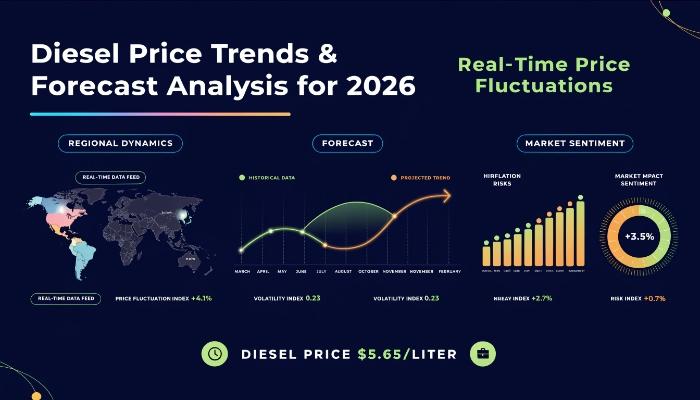

March 2026 diesel prices were mixed globally: North America rose 4.9% to $1.08/Kg, while Europe fell 1.4% to $2.16/Kg and India dropped 6.7% to $0.98/Kg. The article attributes the divergence to stronger transportation and agricultural demand in North America versus softer industrial activity and freight demand in Asia and Europe. The outlook points to moderate stability, but regional volatility should persist as crude prices, refinery maintenance, and logistics costs continue to drive price dispersion.

The important signal is not the regional print itself but the dispersion: diesel is functioning as a real-time stress test for industrial activity and logistics. North America’s firmness implies that freight, farm, and maintenance-driven inventory tightness are still translating into near-term earnings support for midstream, refiners, and trucking capacity owners, while the softer Asia/Europe prints argue for margin relief in fuel-intensive sectors and weaker pass-through into consumer prices over the next 1-2 quarters.

The second-order effect is that this is a relative-value setup more than a directional energy call. Regions with declining diesel should see incremental support for airlines, parcel/logistics, chemicals, and heavy manufacturing through lower input costs; regions with rising diesel face a hidden tax on small-cap transport and agriculture, where fuel is a larger share of opex and pricing power is weaker. If inventories in North America normalize after maintenance, the current firmness can fade quickly, but if export pull from Latin America or seasonal ag demand persists, the spread can stay elevated into early summer.

The market may be underestimating how much of the current move is a policy/operations issue rather than pure demand. Refinery maintenance, compliance costs, and taxation can keep European diesel structurally expensive even when demand softens, which compresses the probability of a sharp downside snapback. Conversely, the bearish case on Asia may be overstated if manufacturing and shipping cycle higher in Q2; that would be the fastest catalyst for a reversal because diesel demand responds almost immediately to freight and industrial throughput.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

neutral

Sentiment Score

-0.02