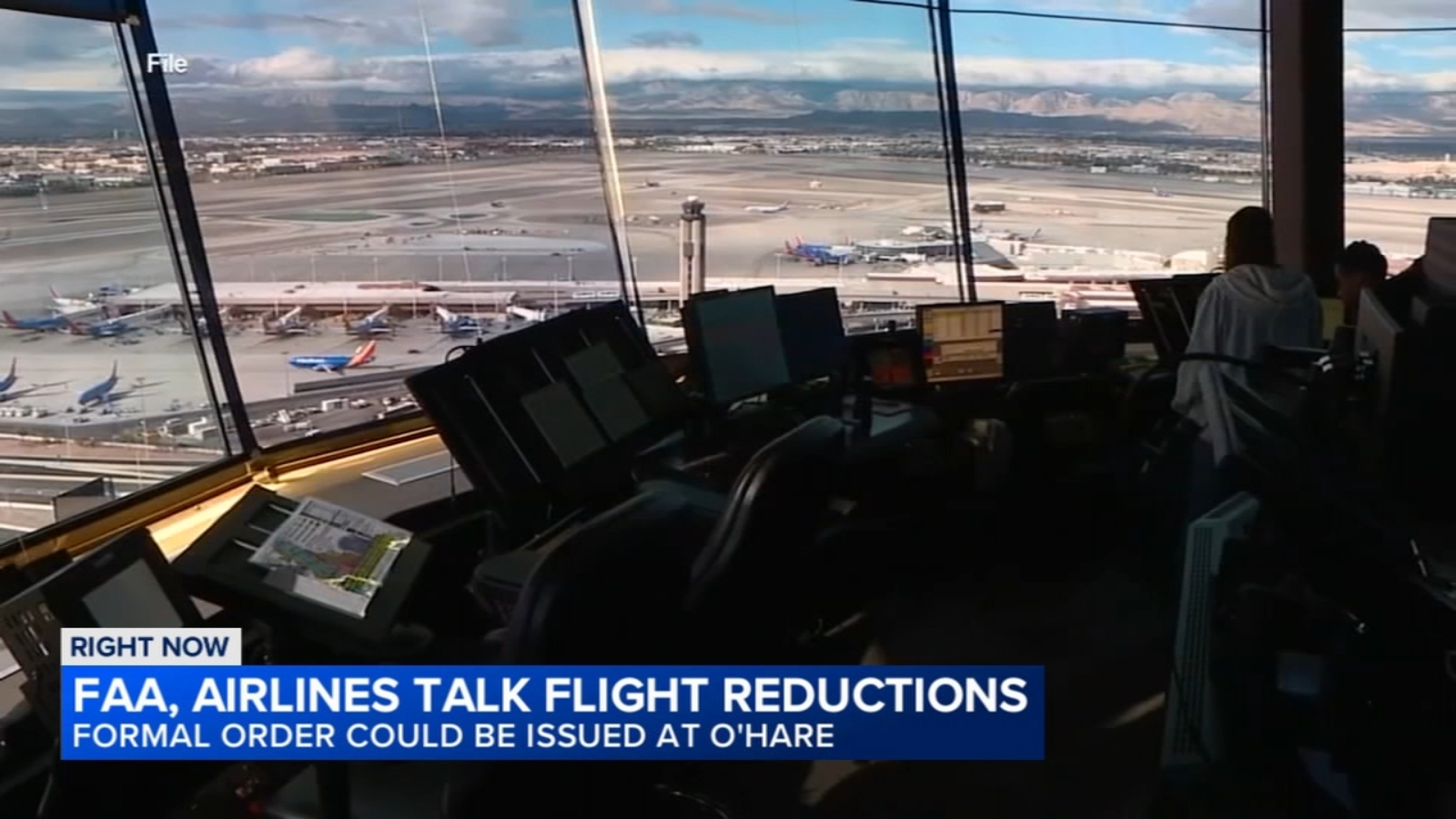

The FAA convened major carriers to address alleged over‑scheduling at Chicago O'Hare and plans to cut flights from March 29 through October 25 to relieve pressure on terminals, runways and ATC. The measure comes as United and American are pursuing significant flight increases and competing for gates amid O'Hare terminal expansion, raising short‑term capacity and operational risk at the airport. The move is intended to improve safety and customer experience but could constrain summer capacity and influence market share dynamics for carriers concentrated at ORD.

Market structure: The FAA’s planned flight reduction at ORD from Mar 29–Oct 25 acts as a short-term supply cap that should lift load factors and fares across the summer peak if enforced; legacy hub operators (UAL, AAL) with gate control and revenue management systems are positioned to capture most upside while smaller/expansionary carriers face growth curbs. Reduced flight counts compress ASMs (likely low-single-digit % decline at ORD month-to-month during the window) which increases unit revenue sensitivity to demand shocks and gives incumbents marginal pricing power.

Risk assessment: Tail risks include the FAA imposing stricter slot limits or reassigning gates (triggering litigation/antitrust suits) and severe operational disruptions (weather/capacity outages) that could flip summer profitability negative; probability low-to-medium but high impact for highly levered carriers. Immediate (days) — share volatility on headlines; short-term (weeks/months) — visible lift/fall in yields and load factors; long-term (quarters/years) — terminal expansion at ORD will reset capacity dynamics (~post-2026) and could dilute any temporary pricing benefit.

Trade implications: Direct trade favors carriers with durable hub advantages and better balance sheets; consider concentrated, size-controlled exposure to AAL/UAL depending on which secures visas/gates. Options: sell limited-risk call spreads to monetize near-term IV if enforcement seems likely, or buy call spreads to play higher fares; monitor TSA throughput and weekly capacity for entry/exit triggers. Cross-asset: expect modest tightening of airline HY spreads and a short-term reflationary impulse to jet fuel demand, but FX and broad commodities impact minimal.

Contrarian angles: The consensus treats cuts as uniformly negative for growth, but modest, temporary capacity discipline often improves unit economics — a 2–5% capacity reduction at a hub can lift fares 3–7% in peak weeks historically. Market may underprice the upside for the operator that avoids disproportionate cuts; unintended consequences include accelerated passenger migration to secondary airports (benefiting carriers with MDW/MDW-adjacent strength) and protracted gate litigation that keeps capacity constrained beyond Oct 25.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

-0.10

Ticker Sentiment