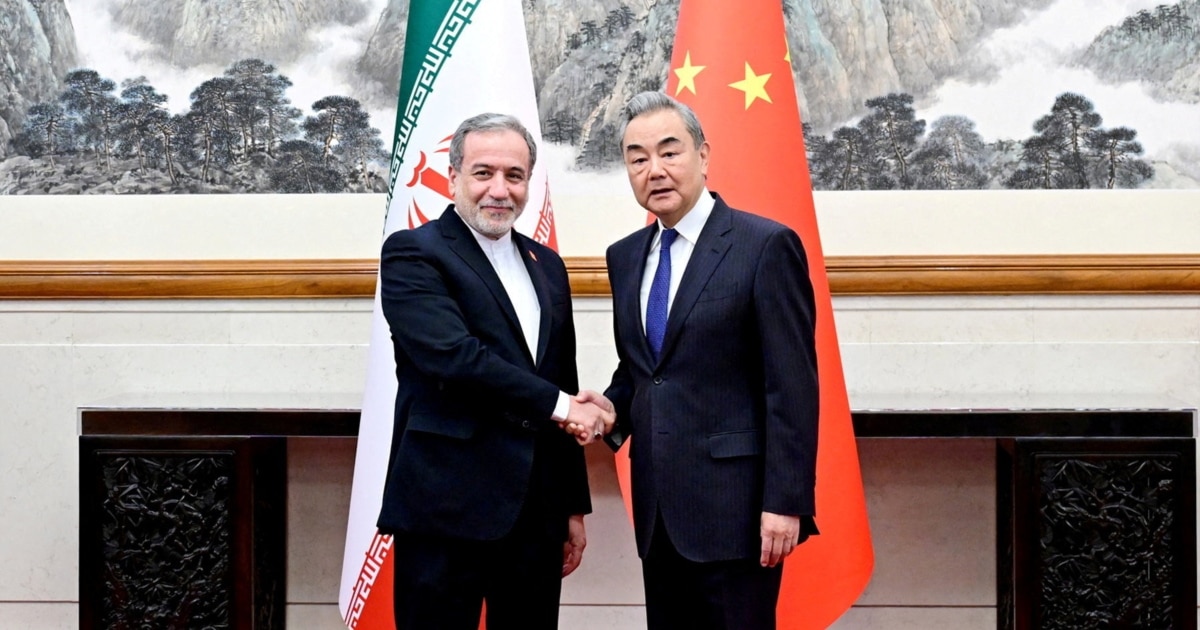

China reiterated support for a comprehensive cease-fire in the Iran-US conflict and for normal passage through the Strait of Hormuz as Iran's foreign minister visited Beijing ahead of the Trump-Xi meeting. Media reports suggest Tehran and Washington may be close to a one-page memorandum that could include an Iranian nuclear-enrichment moratorium, U.S. sanctions relief, release of frozen Iranian funds, and reduced shipping restrictions in the Strait of Hormuz. The article also highlights the risk of a new U.N. Security Council resolution targeting Iran and the potential for Chinese financial backing to offset U.S. pressure.

The market is underestimating how much of this is about maritime optionality rather than headline diplomacy. Any credible path to a Hormuz de-escalation would disproportionately benefit Asian refiners, LNG importers, and container/shipping names with heavy Gulf exposure, while pressuring freight-rate volatility, bunker spreads, and defense premiums embedded in regional logistics. The bigger second-order effect is that even a partial truce lowers the probability of emergency inventory hoarding across Europe and Asia, which can unwind an energy-risk bid faster than the underlying conflict premium itself.

China’s posture matters because it is one of the few actors that can convert rhetoric into enforcement leverage through payment channels, shipping insurance, and trade finance. If Beijing is willing to underwrite a thaw, the immediate winner is not Iran so much as China’s own industrial complex: lower imported energy costs, less supply-chain disruption, and reduced tail risk for commodity-intensive sectors. Conversely, any visible Chinese backtracking would likely reprice sanctions enforcement risk across shadow shipping, ship-to-ship transfer activity, and non-Western insurers within days.

The consensus is likely too linear on ‘peace = lower oil.’ A cease-fire that preserves sanctions relief and frozen-fund release would be stimulative for Iran’s import demand, but also could channel capital into infrastructure, drones, and asymmetric capabilities over a 6-18 month horizon, raising medium-term security premiums again. The highest-probability mispricing is that investors focus on crude beta while ignoring the re-rating of compliance risk, where firms exposed to transshipment, port services, and dual-use industrial exports can move more on policy ambiguity than on spot prices.

Catalyst timing is short. The Trump-Xi meeting is the key binary in the next 1-2 weeks; if the talks produce even a vague endorsement of talks, shipping and oil-volatility proxies should fade quickly. If negotiations stall, expect a sharp reversal in risk assets tied to Asia trade corridors and a renewed bid for defense and energy names within days, not months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

-0.05