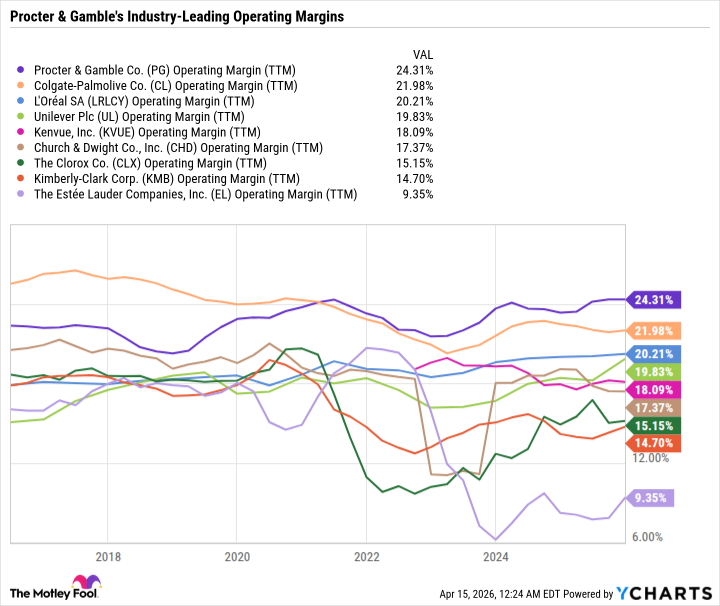

Procter & Gamble announced its 70th consecutive annual dividend increase, lifting the quarterly payout 3% to $1.0885 per share, or $4.354 annually, for a forward yield of about 3%. The company continues to support the dividend with $6.75 in trailing-12-month EPS, $6.09 in FCF per share, and a 61.9% payout ratio, while highlighting resilient margins above 20% and broad brand diversification. Shares are described as trading at a five-year low valuation, with a 21.4 P/E and 20.8 forward P/E versus 20.3 for the S&P 500.

PG’s dividend raise is less a signal of acceleration than of balance-sheet discipline: management is choosing to preserve optionality in a period where volume elasticity is getting harder to ignore. The key second-order effect is that a low-single-digit raise telegraphs a more cautious stance on future capital deployment, which can be a subtle headwind for multiple expansion if investors were hoping for a reacceleration in buybacks or margin leverage.

The competitive dynamic is not just "defensive staples versus consumers under pressure"; it is premium-brand mix versus private-label trade-down. If household budgets stay tight for another 2-3 quarters, the pressure will likely show up first in lower-tier baskets and in categories where retailer own-label substitution is easiest, which benefits big-box retailers more than branded CPGs. That creates a relative winner in WMT/COST versus PG on the consumer wallet share axis, even if PG retains unit share better than smaller peers.

The contrarian miss is that a high-quality dividend name can still be a value trap if the market is already paying for bond-proxy durability while real earnings growth slows. At ~20x forward earnings, PG is not cheap enough to absorb a prolonged period of mid-single-digit organic growth with only modest margin expansion; the stock likely needs either a rate cut backdrop or a reacceleration in category growth to sustain outperformance. Near term, the stock can continue to work as a carry trade, but over 6-12 months the upside is capped unless the consumer stabilizes or FX/headline inflation eases materially.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mildly positive

Sentiment Score

0.45

Ticker Sentiment