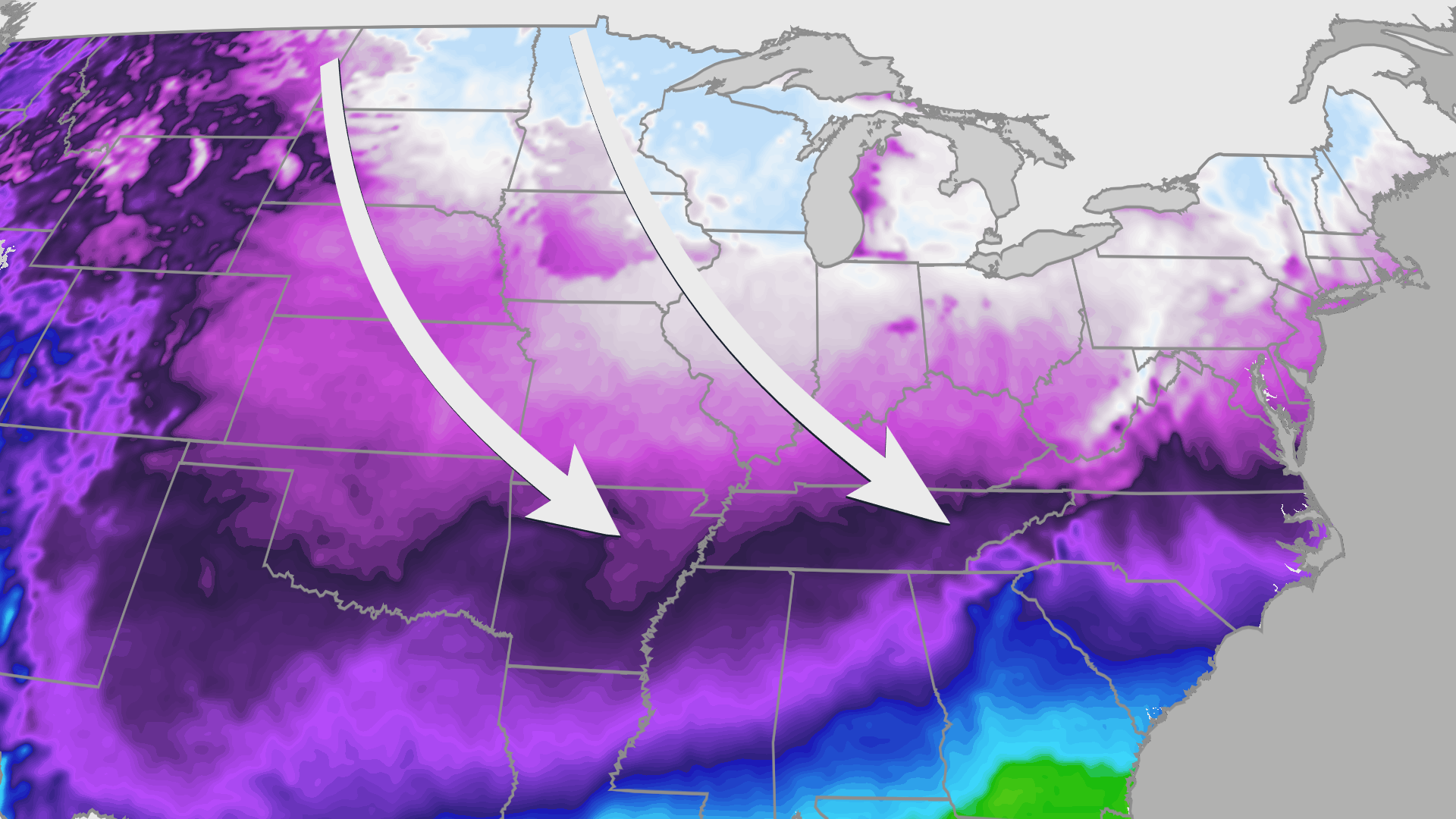

A severe arctic outbreak will drive the coldest air of the season across the U.S., with actual lows of 15–25°F below zero across the Plains and Midwest and wind chills as low as 35–45°F below zero in places; International Falls could reach −40°F on Saturday. The event peaks Thursday–Saturday and the cold pushes south with Winter Storm Fern bringing ice, multi-day subfreezing highs, and the risk of widespread power outages and prolonged pipe damage across the Deep South; near-term implications include sharply elevated heating demand, stress on utilities and fuel markets, and potential insurance and infrastructure losses in affected regions.

Market structure: Extreme cold is a multi-day demand shock concentrated in the Northern Plains, Midwest, South and Northeast that will likely add an incremental 5–15 Bcf/day regional gas burn for 7–10 days, driving front-month Henry Hub volatility and regional basis blowouts (Midwest/South). Direct winners: natural‑gas producers with free cash flow sensitivity, pipeline operators (fee‑for‑transport) and genset/OEM vendors (Generac GNRC), as well as home improvement retailers (HD/LOW). Losers: unhedged gas marketers/retailers, small municipal utilities with stressed distribution, and insurers facing winter-storm claims. Risk assessment: Tail risks include prolonged multi-week outages, pipeline freeze‑offs or LNG/LNG feedgas force‑majeures that could push spot gas +20–50% and power prices to extreme spikes; regulatory interventions (price caps/disconnect moratoria) are medium probability in populous Southern states. Immediate horizon (0–14 days) is dominated by load and outage dynamics; short term (weeks–months) by storage draws and basis normalization; long term (quarters) by capex and incremental pipeline throughput. Hidden dependencies: local distribution constraints, counterparty credit among retail suppliers and municipal balance sheets. Trade implications: Favor short‑dated directional plays on natural gas volatility and equipment demand: buy front‑month NG call spreads (20–30 delta long) sized to 1–3% portfolio, target +30–80% payoff if spot jumps 20–50% in 7–14 days; buy GNRC (2% position) or 6–8 week 25‑delta calls to play emergency genset demand and grid outages. Consider 1–2% tactical longs in HD (consumer repair demand) and KMI (pipeline toll exposure), and avoid long positions in small unhedged retail gas marketers and undercapitalized municipal utilities. Contrarian angles: Consensus will overprice a sustained bull for gas if temperatures normalize — history (polar vortex episodes) shows sharp intramonth mean reversion once weather moderates; storage still a hinge for later winter prices. Risk of policy intervention (temporary price controls or emergency load sheds) could cap upside for spot but create idiosyncratic winners (generators with firm contracts). Monitor model updates closely: a single ECMWF run flip can unwind short‑dated option premium quickly.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35