddles/strangles sized to 0.5% each) to monetize event-driven volatility. Contrarian angles: Consensus underestimates the durability risk if services inflation stays sticky despite cooling goods—this would lift real yields and punish growth; conversely, markets may be underpricing a benign Fed path: if PCE stays ≤2.8% and PPI decelerates Friday, expect a 20–40bp fall in 10y within 6–8 weeks, suggesting mispriced duration. Historical parallel: 2019 disinflation led to equity multiple expansion; unintended consequence: miners/commodity cyclicals may lag and should be avoided over next 3–6 months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment