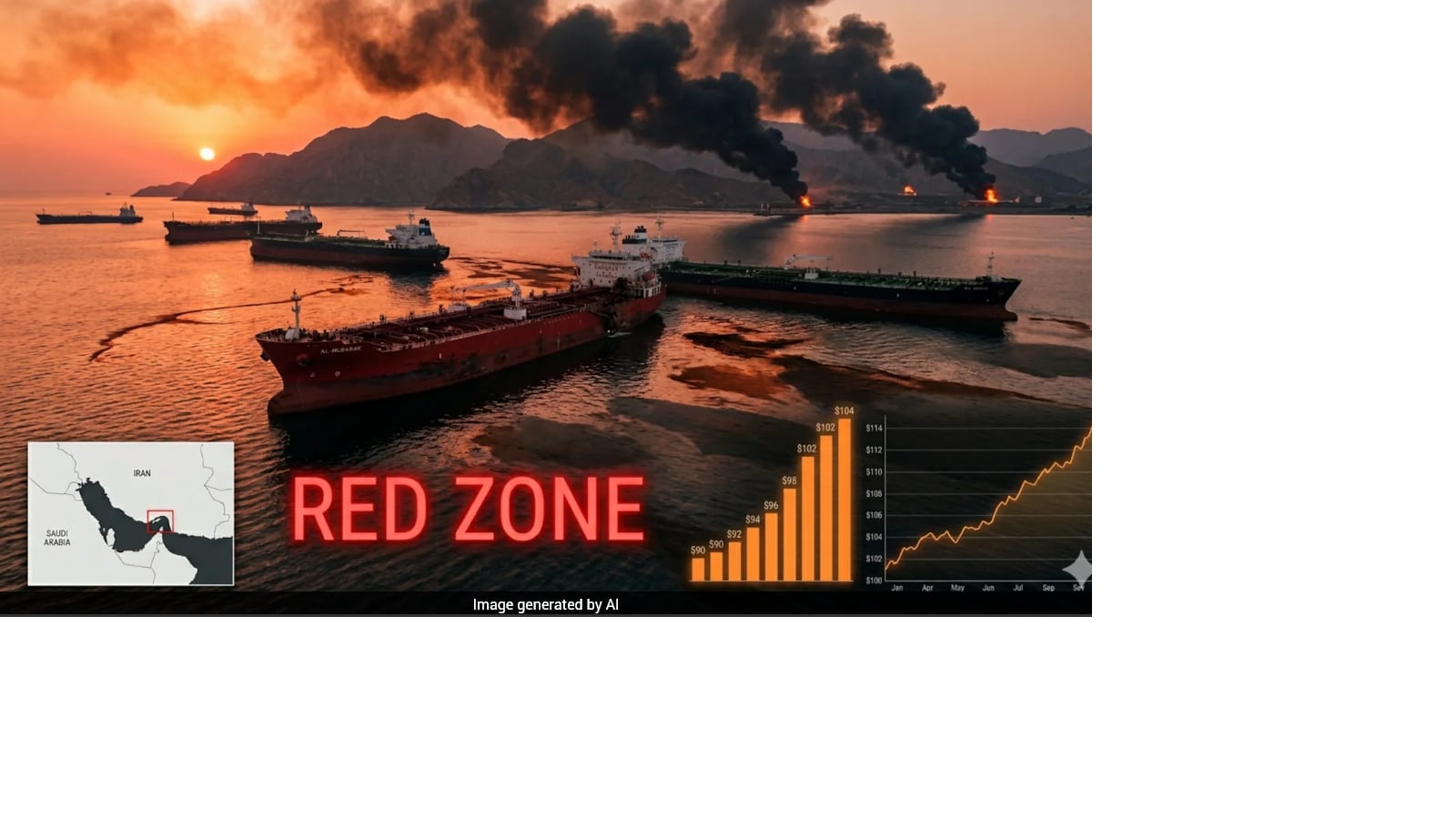

The closure of the Strait of Hormuz has already removed an estimated 14 million barrels of oil per day from global markets, with the IEA warning of a potential "red zone" by July if disruptions persist. Global stockpiles are being depleted after a record 400 million-barrel release, while Brent has risen to $104-$105 a barrel from $72 before the war and could exceed $120 if fighting resumes. The shock threatens broader fuel inflation, with especially severe effects on poorer nations and energy-importing markets.

The market is still pricing this as an oil headline, but the bigger second-order move is a forced repricing of global logistics optionality. When the cheapest maritime route becomes unreliable, the marginal barrel does not just get more expensive; the entire distribution stack re-rates via higher tanker insurance, longer voyage times, inventory buffers, and refinery substitution costs. That tends to hit transport-heavy EMs, airlines, and chemical/feedstock users before it fully shows up in broad inflation prints. The key inflection is not the spot price level, it is duration. A brief disruption is manageable because inventories and strategic releases smooth the shock; a multi-week bottleneck into the summer travel season creates a convex jump in working-capital needs and erodes demand elasticity. That means the next leg of pain likely comes from margin compression in sectors that cannot pass through costs fast enough, while upstream energy names with low decline rates and physical optionality gain relative scarcity value. The contrarian risk is that the market overestimates immediate pass-through to headline CPI and underestimates policy response. If governments accelerate reserve releases, impose freight subsidies, or secure alternate supply corridors, the most violent part of the move may be front-loaded and then mean-revert. In that case, the best trade is not to chase beta to oil, but to own the convexity around further escalation and short the cost absorbers most exposed to persistent fuel input inflation. META and TSLA are not direct operational shorts here, but they are exposed through ad budgets and consumer discretionary spend if gasoline/jet fuel stays elevated for another quarter. The higher-confidence opportunity is in airlines, parcel/logistics, and emerging-market consumers first; the second-order consumer demand hit usually arrives with a lag, so the best entry is on confirmation that Hormuz remains constrained into July rather than on the initial spike alone.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

extremely negative

Sentiment Score

-0.85

Ticker Sentiment