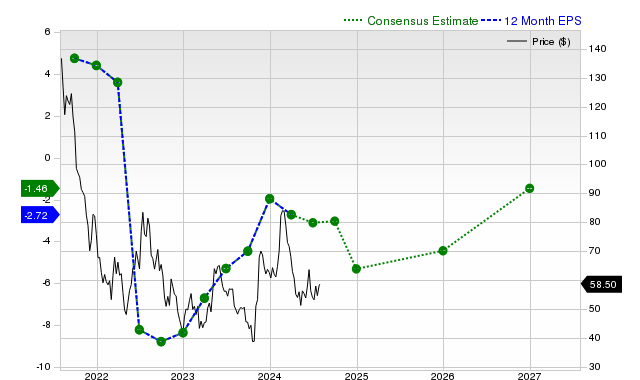

CRISPR Therapeutics (CRSP) shares have underperformed recently, declining 5% over the past month against a rising S&P 500 and industry. Analyst estimates indicate a projected current fiscal year EPS loss of -$6.57, followed by a significant turnaround to a $3.70 profit in the next fiscal year, alongside highly volatile revenue forecasts including a +1311.8% QOQ increase. The company currently holds a Zacks Rank #3 (Hold) and is assessed with an 'F' for valuation, suggesting it trades at a premium to its peers.

CRISPR Therapeutics (CRSP) exhibits a stark contrast between its recent performance, current fundamentals, and future expectations. The stock has significantly underperformed, declining 5% over the past month against a 7.1% gain in its industry and a 3.4% rise in the S&P 500. This bearish momentum is concurrent with projections for a substantial current-year loss of $6.57 per share. However, analyst consensus points to a dramatic inflection point, forecasting a swing to a $3.70 EPS profit in the next fiscal year, driven by an anticipated 554.6% surge in revenue. This projected revenue growth is highly volatile, following an expected 3.1% decline for the current full year. The company's execution history presents a mixed signal; it has surpassed EPS estimates in three of the last four quarters but missed revenue consensus significantly in its last report by -86.45%. This inconsistency, coupled with a Zacks Value Style Score of 'F', indicates the stock trades at a premium to peers, suggesting high growth expectations are already priced in, while the overall Zacks Rank of #3 (Hold) implies an anticipated in-line market performance in the near term.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mixed

Sentiment Score

0.00

Ticker Sentiment