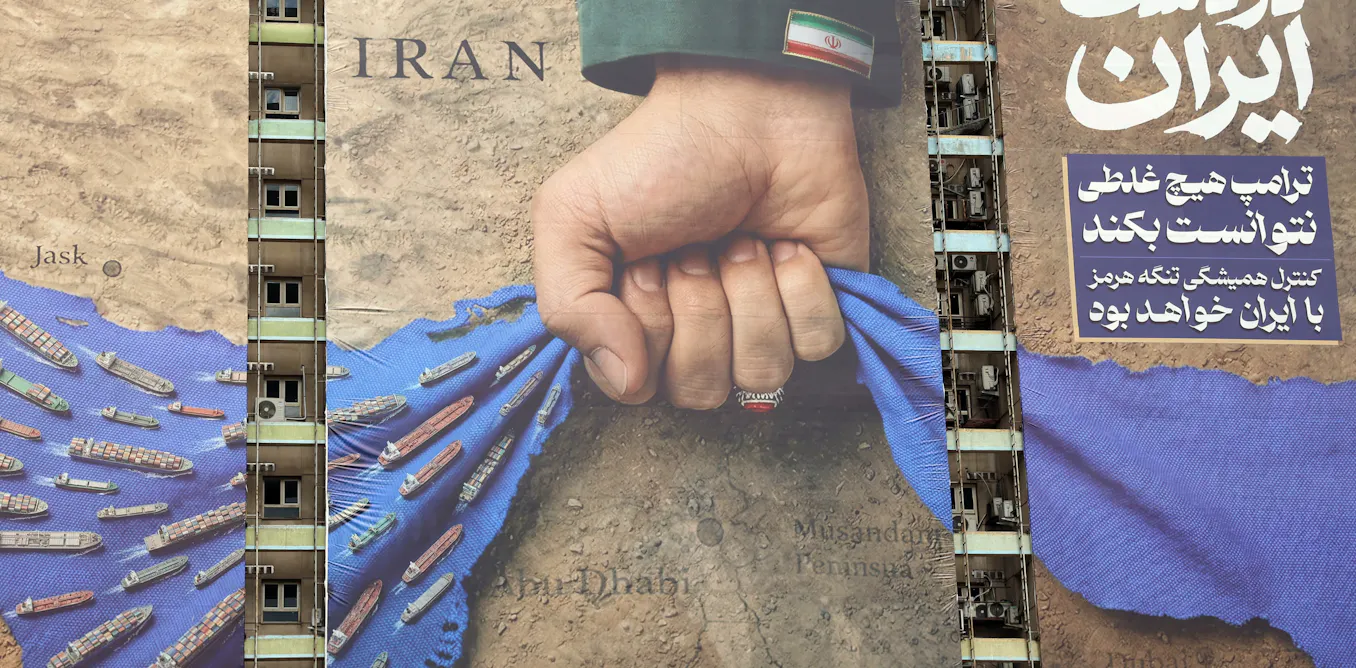

The article argues the US and Israel cannot achieve a decisive victory over Iran, warning the conflict is settling into a prolonged stalemate. It highlights risks to the Strait of Hormuz, energy infrastructure, and regional retaliatory strikes, with the US said to have already consumed roughly 45% to 50% of key missile stockpiles, including about 30% of Tomahawk inventory. The piece frames the situation as a potential forever war with elevated risk of regional disruption, displacement, and a broader economic shock.

The market is underpricing the difference between a kinetic headline risk and a durable macro regime shift. The first-order winners are not just upstream energy producers, but the entire volatility stack: crude optionality, tanker rates, airfreight, and defense/logistics names with exposure to replenishment cycles. The more important second-order effect is that prolonged uncertainty acts like a tax on global working capital — higher inventory buffers, rerouting costs, and more expensive insurance — which supports pricing power in select industrials while compressing margins for transport-heavy users.

The longer this remains unresolved, the more the market has to price a chronic risk premium rather than a one-off spike. That argues for a flatter-but-higher energy curve: front-end crude can gap on headlines, but sustained strength should show up in refined product spreads, LNG/propane arbitrage, and shipping bottlenecks before it becomes obvious in spot Brent. Aviation is the cleanest loser because it has direct fuel sensitivity plus limited ability to pass through cost in the short run; the lag between fuel cost inflation and fare repricing is where P&L compression should show up over the next 1-2 quarters.

The contrarian read is that consensus may be overestimating the odds of a clean supply shock and underestimating policy intervention. If the conflict stays contained, the market can fade the panic premium faster than many expect, especially if strategic reserves, diplomacy, or corridor security reduce tail risk. But if the issue is endurance rather than escalation, the right expression is not chasing outright beta; it is owning convexity in assets that benefit from persistent uncertainty and shorting those with the worst pass-through economics.

The highest-value setup is to buy protection before realized vol reprices, not after the first spike. The optimal window is on relief rallies or ceasefire headlines, when implied volatility in oil, shipping, and defense-linked names typically cheapens faster than the underlying geopolitical probability distribution.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.75